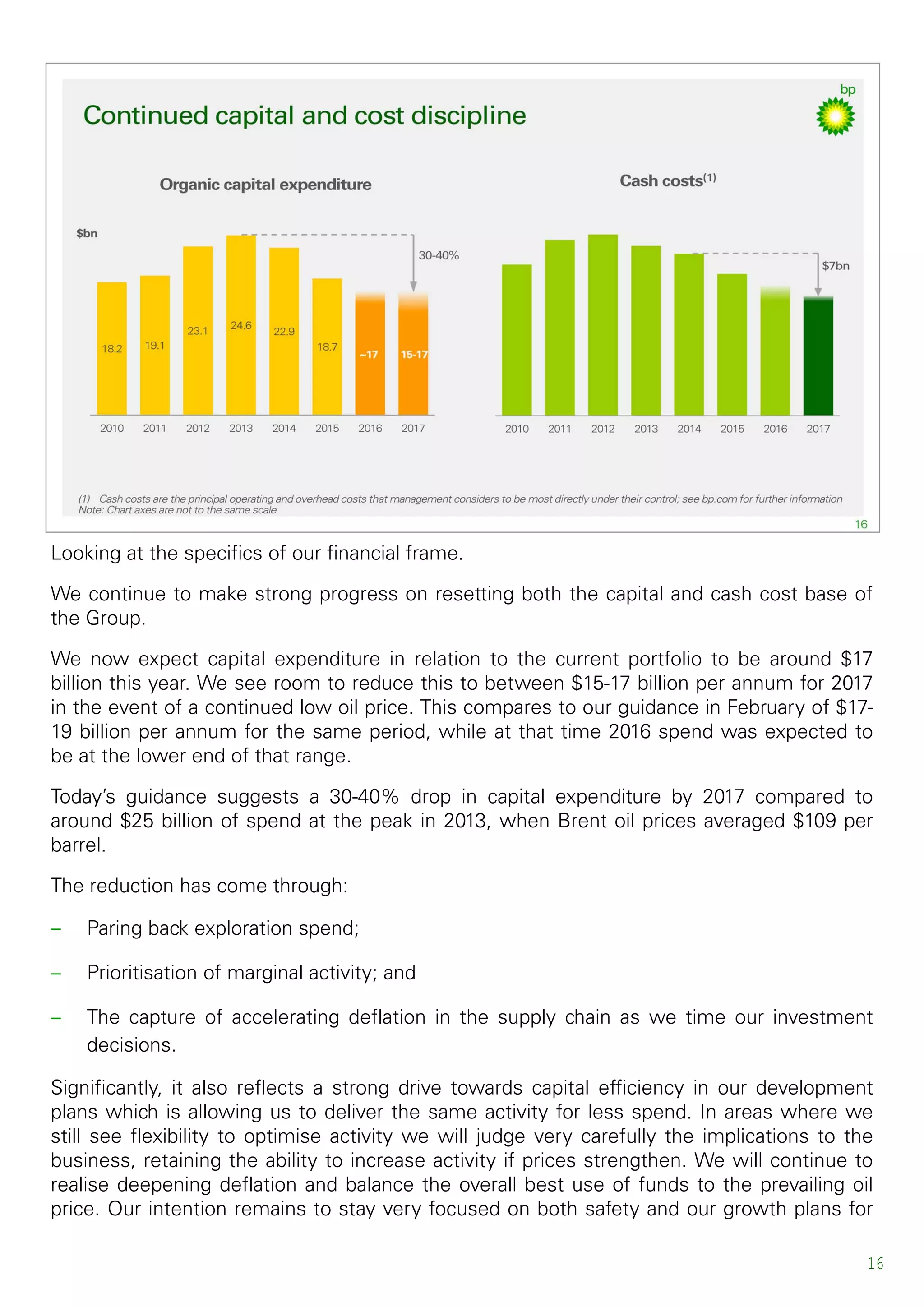

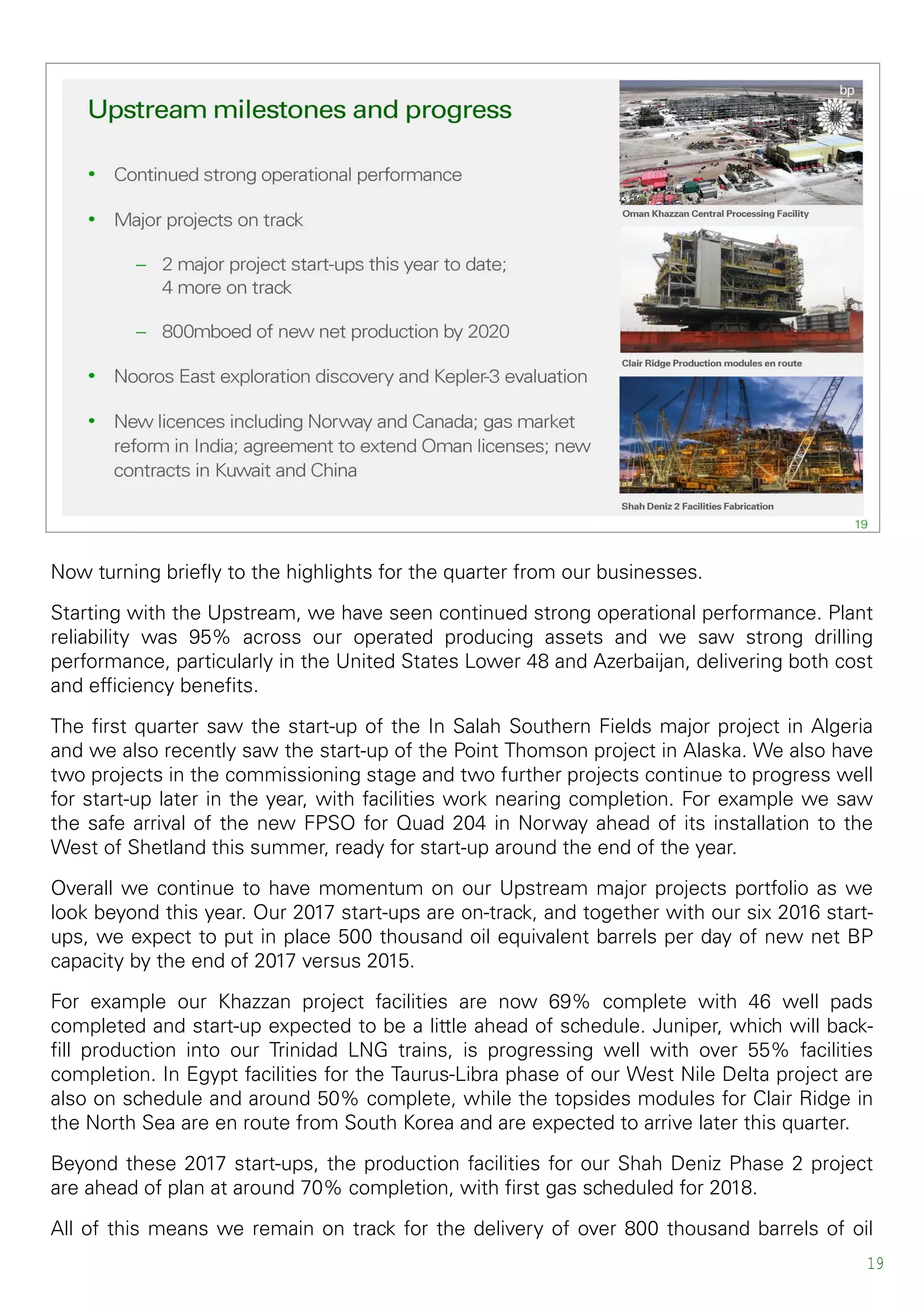

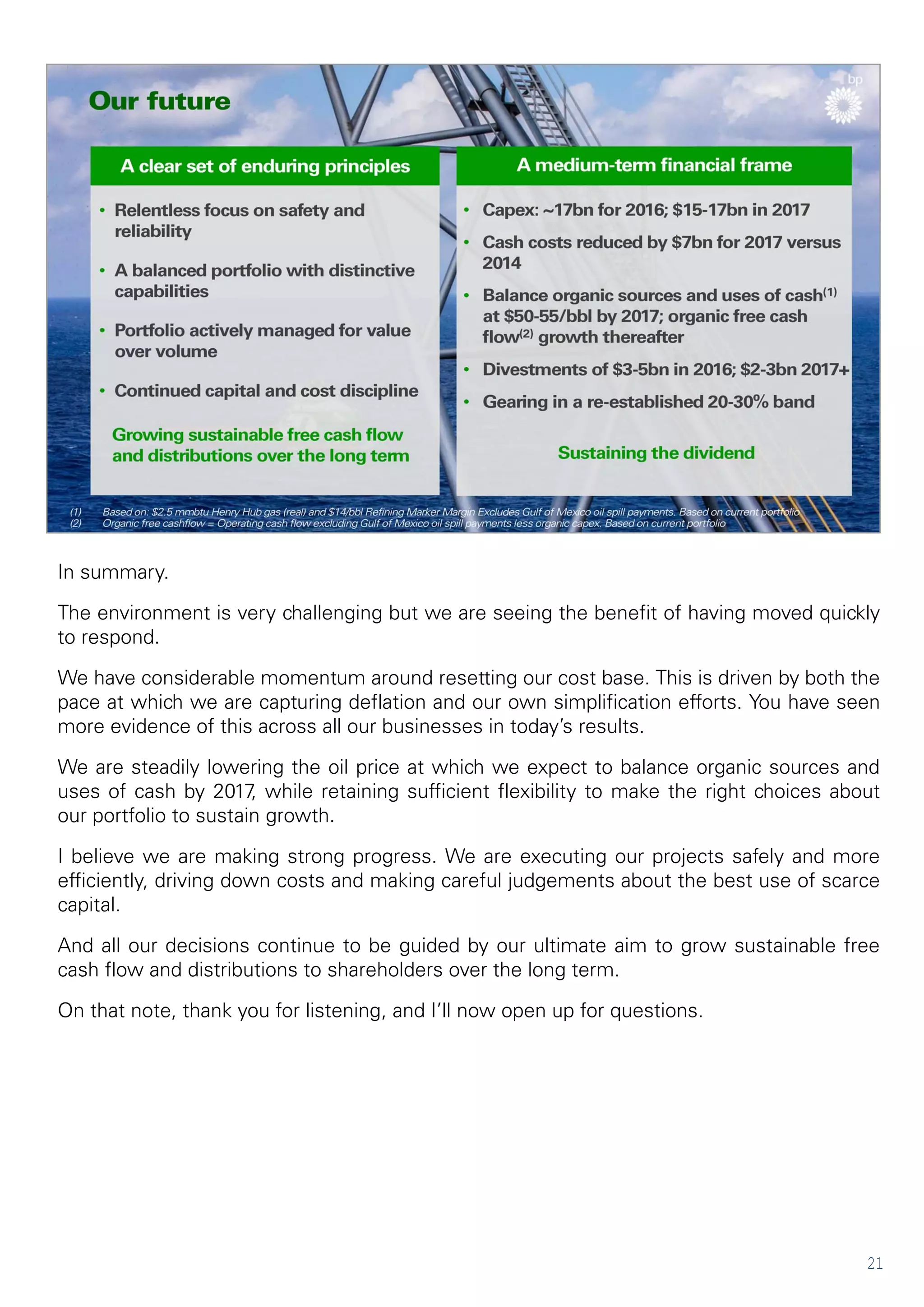

Download to read offline

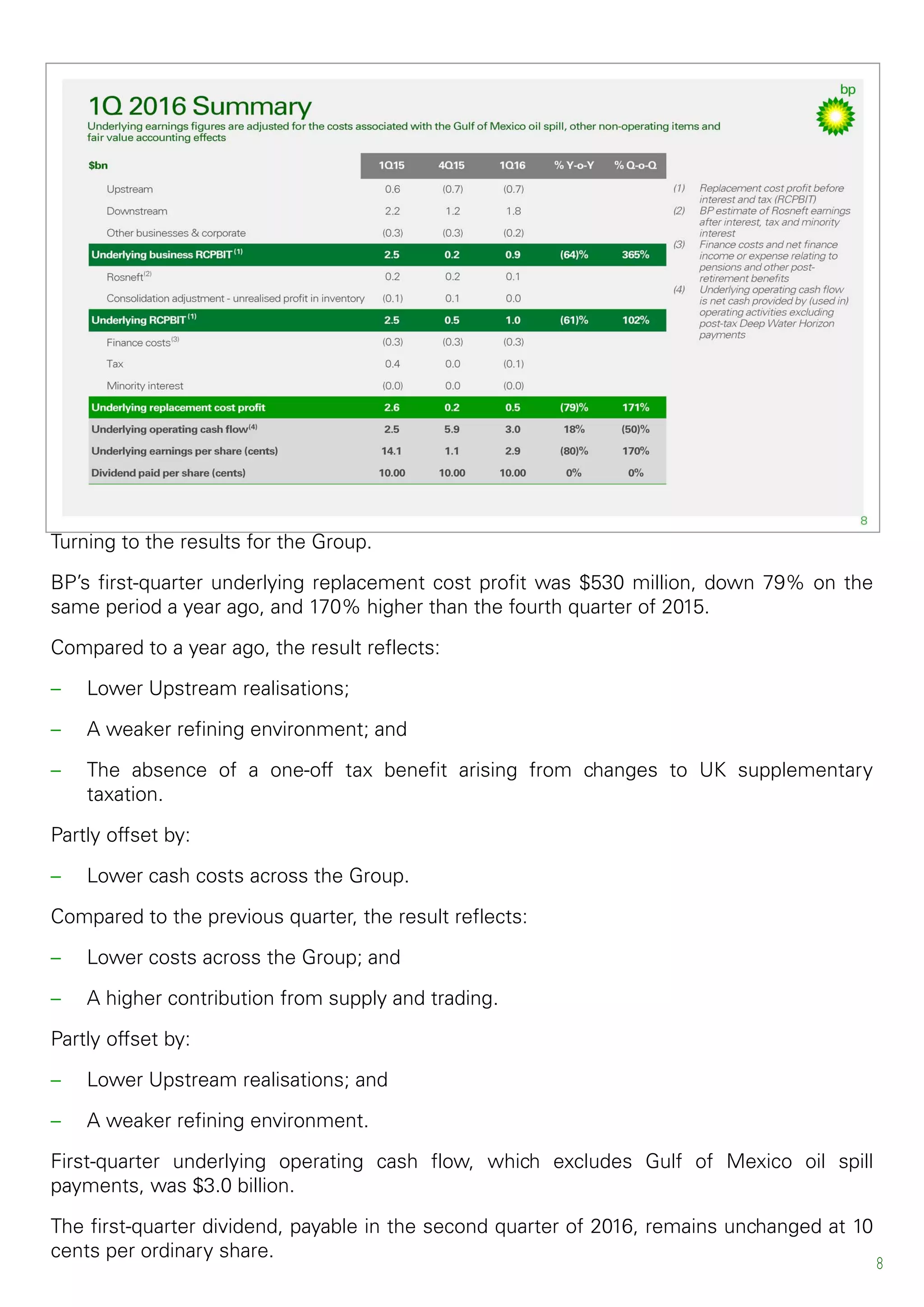

This document provides a summary of BP's first quarter 2016 results webcast and conference call. It includes an introduction by Jess Mitchell, Head of Investor Relations, and Brian Gilvary, Chief Financial Officer. Gilvary discusses BP's financial results for the first quarter, including lower underlying replacement cost profit of $530 million due to a weaker price environment. He also provides updates on BP's cost reduction progress, capital expenditure plans, and expectations for balancing organic cash flows by 2017 at oil prices of $50-55 per barrel.