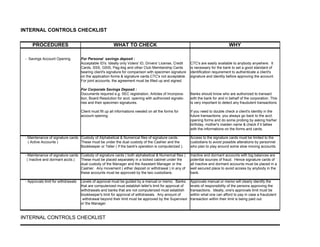

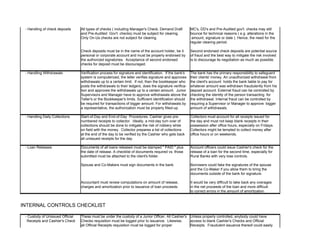

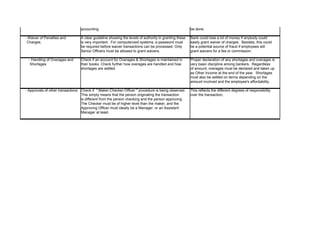

This internal controls checklist summarizes procedures that a bank should follow to properly manage accounts, transactions, and protect against fraud. Key points include: - Requiring proper identification for account openings and maintaining signature cards in secure storage. - Establishing approval limits for tellers, bookkeepers, and managers for withdrawals and other transactions. - Ensuring proper verification and endorsement of check deposits and following clearing periods. - Having collectors account for all receipts issued and turn over daily collections to mitigate robbery risks. - Reviewing loan release documents and amounts to prevent duplicate issuances or errors. - Maintaining custody over unissued receipts and checks and logging all requisitions for proper accounting