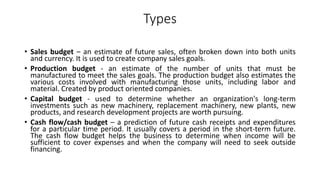

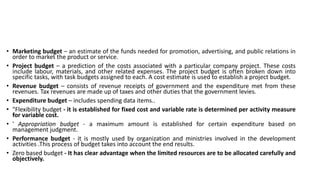

Budgets are financial plans that express the strategic goals of organizations in measurable terms. They allocate money for specific purposes and summarize intended expenditures and revenue sources. Budgets help managers plan operations, coordinate activities between departments, motivate goal achievement, and evaluate performance. The main purposes of budgets are to forecast finances, measure actual performance against forecasts, and establish cost constraints. Common types of budgets include sales, production, capital, cash flow, marketing, project, revenue, expenditure, and zero-based budgets.