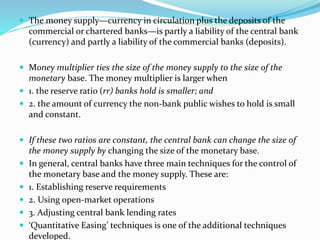

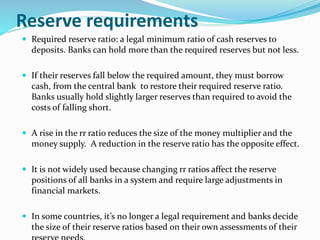

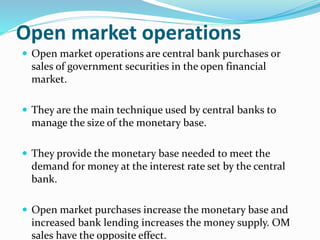

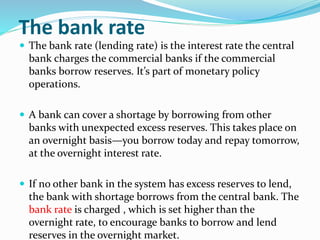

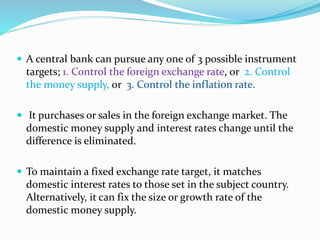

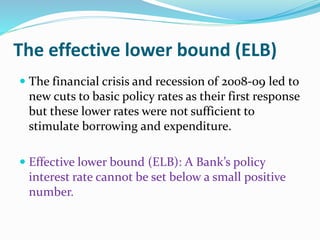

The document discusses central banking and monetary policy. It provides an overview of central banking techniques like open market operations, reserve requirements, and adjusting interest rates to influence money supply and aggregate demand. The document also discusses monetary policy targets like inflation, money supply, and exchange rates. It describes indicators like interest rates and exchange rates that central banks use to gauge the impact of their policies. Quantitative easing and other unconventional policies are mentioned as tools used when interest rates near the effective lower bound.