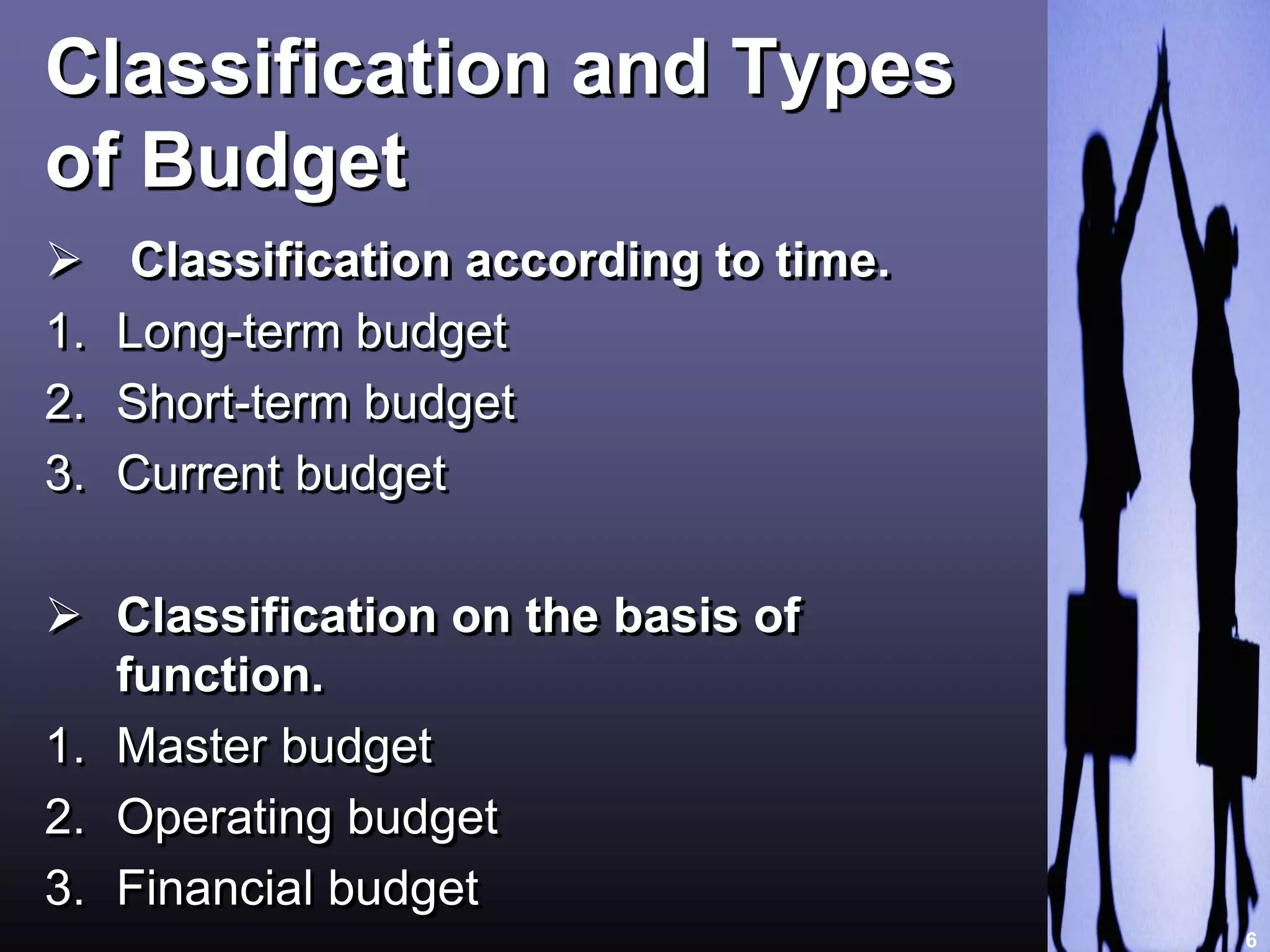

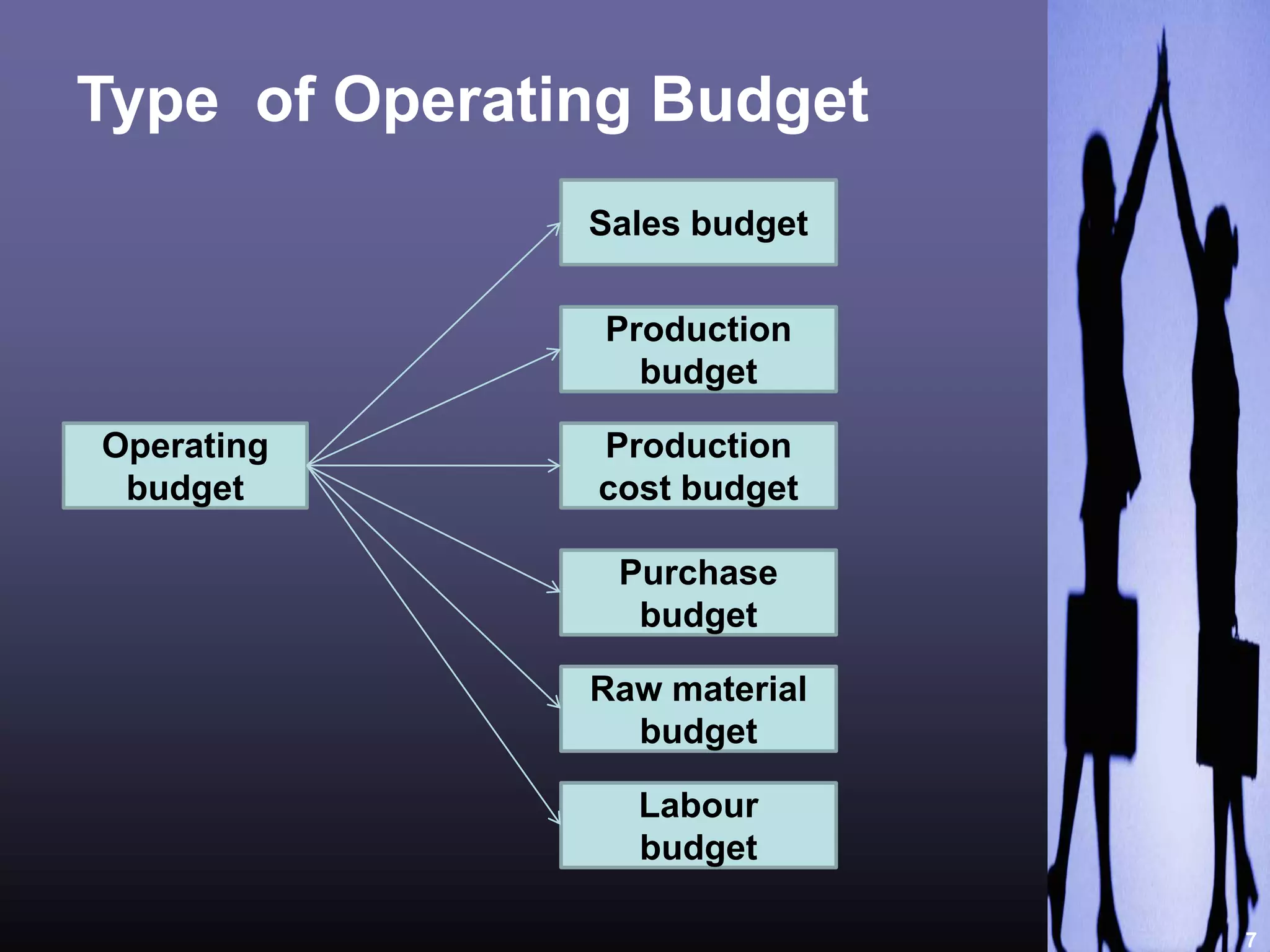

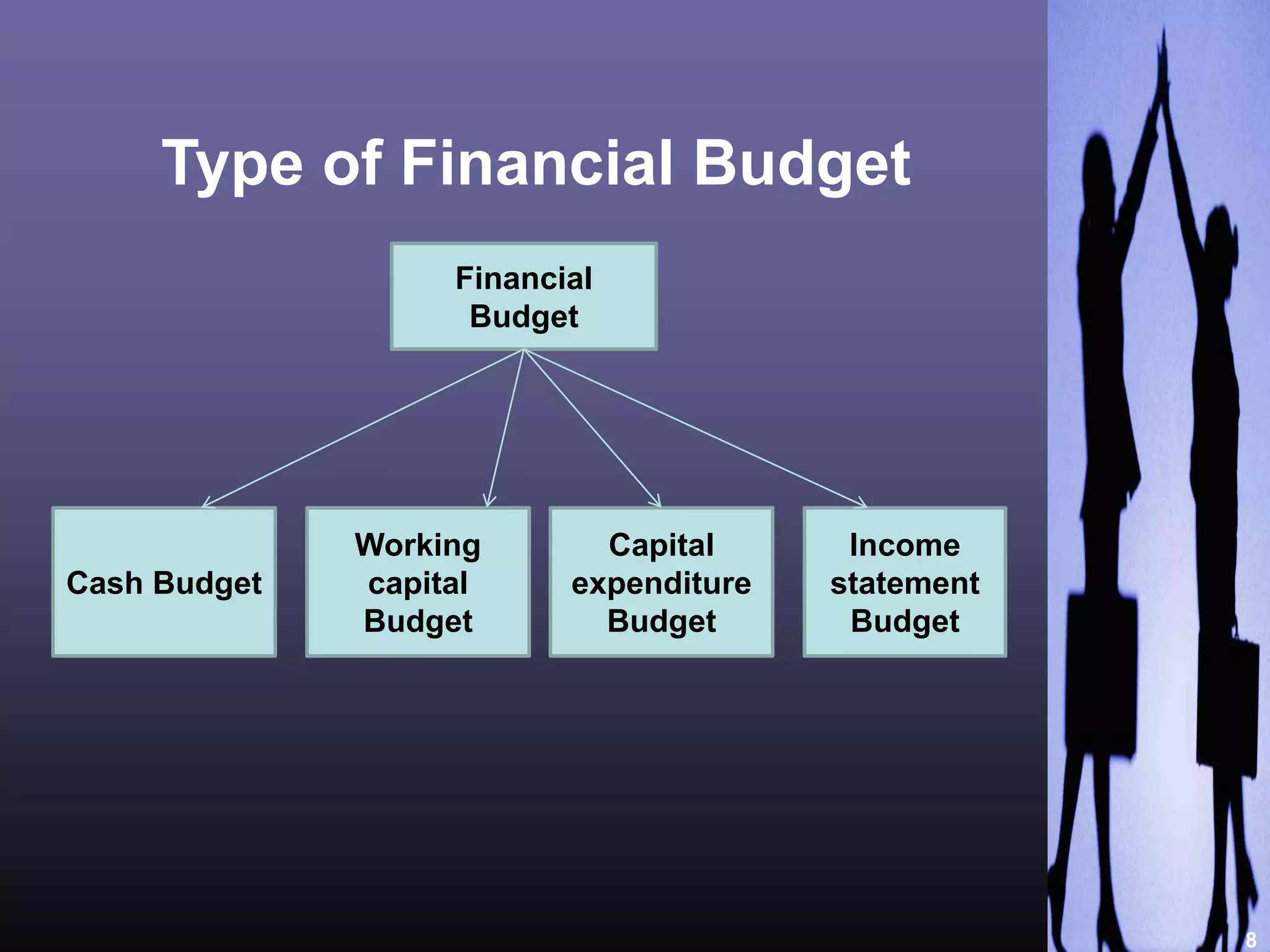

This document provides an overview of budgets, including their meaning, purpose, types, advantages, and limitations. It defines a budget as a financial plan that lists all revenues and expenses. Budgets are prepared annually by the Indian government. They serve several purposes, such as controlling resources, communicating plans, motivating managers, and evaluating performance. Budgets can be classified by time period (long, short, current) or function (master, operating, financial). The document also outlines the various types of operating and financial budgets. Advantages of budgets include aiding decision making and promoting specialization. Limitations are that budgets only provide estimates and can be inflexible.