Downloaded 50 times

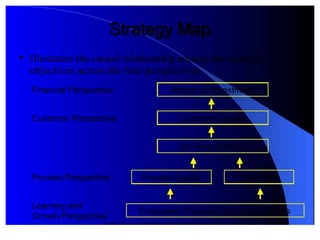

The document discusses the Balanced Scorecard (BSC) framework for measuring organizational performance. The BSC balances traditional financial measures with non-financial measures across four perspectives: financial, customer, internal processes, and learning and growth. It allows organizations to track financial results while also monitoring capabilities for future growth. A strategy map illustrates the causal relationships between objectives in each perspective. The BSC is well-suited for non-profits and governments as it can assess performance through non-financial metrics related to constituents.