Download as PDF, PPTX

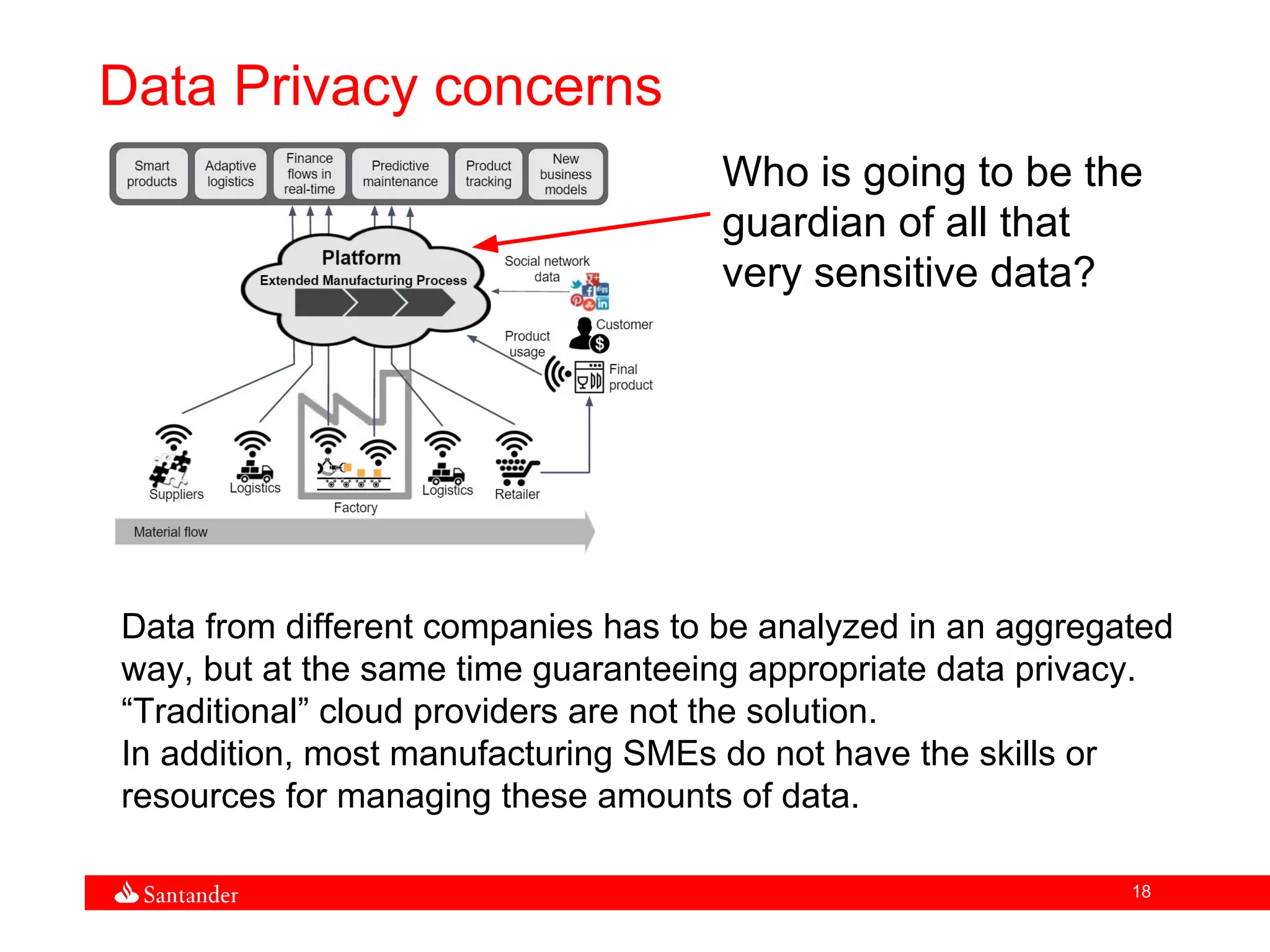

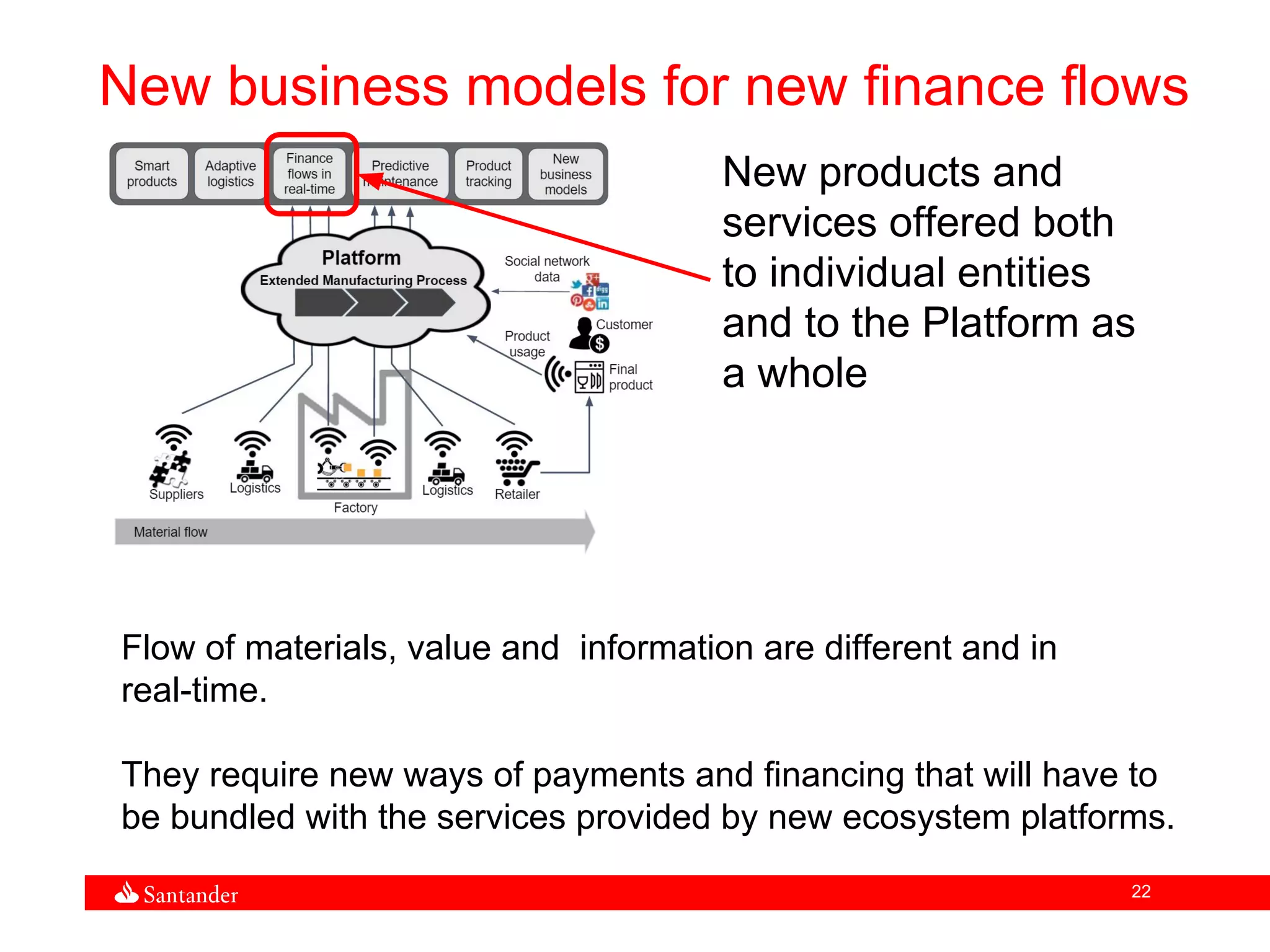

The document discusses how the Fourth Industrial Revolution, driven by technologies like the Internet of Things, big data, machine learning and 3D printing, will transform industries and require new approaches to financing. It notes that Industry 4.0 will create new flows of materials, value and information in real-time between suppliers, factories, logistics providers and customers. This will necessitate new forms of payments and financing that are bundled with the services provided by new industry platforms. The document concludes that banks must determine new business models beyond purely financial services and partnerships to help all participants in the new economy prosper.