Agenda

After studying thischapter, you should be able to:

• Calculate the future value to which money invested at a given interest rate will grow.

• Calculate the present value of a future payment

• Calculate present and future values of streams of cash payments.

• Find the interest rate implied by the present or future value.

• Explain how we would compare interest rates quoted over different intervals.

1

3.

• Financial decisionsrequire comparisons of cash payments at different dates.

• Since a dollar today does not have the same value as a dollar tomorrow, a

relationship has to be established to compare cash flows at different times.

• Future value is the amount to which a present value will grow after earning interest.

• There are two kinds of interest that money can earn:

• Simple interest

• Compound interest

FutureValues and Compound Interest

3

4.

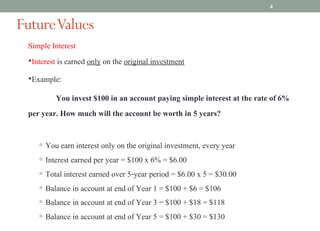

Simple Interest

•Interest isearned only on the original investment

•Example:

You invest $100 in an account paying simple interest at the rate of 6%

per year. How much will the account be worth in 5 years?

◦ You earn interest only on the original investment, every year

◦ Interest earned per year = $100 x 6% = $6.00

◦ Total interest earned over 5-year period = $6.00 x 5 = $30.00

◦ Balance in account at end of Year 1 = $100 + $6 = $106

◦ Balance in account at end of Year 3 = $100 + $18 = $118

◦ Balance in account at end of Year 5 = $100 + $30 = $130

FutureValues

4

5.

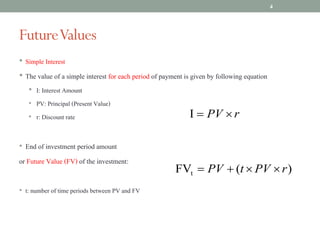

FutureValues

• Simple Interest

•The value of a simple interest for each period of payment is given by following equation

• I: Interest Amount

• PV: Principal (Present Value)

• r: Discount rate

• End of investment period amount

or Future Value (FV) of the investment:

• t: number of time periods between PV and FV

4

)

(

FVt r

PV

t

PV ´

´

+

=

r

PV ´

=

I

6.

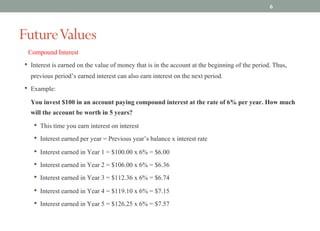

Compound Interest

• Interestis earned on the value of money that is in the account at the beginning of the period. Thus,

previous period’s earned interest can also earn interest on the next period.

• Example:

You invest $100 in an account paying compound interest at the rate of 6% per year. How much

will the account be worth in 5 years?

• This time you earn interest on interest

• Interest earned per year = Previous year’s balance x interest rate

• Interest earned in Year 1 = $100.00 x 6% = $6.00

• Interest earned in Year 2 = $106.00 x 6% = $6.36

• Interest earned in Year 3 = $112.36 x 6% = $6.74

• Interest earned in Year 4 = $119.10 x 6% = $7.15

• Interest earned in Year 5 = $126.25 x 6% = $7.57

FutureValues

6

7.

Compound Interest

• Valueat the end of Year 1 = $100.00 +[$100 x 6%] = $100 x (1+r)

• Value at the end of Year 2 = $106.00 + [$106 x 6%] = $100 x (1+r)2

• …….

• Value at the end of Year 5 = $100 x (1+r)5

•The formula for the future value of PV dollars at r% interest per period for t periods

is:

FutureValues

t

r

PV

FV )

1

( +

´

=

7

8.

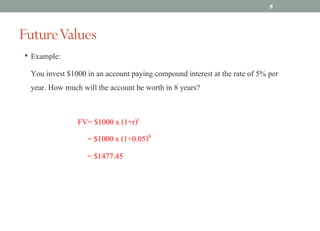

• Example:

You invest$1000 in an account paying compound interest at the rate of 5% per

year. How much will the account be worth in 8 years?

FV= $1000 x (1+r)t

= $1000 x (1+0.05)8

= $1477.45

FutureValues

8

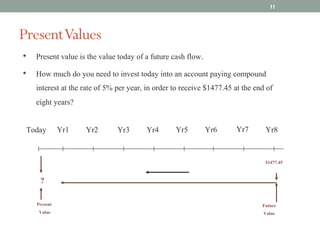

• Present valueis the value today of a future cash flow.

• How much do you need to invest today into an account paying compound

interest at the rate of 5% per year, in order to receive $1477.45 at the end of

eight years?

Yr3

$1477.45

?

Present

Value

Future

Value

Today Yr1 Yr2 Yr4 Yr7

Yr5 Yr6 Yr8

PresentValues

11

11.

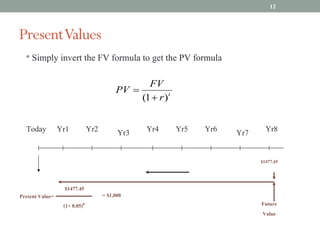

• Simply invertthe FV formula to get the PV formula

Yr3

$1477.45

Future

Value

Today Yr1 Yr2 Yr4 Yr7

Yr5 Yr6 Yr8

$1477.45

(1+ 0.05)8

= $1,000

PresentValues

t

r

FV

PV

)

1

( +

=

Present Value=

12

12.

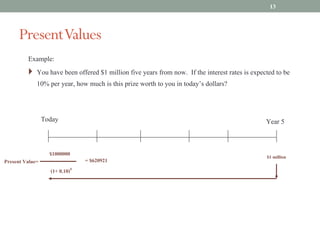

Example:

} You havebeen offered $1 million five years from now. If the interest rates is expected to be

10% per year, how much is this prize worth to you in today’s dollars?

Today Year 5

$1 million

PresentValues

$1000000

(1+ 0.10)5

= $620921

Present Value=

13

13.

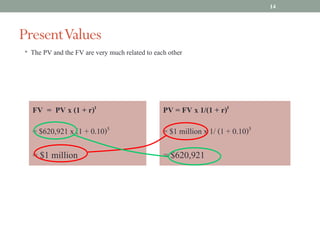

• The PVand the FV are very much related to each other

PV = FV x 1/(1 + r)t

= $1 million x 1/ (1 + 0.10)5

= $620,921

FV = PV x (1 + r)t

= $620,921 x (1 + 0.10)5

= $1 million

PresentValues

14

14.

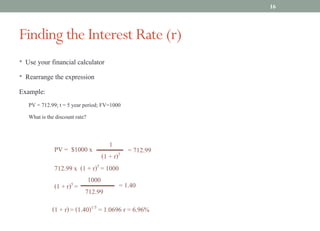

• Use yourfinancial calculator

• Rearrange the expression

Example:

PV = 712.99; t = 5 year period; FV=1000

What is the discount rate?

PV = $1000 x

1

(1 + r)5

= 712.99

712.99 x (1 + r)5 = 1000

(1 + r)5 =

1000

712.99

= 1.40

(1 + r)= (1.40)1/5 = 1.0696 r = 6.96%

Finding the Interest Rate (r)

16

15.

• Can befound the same way

• Use your financial calculator

• Use the tables – look up the discount factor

• Rearrange the expression to solve for “t”

Finding the Investment Period (t)

17

16.

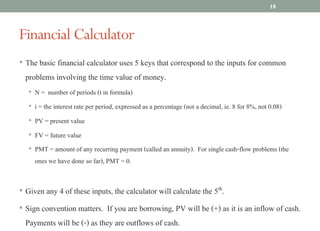

• The basicfinancial calculator uses 5 keys that correspond to the inputs for common

problems involving the time value of money.

• N = number of periods (t in formula)

• i = the interest rate per period, expressed as a percentage (not a decimal, ie. 8 for 8%, not 0.08)

• PV = present value

• FV = future value

• PMT = amount of any recurring payment (called an annuity). For single cash-flow problems (the

ones we have done so far), PMT = 0.

• Given any 4 of these inputs, the calculator will calculate the 5th.

• Sign convention matters. If you are borrowing, PV will be (+) as it is an inflow of cash.

Payments will be (-) as they are outflows of cash.

Financial Calculator

18

17.

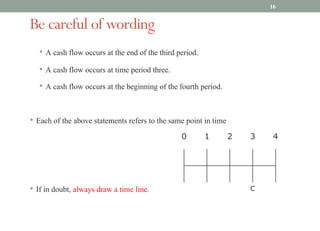

Be careful ofwording

• A cash flow occurs at the end of the third period.

• A cash flow occurs at time period three.

• A cash flow occurs at the beginning of the fourth period.

• Each of the above statements refers to the same point in time

• If in doubt, always draw a time line.

16

0 1 2 3 4

C

18.

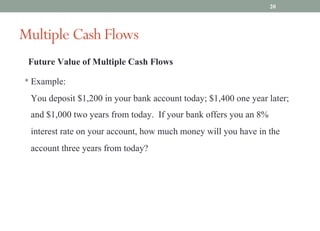

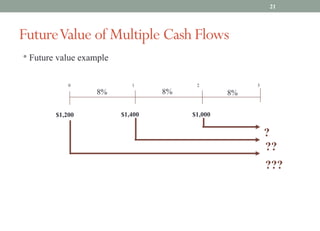

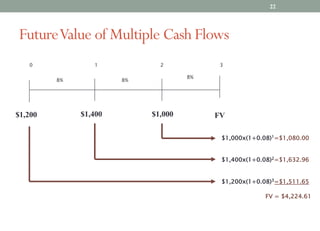

Future Value ofMultiple Cash Flows

• Example:

You deposit $1,200 in your bank account today; $1,400 one year later;

and $1,000 two years from today. If your bank offers you an 8%

interest rate on your account, how much money will you have in the

account three years from today?

Multiple Cash Flows

20

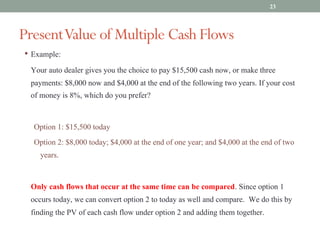

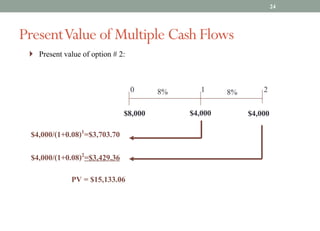

• Example:

Your autodealer gives you the choice to pay $15,500 cash now, or make three

payments: $8,000 now and $4,000 at the end of the following two years. If your cost

of money is 8%, which do you prefer?

Option 1: $15,500 today

Option 2: $8,000 today; $4,000 at the end of one year; and $4,000 at the end of two

years.

Only cash flows that occur at the same time can be compared. Since option 1

occurs today, we can convert option 2 to today as well and compare. We do this by

finding the PV of each cash flow under option 2 and adding them together.

PresentValue of Multiple Cash Flows

23

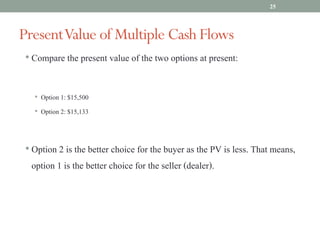

• Compare thepresent value of the two options at present:

• Option 1: $15,500

• Option 2: $15,133

• Option 2 is the better choice for the buyer as the PV is less. That means,

option 1 is the better choice for the seller (dealer).

PresentValue of Multiple Cash Flows

25

24.

• Annuities: Cashflows of equal amount every period for a limited

number of periods (finite).

• Example: Loan payments for automobile, periodic earnings from lottery wins, etc.

• Regular Annuity

• Annuity Due

• Perpetuities: Cash flows of equal amount every period for an unlimited

number of periods (infinite).

• Example: Property tax payments, preferred stocks, etc.

• Regular Perpetuity

• Perpetuity Due

Level Cash Flows:Perpetuities andAnnuities

26

25.

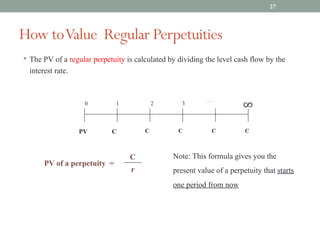

• The PVof a regular perpetuity is calculated by dividing the level cash flow by the

interest rate.

PV of a perpetuity =

C

r

0 1 3

2 …….

∞

C

C

C

C

C

Note: This formula gives you the

present value of a perpetuity that starts

one period from now

PV

How toValue Regular Perpetuities

27

26.

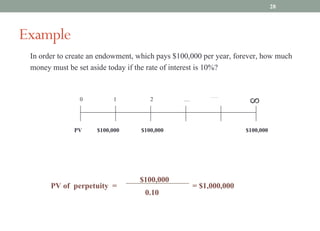

In order tocreate an endowment, which pays $100,000 per year, forever, how much

money must be set aside today if the rate of interest is 10%?

PV of perpetuity =

$100,000

0.10

0 1 …

2 …….

∞

$100,000

PV $100,000 $100,000

= $1,000,000

Example

28

27.

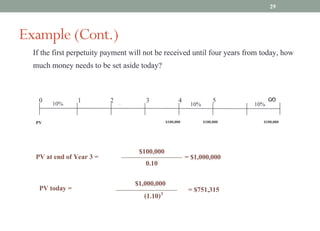

If the firstperpetuity payment will not be received until four years from today, how

much money needs to be set aside today?

PV at end of Year 3 =

$100,000

0.10

1 2 4

3 5 ∞

10% 10% 10%

$100,000

PV $100,000 $100,000

= $1,000,000

…

PV today = $1,000,000

(1.10)3 = $751,315

0

Example (Cont.)

29

28.

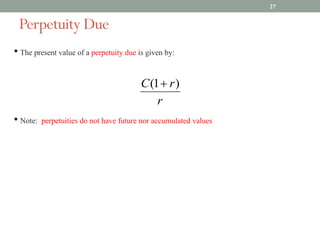

Perpetuity Due

27

• Thepresent value of a perpetuity due is given by:

• Note: perpetuities do not have future nor accumulated values

29.

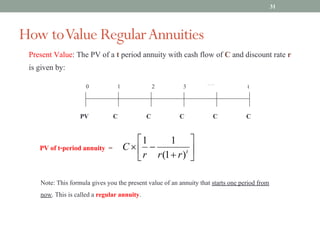

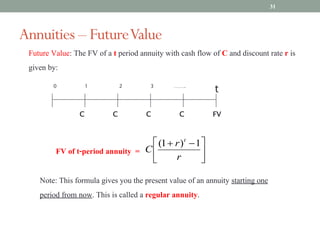

Present Value: ThePV of a t period annuity with cash flow of C and discount rate r

is given by:

PV of t-period annuity =

0 1 3

2 …….

t

C

C

C

C

C

PV

Note: This formula gives you the present value of an annuity that starts one period from

now. This is called a regular annuity.

How toValue RegularAnnuities

ú

û

ù

ê

ë

é

+

-

´ t

r

r

r

C

)

1

(

1

1

31

30.

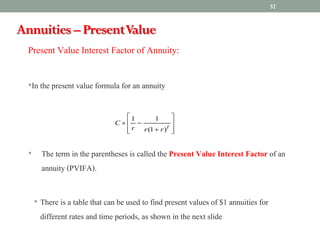

Present Value InterestFactor of Annuity:

•In the present value formula for an annuity

• The term in the parentheses is called the Present Value Interest Factor of an

annuity (PVIFA).

• There is a table that can be used to find present values of $1 annuities for

different rates and time periods, as shown in the next slide

ú

ú

û

ù

ê

ê

ë

é

+

-

´

t

r

r

r

C

)

1

(

1

1

Annuities – PresentValue

32

31.

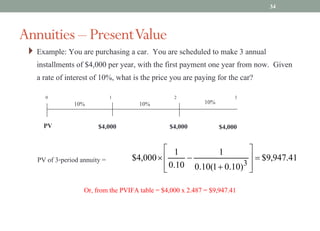

} Example: Youare purchasing a car. You are scheduled to make 3 annual

installments of $4,000 per year, with the first payment one year from now. Given

a rate of interest of 10%, what is the price you are paying for the car?

0 1 2

$4,000

10%

$4,000

10%

$4,000

3

10%

PV of 3-period annuity = 41

.

947

,

9

$

)

10

.

0

1

(

10

.

0

1

10

.

0

1

000

,

4

$

3

=

ú

ú

û

ù

ê

ê

ë

é

+

-

´

Or, from the PVIFA table = $4,000 x 2.487 = $9,947.41

Annuities – PresentValue

PV

34

32.

Future Value: TheFV of a t period annuity with cash flow of C and discount rate r is

given by:

0 1 3

2 …….

t

FV

C

C

C

C

FV of t-period annuity =

Note: This formula gives you the present value of an annuity starting one

period from now. This is called a regular annuity.

Annuities – FutureValue

ú

û

ù

ê

ë

é -

+

r

r

C

t

1

)

1

(

31

33.

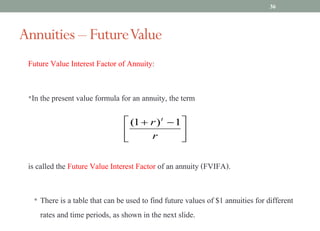

Future Value InterestFactor of Annuity:

•In the present value formula for an annuity, the term

is called the Future Value Interest Factor of an annuity (FVIFA).

• There is a table that can be used to find future values of $1 annuities for different

rates and time periods, as shown in the next slide.

Annuities – FutureValue

ú

û

ù

ê

ë

é -

+

r

r t

1

)

1

(

36

34.

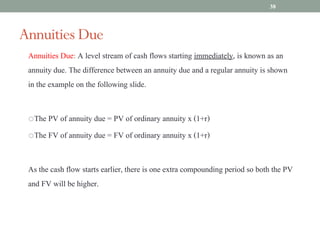

Annuities Due: Alevel stream of cash flows starting immediately, is known as an

annuity due. The difference between an annuity due and a regular annuity is shown

in the example on the following slide.

oThe PV of annuity due = PV of ordinary annuity x (1+r)

oThe FV of annuity due = FV of ordinary annuity x (1+r)

As the cash flow starts earlier, there is one extra compounding period so both the PV

and FV will be higher.

Annuities Due

38

35.

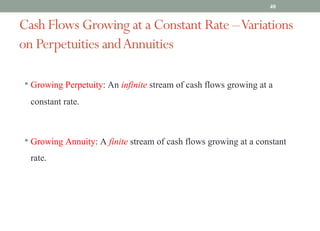

Cash Flows Growingat a Constant Rate –Variations

on Perpetuities andAnnuities

• Growing Perpetuity: An infinite stream of cash flows growing at a

constant rate.

• Growing Annuity: A finite stream of cash flows growing at a constant

rate.

40

36.

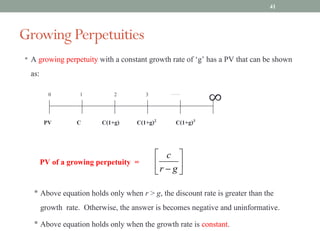

• A growingperpetuity with a constant growth rate of ‘g’ has a PV that can be shown

as:

• Above equation holds only when r > g, the discount rate is greater than the

growth rate. Otherwise, the answer is becomes negative and uninformative.

• Above equation holds only when the growth rate is constant.

0 1 3

2 …….

∞

C(1+g)3

C(1+g)2

C(1+g)

C

PV

PV of a growing perpetuity =

Growing Perpetuities

ú

û

ù

ê

ë

é

- g

r

c

41

37.

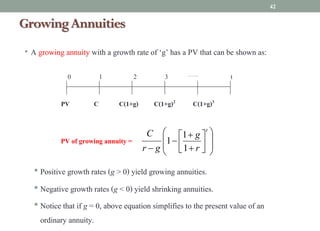

• A growingannuity with a growth rate of ‘g’ has a PV that can be shown as:

• Positive growth rates (g > 0) yield growing annuities.

• Negative growth rates (g < 0) yield shrinking annuities.

• Notice that if g = 0, above equation simplifies to the present value of an

ordinary annuity.

0 1 3

2 ……. t

C(1+g)3

C(1+g)2

C(1+g)

C

PV

÷

÷

ø

ö

ç

ç

è

æ

ú

û

ù

ê

ë

é

+

+

-

-

t

r

g

g

r

C

1

1

1

GrowingAnnuities

PV of growing annuity =

42

38.

GrowingAnnuities

37

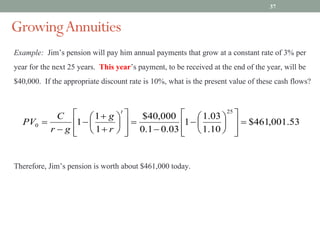

Example: Jim’s pensionwill pay him annual payments that grow at a constant rate of 3% per

year for the next 25 years. This year’s payment, to be received at the end of the year, will be

$40,000. If the appropriate discount rate is 10%, what is the present value of these cash flows?

Therefore, Jim’s pension is worth about $461,000 today.

53

.

001

,

461

$

10

.

1

03

.

1

1

03

.

0

1

.

0

000

,

40

$

1

1

1

25

0 =

ú

ú

û

ù

ê

ê

ë

é

÷

ø

ö

ç

è

æ

-

-

=

ú

ú

û

ù

ê

ê

ë

é

÷

ø

ö

ç

è

æ

+

+

-

-

=

t

r

g

g

r

C

PV

39.

ShrinkingAnnuities

38

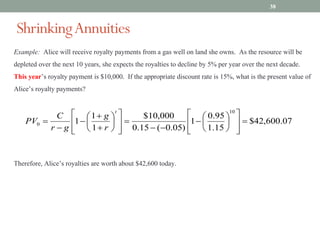

Example: Alice willreceive royalty payments from a gas well on land she owns. As the resource will be

depleted over the next 10 years, she expects the royalties to decline by 5% per year over the next decade.

This year’s royalty payment is $10,000. If the appropriate discount rate is 15%, what is the present value of

Alice’s royalty payments?

Therefore, Alice’s royalties are worth about $42,600 today.

07

.

600

,

42

$

15

.

1

95

.

0

1

)

05

.

0

(

15

.

0

000

,

10

$

1

1

1

10

0 =

ú

ú

û

ù

ê

ê

ë

é

÷

ø

ö

ç

è

æ

-

-

-

=

ú

ú

û

ù

ê

ê

ë

é

÷

ø

ö

ç

è

æ

+

+

-

-

=

t

r

g

g

r

C

PV

40.

Annuity and Perpetuity(important remarks)

• While solving an annuity or perpetuity related problems, you need to consider the following

points:

• Are we dealing with an annuity or a perpetuity? or dealing with different cash flows falling at

distinct points in time?

• To qualify as an annuity or a perpetuity, the cash flows should be equal or growing at

constant rate (g) or falling at the same interval

• If the cash flows do not form an annuity or a perpetuity, then we should discount each

cash flow independently

• Are we dealing with ordinary or due series?

• For an annuity, what is t?

• The interest rate should be the effective interest rate for the period separating two cash flows

(two payments)

• What is an effective interest rate?

39

41.

NominalVersus Effective Rates

•Effective rate for a period is the actual rate at which a dollar invested grows over

that period (e.g., daily, monthly, quarterly, Annual etc.)

• For annual period, we have Effective Annual Rate (EAR)

• Nominal interest rate, quoted rate, or Annual Percentage Rate (APR) is an

interest rate that does not include any consideration of compounding

• Usually, the nominal rate is a yearly rate except that other period is mentioned in

a problem

• What should we do with nominal rates? Convert it to effective rates

40

42.

NominalVersus Effective Rates(Cont’d)

The followings are nominal rate statements:

Nominal Rate (Qr) Time Period (t) Compounding Period

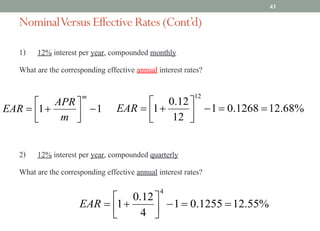

1) 12% interest per year, compounded monthly

2) 12% interest per year, compounded quarterly

3) 3% interest per quarter, compounded monthly

What are the corresponding effective annual interest rates?

41

43.

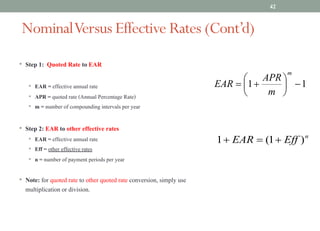

NominalVersus Effective Rates(Cont’d)

• Step 1: Quoted Rate to EAR

• EAR = effective annual rate

• APR = quoted rate (Annual Percentage Rate)

• m = number of compounding intervals per year

• Step 2: EAR to other effective rates

• EAR = effective annual rate

• Eff = other effective rates

• n = number of payment periods per year

• Note: for quoted rate to other quoted rate conversion, simply use

multiplication or division.

42

1

1 -

÷

ø

ö

ç

è

æ

+

=

m

m

APR

EAR

n

Eff

EAR )

1

(

1 +

=

+

44.

NominalVersus Effective Rates(Cont’d)

1) 12% interest per year, compounded monthly

What are the corresponding effective annual interest rates?

2) 12% interest per year, compounded quarterly

What are the corresponding effective annual interest rates?

43

1

1 -

ú

û

ù

ê

ë

é

+

=

m

m

APR

EAR %

68

.

12

1268

.

0

1

12

12

.

0

1

12

=

=

-

ú

û

ù

ê

ë

é

+

=

EAR

%

55

.

12

1255

.

0

1

4

12

.

0

1

4

=

=

-

ú

û

ù

ê

ë

é

+

=

EAR

45.

NominalVersus Effective Rates(Cont’d)

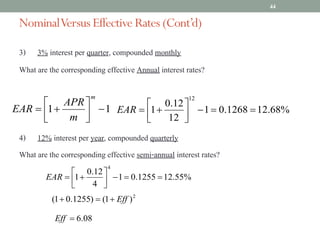

3) 3% interest per quarter, compounded monthly

What are the corresponding effective Annual interest rates?

4) 12% interest per year, compounded quarterly

What are the corresponding effective semi-annual interest rates?

44

1

1 -

ú

û

ù

ê

ë

é

+

=

m

m

APR

EAR %

68

.

12

1268

.

0

1

12

12

.

0

1

12

=

=

-

ú

û

ù

ê

ë

é

+

=

EAR

%

55

.

12

1255

.

0

1

4

12

.

0

1

4

=

=

-

ú

û

ù

ê

ë

é

+

=

EAR

2

)

1

(

)

1255

.

0

1

( Eff

+

=

+

08

.

6

=

Eff

46.

Comprehensive Example:

A BasicRetirement Problem

45

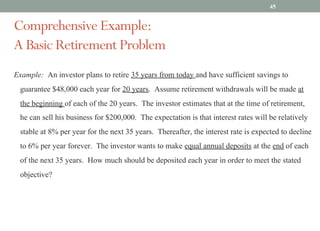

Example: An investor plans to retire 35 years from today and have sufficient savings to

guarantee $48,000 each year for 20 years. Assume retirement withdrawals will be made at

the beginning of each of the 20 years. The investor estimates that at the time of retirement,

he can sell his business for $200,000. The expectation is that interest rates will be relatively

stable at 8% per year for the next 35 years. Thereafter, the interest rate is expected to decline

to 6% per year forever. The investor wants to make equal annual deposits at the end of each

of the next 35 years. How much should be deposited each year in order to meet the stated

objective?

47.

Comprehensive Example:

A BasicRetirement Problem

46

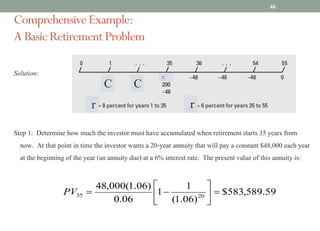

Solution:

Step 1: Determine how much the investor must have accumulated when retirement starts 35 years from

now. At that point in time the investor wants a 20-year annuity that will pay a constant $48,000 each year

at the beginning of the year (an annuity due) at a 6% interest rate. The present value of this annuity is:

59

.

589

,

583

$

)

06

.

1

(

1

1

06

.

0

)

06

.

1

(

000

,

48

20

35 =

ú

û

ù

ê

ë

é

-

=

PV

C C

C

r r

48.

Comprehensive Example:

A BasicRetirement Problem

47

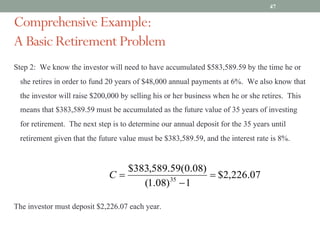

Step 2: We know the investor will need to have accumulated $583,589.59 by the time he or

she retires in order to fund 20 years of $48,000 annual payments at 6%. We also know that

the investor will raise $200,000 by selling his or her business when he or she retires. This

means that $383,589.59 must be accumulated as the future value of 35 years of investing

for retirement. The next step is to determine our annual deposit for the 35 years until

retirement given that the future value must be $383,589.59, and the interest rate is 8%.

The investor must deposit $2,226.07 each year.

07

.

226

,

2

$

1

)

08

.

1

(

)

08

.

0

(

59

.

589

,

383

$

35

=

-

=

C

![Compound Interest

• Value at the end of Year 1 = $100.00 +[$100 x 6%] = $100 x (1+r)

• Value at the end of Year 2 = $106.00 + [$106 x 6%] = $100 x (1+r)2

• …….

• Value at the end of Year 5 = $100 x (1+r)5

•The formula for the future value of PV dollars at r% interest per period for t periods

is:

FutureValues

t

r

PV

FV )

1

( +

´

=

7](https://image.slidesharecdn.com/topic21-250727063100-5963be13/85/International-Financial-Management-slides-pdf-7-320.jpg)