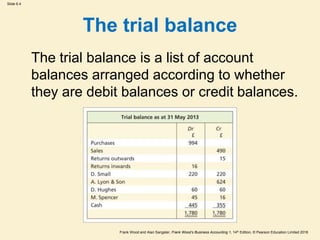

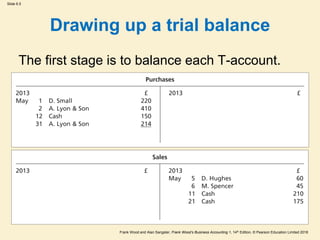

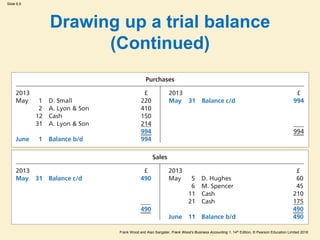

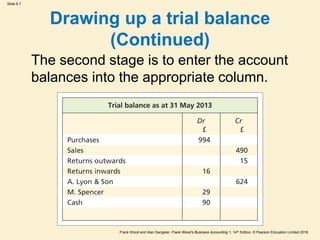

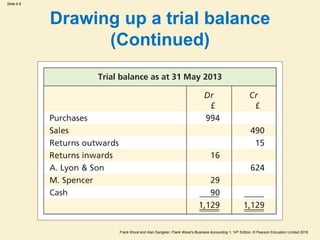

The document discusses the trial balance process in accounting. It explains that a trial balance is a list of account balances arranged by debit and credit columns, and is used to check that the total debits equal total credits. This ensures each transaction has both a debit and credit entry. However, some errors will not be caught by a balanced trial balance. The trial balance is prepared at the end of an accounting period before financial statements.