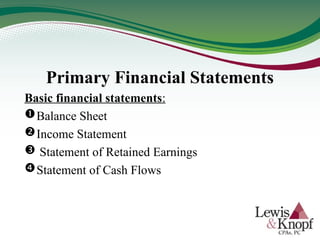

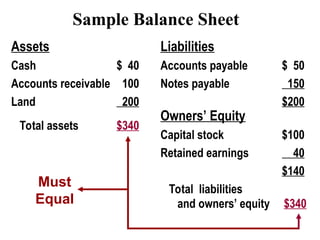

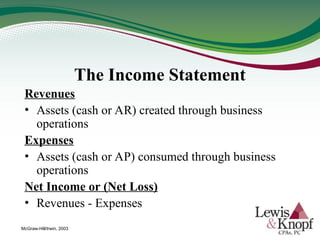

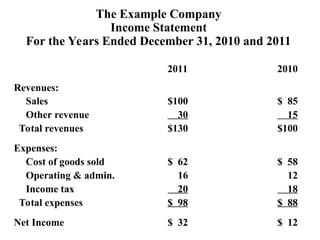

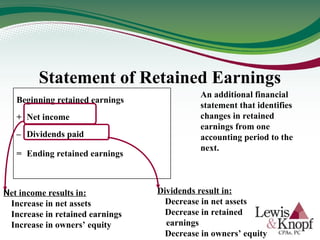

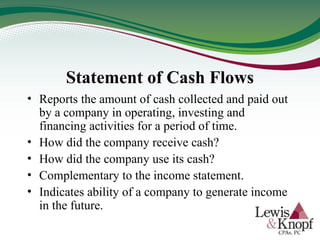

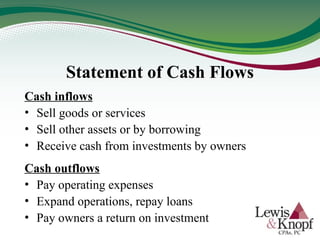

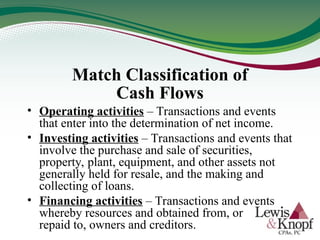

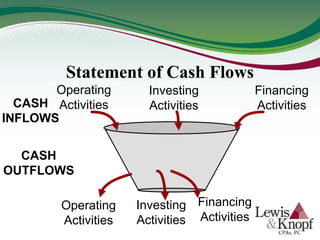

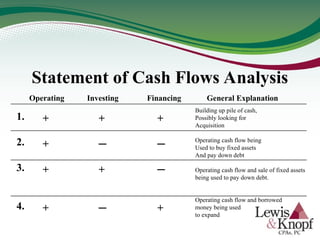

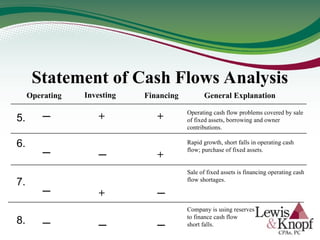

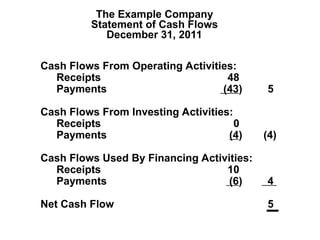

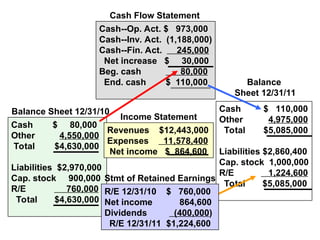

The document provides an overview of basic financial statements, including the balance sheet, income statement, statement of retained earnings, and statement of cash flows, along with their purposes and components. It emphasizes the importance of understanding these statements for analyzing a company's financial health and making informed decisions. Additionally, it discusses key accounting concepts such as accrual accounting, financial statement analysis tools, and methods for evaluating business performance.