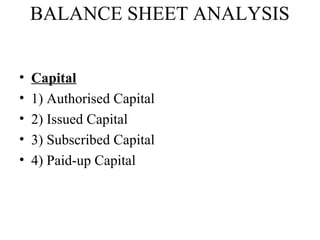

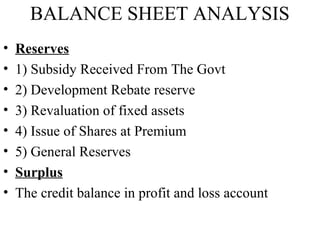

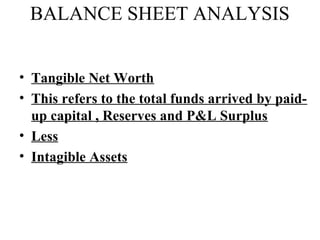

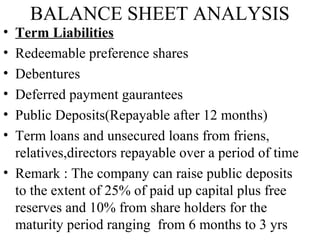

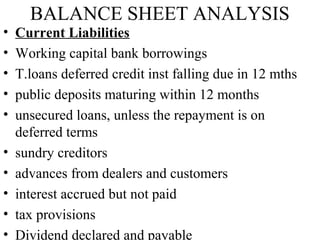

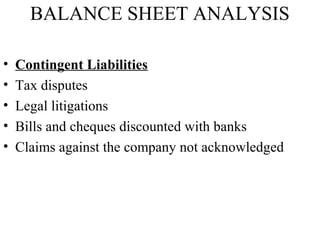

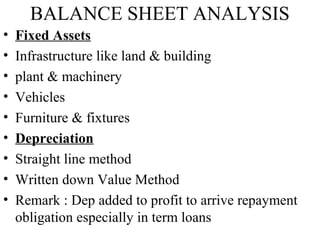

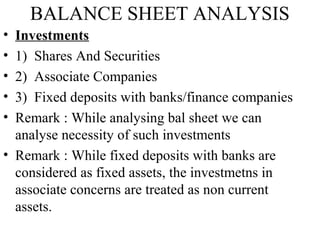

This document provides an overview and definitions for key items in a balance sheet and profit and loss statement analysis. It discusses sources of funds like capital, reserves, and liabilities. It also discusses uses of funds such as fixed assets, current assets, and intangible assets. Key items in the profit and loss statement are also defined like gross profit, operating profit, net profit, and non-operating income and expenses. Notes are provided on interpreting and qualifying balance sheet and profit and loss statement analyses.