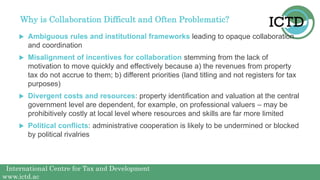

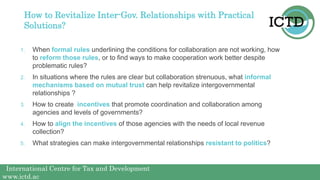

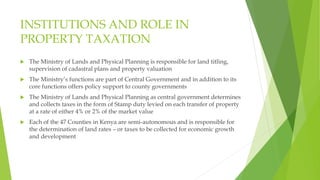

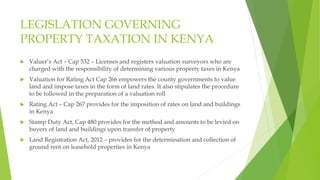

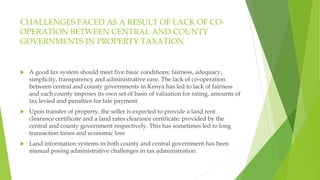

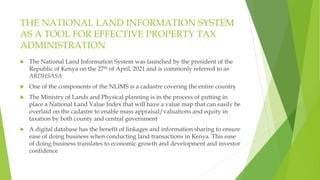

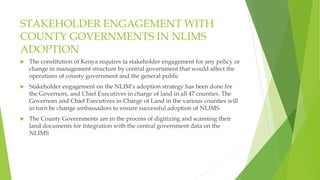

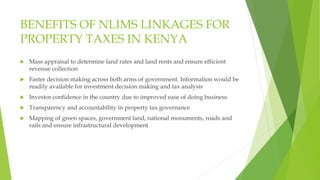

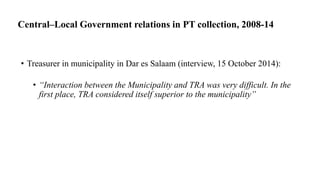

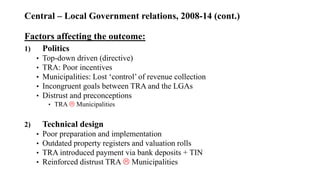

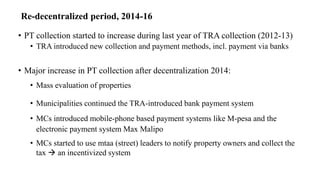

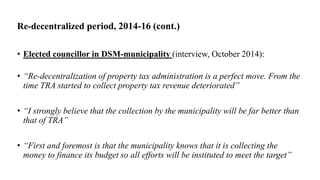

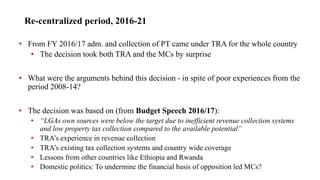

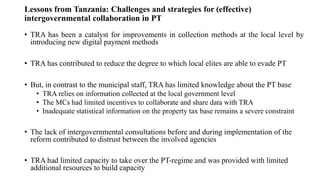

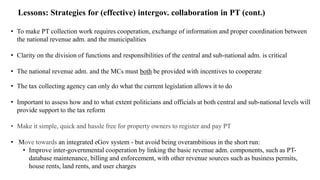

Download to read offline

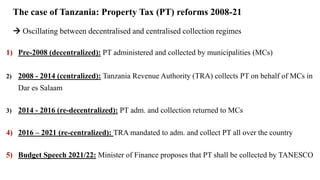

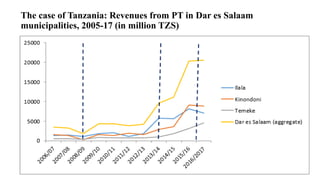

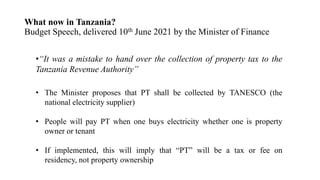

![Budget Speech, delivered 8th June 2017 by the Minister of Finance

To make the re-centralized PT regime work, the Minister emphasizes the

importance of intergovernmental collaboration:

•“[I] urge all stakeholders, including property owners, council

officials, district commissioners and TRA officials to work hand in

hand in fulfilling this important task for development of our

communities and the nation at large"](https://image.slidesharecdn.com/aptiatafwebinar3-slidesjune302021-211007153727/85/Apti-ataf-webinar-3-slides-june-30-2021-27-320.jpg)

O webinar apresentou a importância da colaboração intergovernamental para a administração eficaz do imposto sobre propriedade, discutindo as dinâmicas entre governos centrais e locais em diferentes países africanos. Foi destacado que a responsabilidade pela avaliação e cobrança de impostos varia amplamente, e que a falta de cooperação resulta em ineficiências e desafios administrativos. Através de estudos de caso em países como Quênia, Tanzânia e Gana, foram abordadas as dificuldades e estratégias para fortalecer essa colaboração, visando melhorar a arrecadação e a transparência tributária.