Download as PDF, PPTX

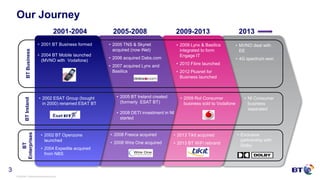

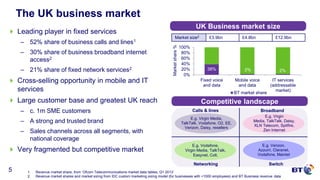

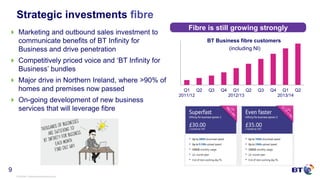

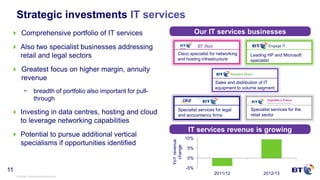

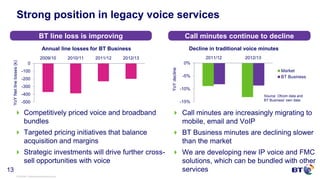

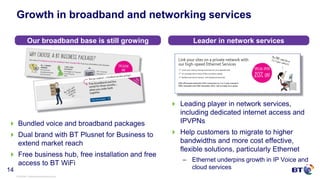

This document provides an overview of BT Business, the business-to-business division of BT Group plc. It discusses BT Business' market context and strategic investments in areas like fiber broadband, mobile services, IT services, and conferencing. It also describes BT Business' organizational structure, sales channels in the UK and Ireland, and presents a case study of providing services to Anchor Trust, a UK housing and care provider. The key messages are that BT Business is a leading UK provider of fixed telecom services to SMEs and mid-market companies, and it aims to leverage this position to drive growth in mobile and IT services through strategic investments and improved customer service.