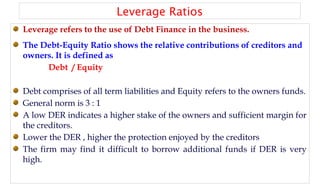

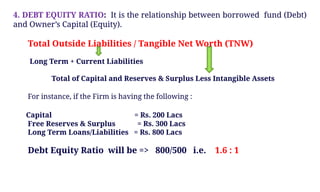

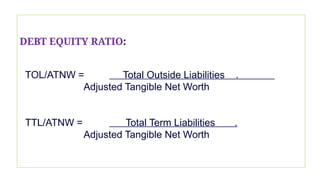

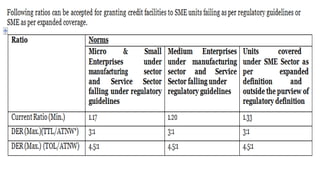

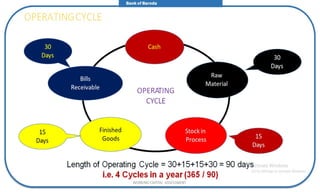

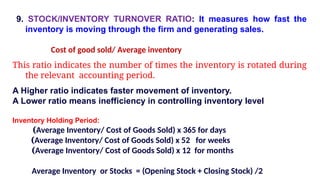

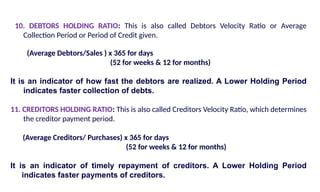

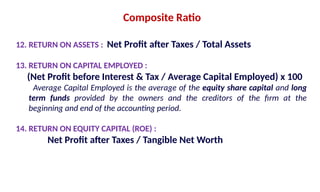

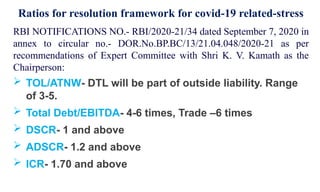

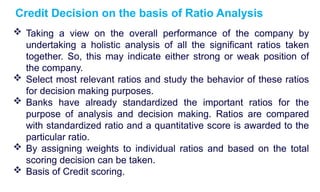

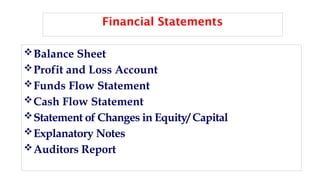

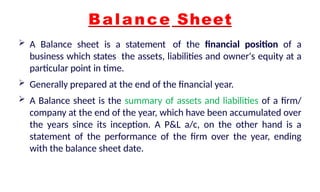

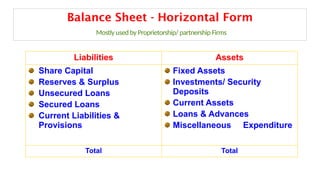

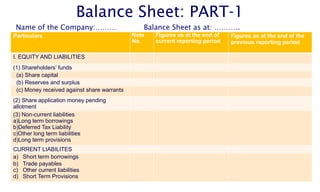

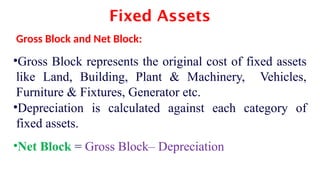

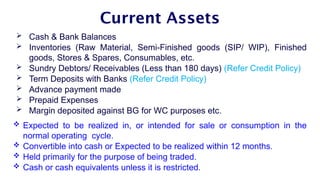

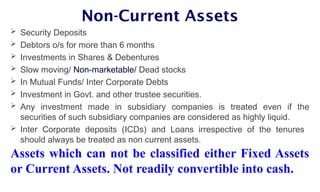

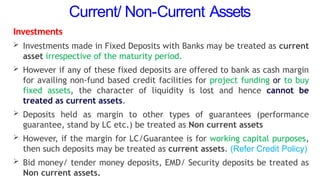

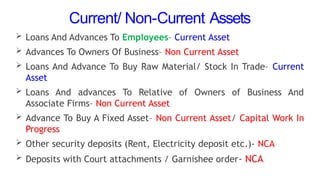

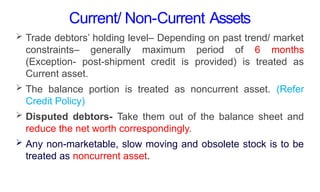

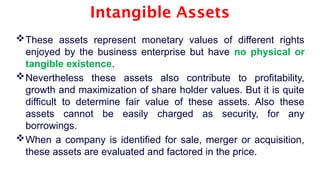

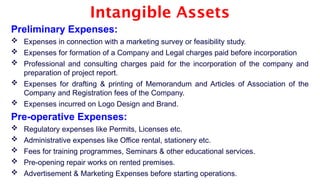

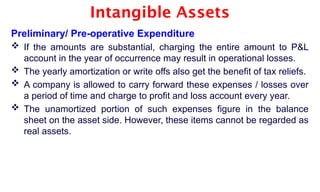

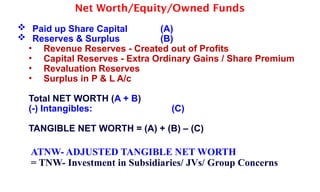

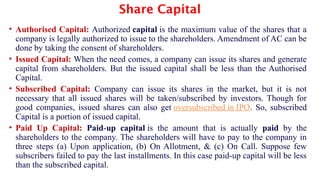

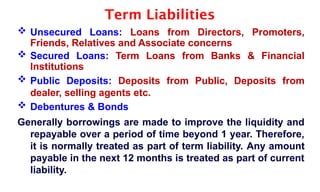

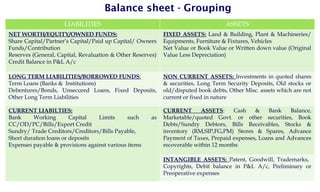

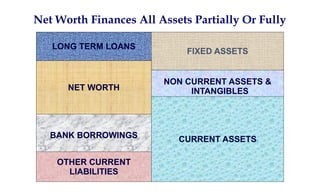

The document provides a comprehensive overview of financial statement analysis, focusing on balance sheets and profit and loss accounts, including their structures, classifications, and interpretation of financial ratios. It explains the components of liabilities and assets, differentiates between current and non-current items, and highlights the importance of accurate financial analysis for various stakeholders. Additionally, it discusses the necessity of audits and the objectives of ratio analysis in evaluating a firm's performance and financial health.

![• Income Net Sales (Sales minus Excise Duty)

Other Income (Net of other Expenses)

• Expenditure Material & other Expenditure

Interest

Depreciation

• Profit before tax

Provision for Tax

• Profit after Tax [PAT] –

• Profit available for appropriations

Dividend

General Reserve

Surplus carried to B/S.

Format of Profit & Loss Account](https://image.slidesharecdn.com/bsandratios-240909170432-2e8c871e/85/Balance-Sheet-components-and-Ratio-Analysis-pptx-34-320.jpg)