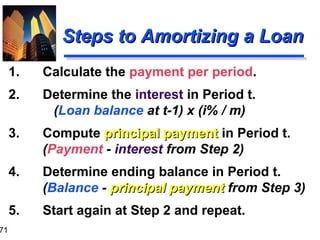

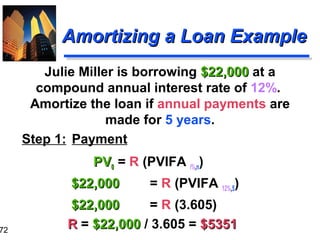

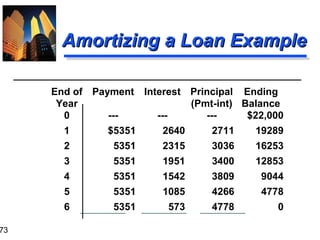

Downloaded 74 times

![14

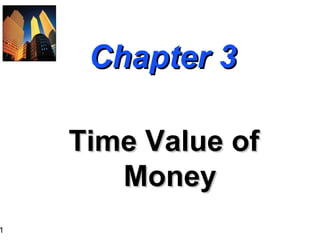

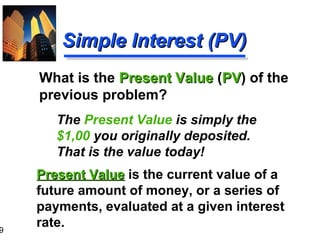

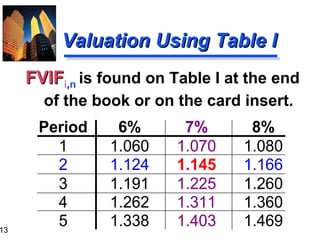

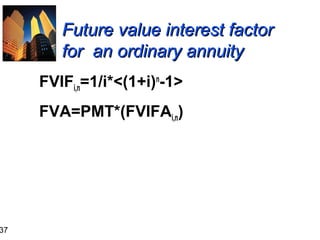

Using Future Value Tables

FV2

= $1,000 (FVIF7%,2)

= $1,000 (1.145)

= $1,145 [Due to Rounding]

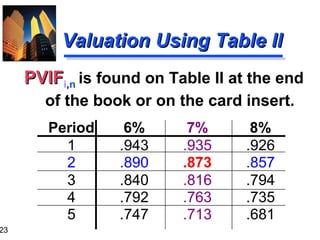

Period

6%

7%

8%

1

1.060

1.070

1.080

2

1.124

1.145

1.166

3

1.191

1.225

1.260

4

1.262

1.311

1.360

5

1.338

1.403

1.469](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-14-320.jpg)

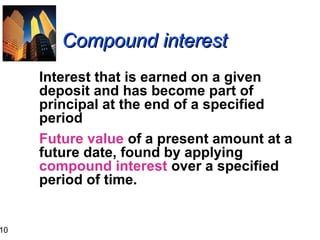

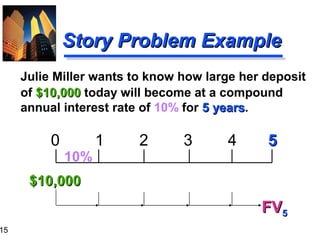

![16

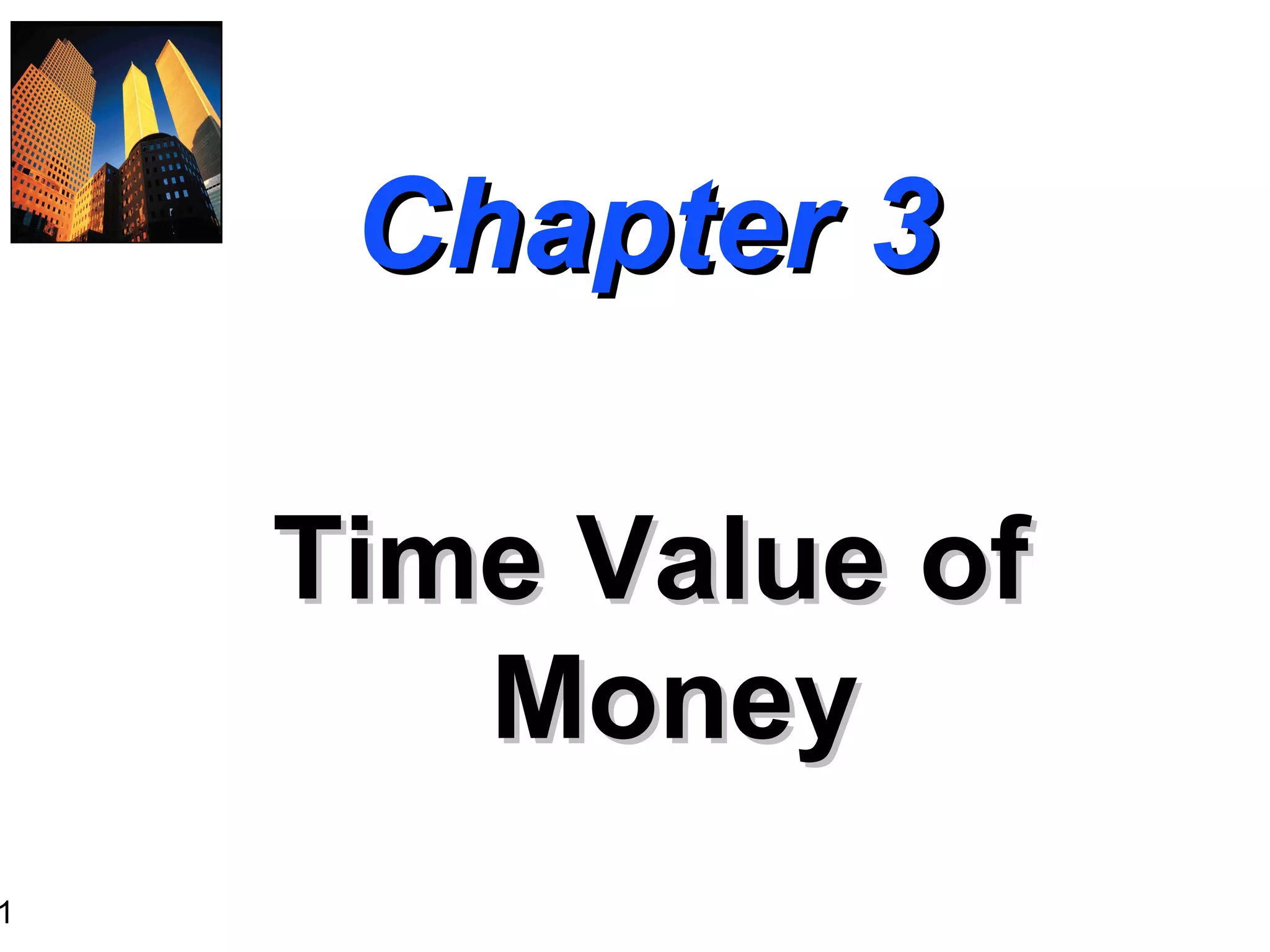

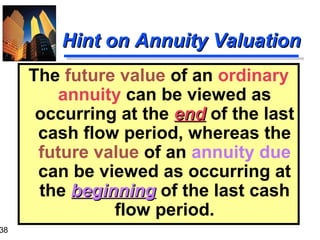

Story Problem Solution

Calculation based on general formula:

FVn = P0 (1+i)n

FV5 = $10,000 (1+ 0.10)5

= $16,105.10

Calculation based on Table I:

FV5 = $10,000 (FVIF10%, 5)

= $10,000 (1.611)

= $16,110 [Due to Rounding]](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-16-320.jpg)

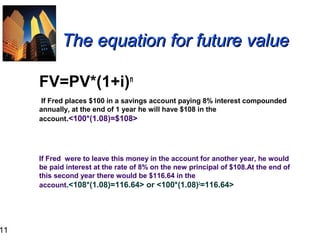

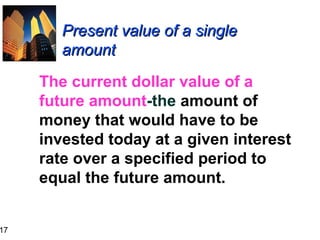

![24

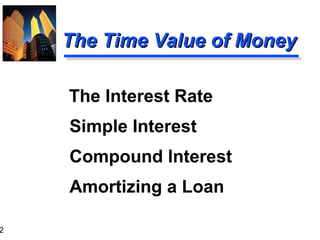

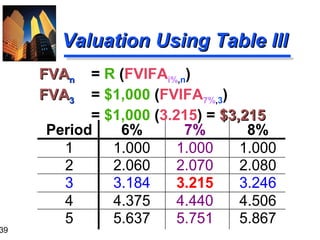

Using Present Value Tables

PV2

= $1,000 (PVIF7%,2)

= $1,000 (.873)

= $873 [Due to Rounding]

Period

6%

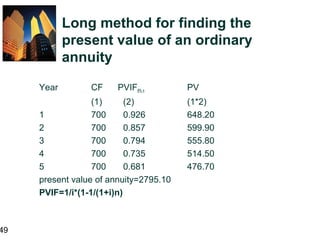

7%

1

.943

.935

2

.890

.873

3

.840

.816

4

.792

.763

5

.747

.713

8%

.926

.857

.794

.735

.681](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-24-320.jpg)

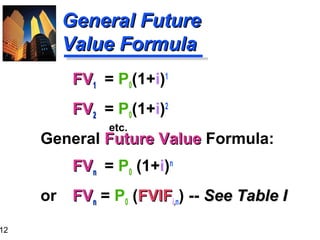

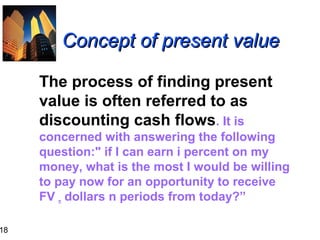

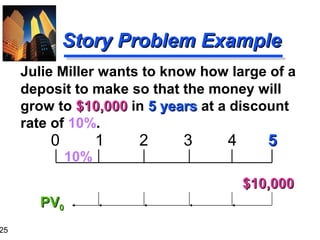

![26

Story Problem Solution

Calculation based on general formula:

PV0 = FVn / (1+i)n

PV0 = $10,000 / (1+ 0.10)5

= $6,209.21

Calculation based on Table I:

PV0 = $10,000 (PVIF10%, 5)

= $10,000 (.621)

= $6,210.00 [Due to Rounding]](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-26-320.jpg)

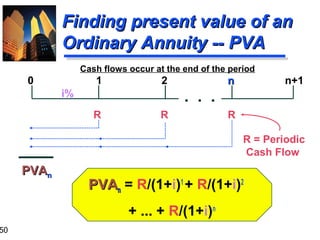

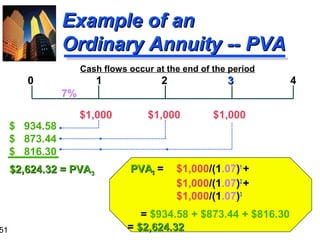

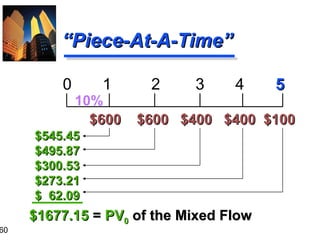

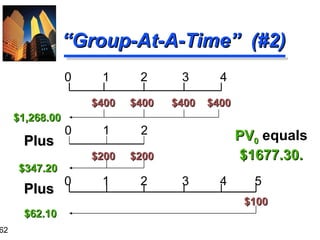

![61

“Group-At-A-Time” (#1)

0

10%

1

$600

2

3

4

5

$600 $400 $400 $100

$1,041.60

$ 573.57

$ 62.10

$1,677.27 = PV0 of Mixed Flow [Using Tables]

$600(PVIFA10%,2) =

$600(1.736) = $1,041.60

$400(PVIFA10%,2)(PVIF10%,2) = $400(1.736)(0.826) = $573.57

$100 (PVIF10%,5) =

$100 (0.621) =

$62.10](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-61-320.jpg)

![63

Frequency of

Compounding

General Formula:

FVn = PV0(1 + [i/m])mn

n:

Number of Years

m:

Compounding Periods per Year

i:

Annual Interest Rate

FVn,m: FV at the end of Year n

PV0:

PV of the Cash Flow today](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-63-320.jpg)

![64

Impact of Frequency

Julie Miller has $1,000 to invest for 2

years at an annual interest rate of

12%.

Annual

FV2

= 1,000(1+ [.12/1])(1)(2)

1,000

= 1,254.40

Semi

FV2

= 1,000(1+ [.12/2])(2)(2)

1,000

= 1,262.48](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-64-320.jpg)

![65

Impact of Frequency

Qrtly

FV2

= 1,000(1+ [.12/4])(4)(2)

1,000

= 1,266.77

Monthly

FV2

= 1,000(1+ [.12/12])(12)(2)

1,000

= 1,269.73

Daily

FV2

= 1,000(1+[.12/365])(365)(2)

1,000

= 1,271.20](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-65-320.jpg)

![67

Effective Annual

Interest Rate

The annual rate of interest actually

paid or earned

The actual rate of interest earned

(paid) after adjusting the nominal

rate for factors such as the number

of compounding periods per year.

(1 + [ i / m ] )m - 1](https://image.slidesharecdn.com/ch03-131129205538-phpapp01/85/Time-volue-of-money-67-320.jpg)

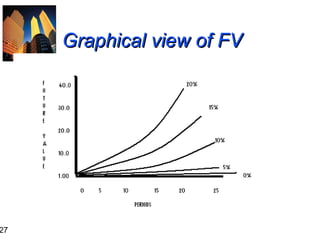

1. The document discusses the concepts of time value of money, interest rates, and different types of interest including simple and compound interest. 2. It provides formulas for calculating future value and present value using simple and compound interest, and examples of applying these formulas. 3. The document also covers annuities, explaining the differences between ordinary annuities and annuities due. It provides formulas and examples for calculating future and present value of both types of annuities.