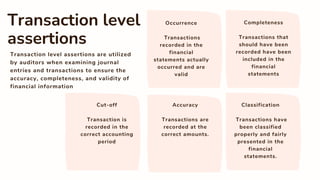

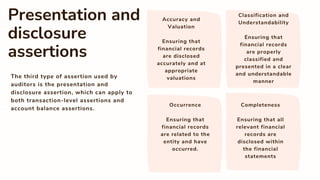

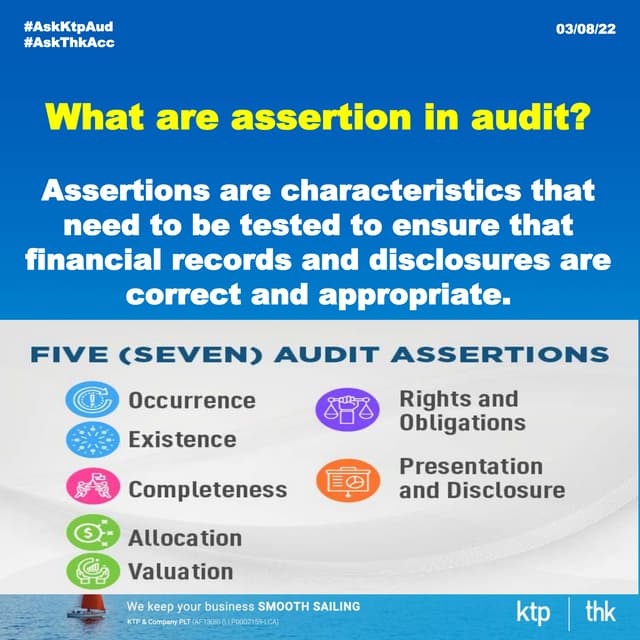

Auditors verify the accuracy of financial statements by testing assertions. There are three types of assertions - transaction level, account balance, and presentation/disclosure. Transaction level assertions ensure accuracy and validity of individual transactions. Account balance assertions check accuracy of assets, liabilities and equity on the balance sheet. Presentation/disclosure assertions ensure financial information is accurately classified, disclosed and understandable in the statements. By testing that transactions and account balances meet the relevant assertions, auditors can determine if the financial statements are fairly presented.