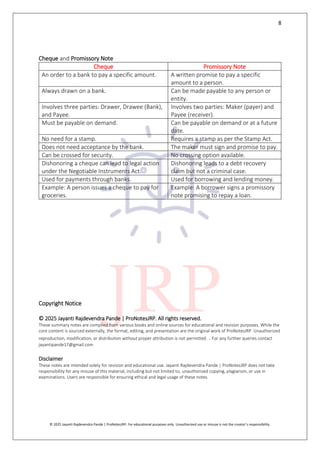

RTMNU BBA | Business Law | Sem 2 and Sem 6 NEP | Summary Notes | Unit 2 | INegotiable Instruments Act 1881| By Jayanti Pande | ProNotesJRP

![World Tread Organization [WTO] Overview.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wtooverview-241001053045-33bcac85-thumbnail.jpg?width=640&height=640&fit=bounds)