Download to read offline

![CASE Network Studies & Analyses No.450 – Macroeconomic Preconditions of the Realization...

29

Bibliography

Drobyshevsky S., Sinelnikov-Murylev S., Sokolov I. (2011). Evolutsia biudzhetnoi politiki

Rossii v 2000-e gody: v poiskakh finansovoi ustoichivosti natsionalnoi biudzhetnoi sistemy

[Drobyshevsky S., Sinelnikov-Murylev S., Sokolov I. (2011). Transformation of Budgetary

Policy in Russia during the 2000s: in Quest of National Fiscal Sustainability // Voprosy

Ekonomiki. No 1.]

Chouraqui J. C., Hagemann R., Sartor N. (l990). Indicators of Fiscal Policy: A Reexamination

// OECD Economics and Statistics Department Working Paper. No 78.

Giorno C., Richardson P., Roseveare D., Noord P. van den (1995). Estimating Potential

Output, Output Gaps and Structural Budget Balances // OECD Economics Department

Working Paper. No 152.

Maddala G. S., In-Moo Kim (1999). Unit Roots, Cointegration, and Structural Change.

Cambridge: Cambridge University Press.

Nelson Ch., Plosser Ch. (1982). Trends and Random Walks in Macroeconomic Time Series:

Some Evidence and Implications // Journal of Monetary Economics. Vol. 10, No 2. P. 139—

162.](https://image.slidesharecdn.com/cnsa2013450-141023072819-conversion-gate02/75/CASE-Network-Studies-and-Analyses-450-Macroeconomic-Preconditions-of-the-Realization-of-a-New-Growth-Model-30-2048.jpg)

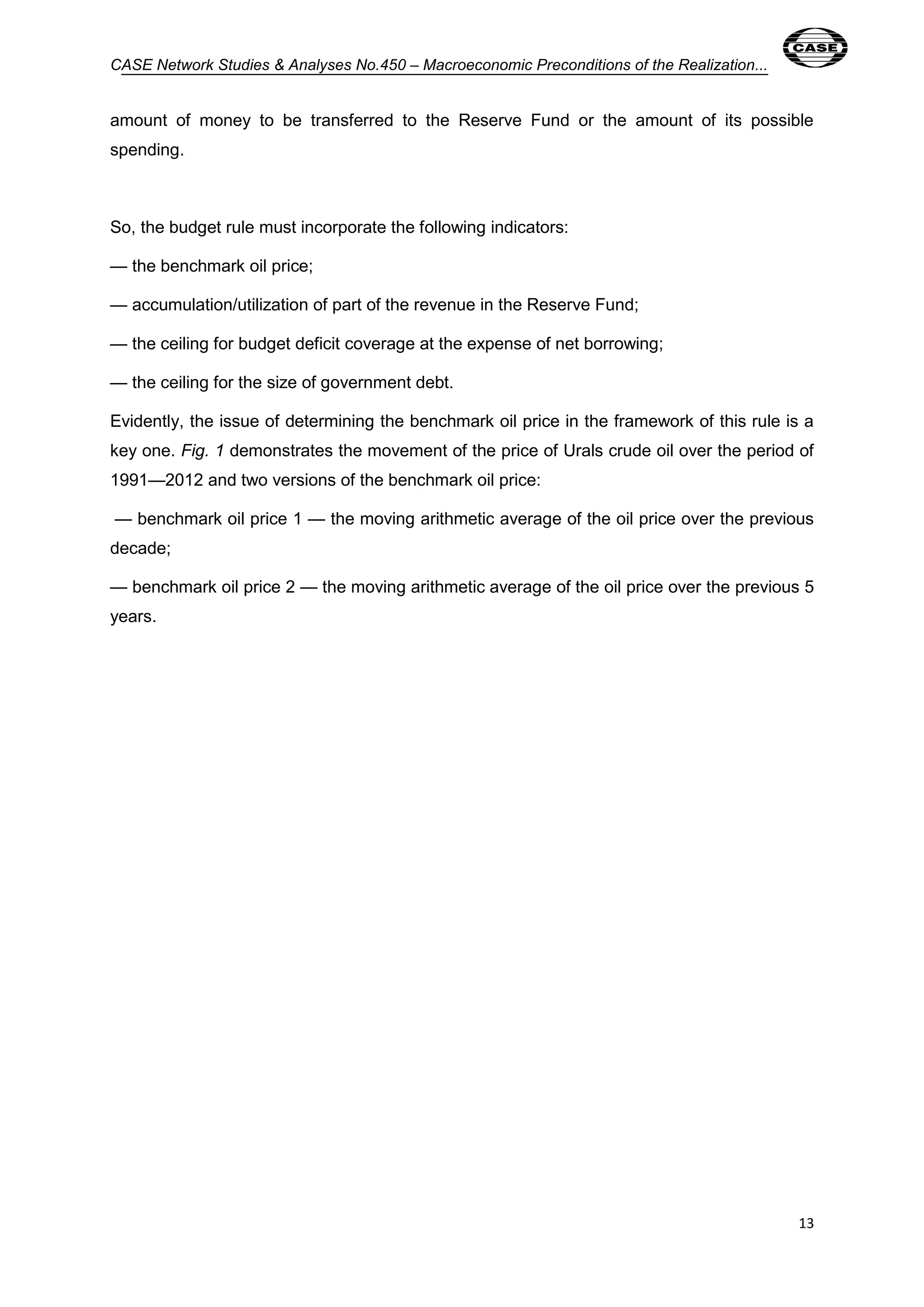

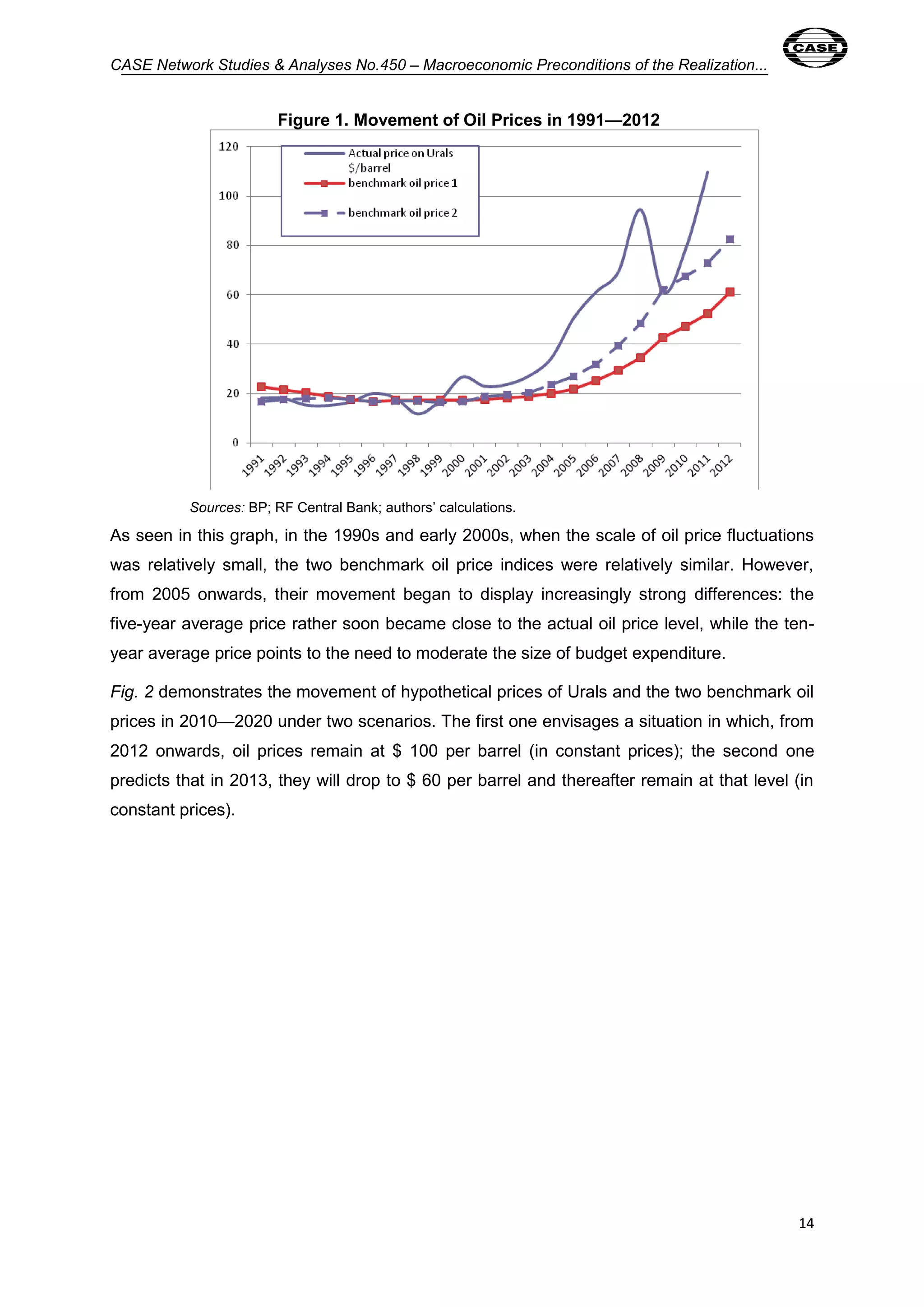

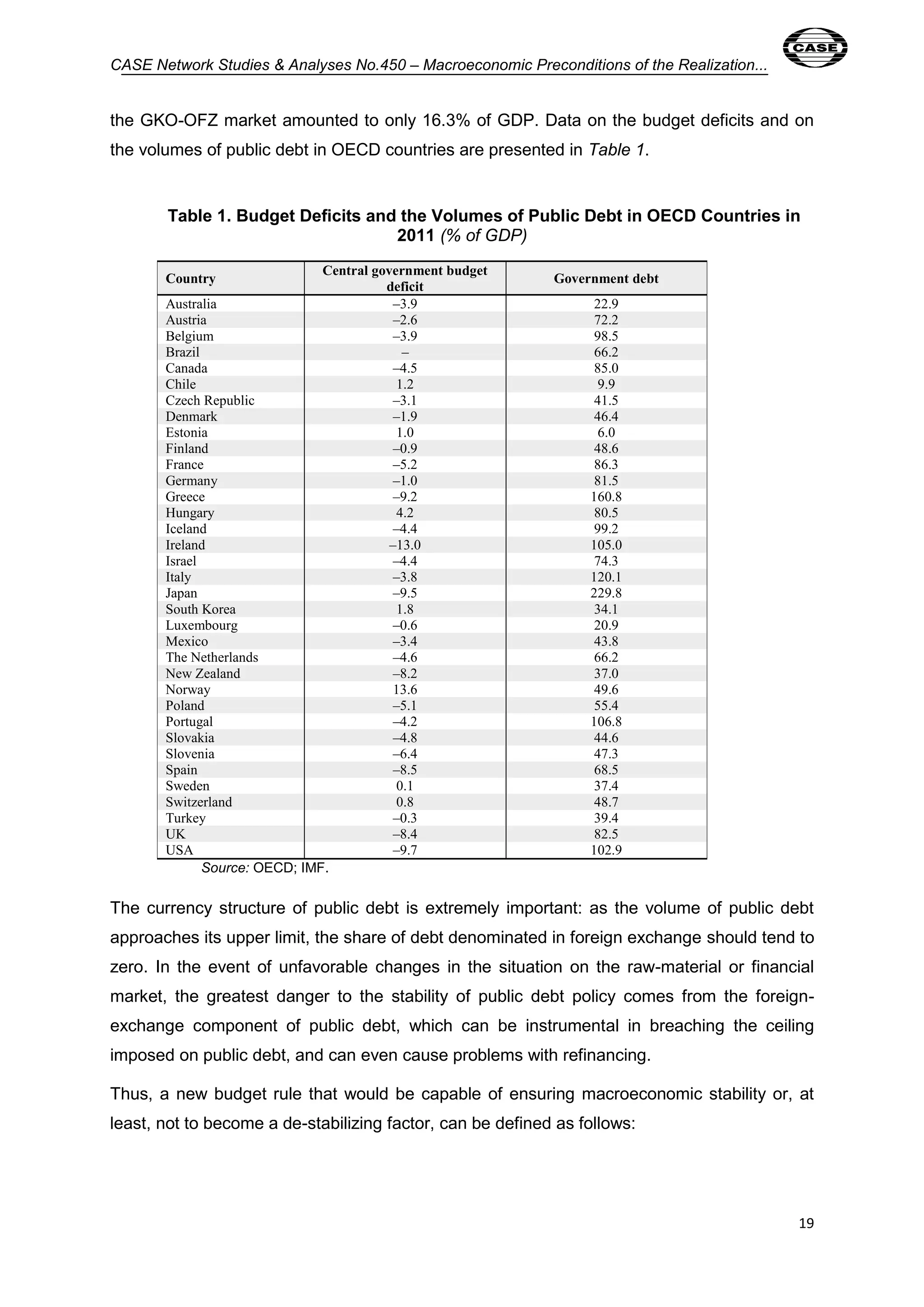

This document discusses macroeconomic preconditions for a new model of economic growth in Russia. It argues that Russia needs stable macroeconomic policies, especially in the areas of fiscal and monetary policy. For fiscal policy, it proposes a "New Budget Rule" based on long-term average oil prices to determine sustainable budget levels. It also advocates for monetary policy focused on low, stable inflation through inflation targeting. Overall, the document examines how macroeconomic stability can help Russia transition to a more diversified, productive economy and ensure continued development.