The document provides accounting entries for various transactions in Oracle apps R12, including:

1. Payables entries for receiving goods, invoice creation, payments, debit/credit memos, and prepayments.

2. Receivables entries for order to cash transactions, deposits, guarantees, revenue recognition, and refunds.

3. Asset entries for additions, changes, transfers, revaluations, retirements, and depreciation.

The published document gives overall view of OTC, is the end-to-end business process for receiving and processing customer orders. It also gives accounting and technical insight for Oracle application R12 OTC cycle.

Accounting is very easy to understand. This tutorial is design for them who does not know about accounting or has limited accounting knowledge. We have described it with hands on example. After viewing this students or business man can understand how reports look like and what important information can bring by structural accounting system. At the end we have shown, how to generate reports using accounting software.

Case 15-8 Controlling Revenue Page 1 Case 15-.docxannandleola

Case 15-8: Controlling Revenue Page 1

Case 15-8 Controlling Revenue

Handout 1 - Process Flow Diagrams

Order Processing

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8: Controlling Revenue Page 2

Shipping and Invoicing

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8 Controlling RevenueHandout 1 - Process Flow Diagrams

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8

Controlling Revenue

An engagement team is planning the audit of Always Better Care Company (ABC or the

“Company”), an SEC registrant that develops, manufactures, and sells a range of

products related to personal health and well-being. The engagement team is performing

an integrated audit for the year ended December 31, 2017, in accordance with the

standards of the PCAOB. This is the first year the team will serve as auditors of the

Company.

Paragraph .28 of PCAOB Auditing Standard 2201, An Audit of Internal Control Over

Financial Reporting That Is Integrated With an Audit of Financial Statements (PCAOB

AS 2201), states that “the auditor should identify significant accounts and disclosures and

their relevant assertions.” Accordingly, the engagement team has identified revenue as a

significant account balance.

In addition, paragraph .34 of PCAOB AS 2201 states:

To further understand the likely sources of potential misstatements, and as a part of

selecting the controls to test, the auditor should achieve the following objectives-

• Understand the flow of transactions related to the relevant assertions, including

how these transactions are initiated, authorized, processed, and recorded;

• Verify that the auditor has identified the points within the company’s processes at

which a misstatement—including a misstatement due to fraud—could arise that,

individually or in combination with other misstatements, would be material;

• Identify the controls that management has implemented to address these potential

misstatements; and

• Identify the controls that management has implemented over the prevention or

timely detection of unauthorized acquisition, use, or disposition of the company’s

assets that could result in a material misstatement of the financial statements.

In summary, the objective of understanding likely sources of misstatement is three-fold:

1. Understand the process.

2. Determine that the risks of material misstatement identified are complete and

appropriate.

3. Identify and understand the controls that address the identified risks.

Obtaining a robust understanding of the flow of transactions for significant accounts and

disclosures is the foundation for (1) identifying the points at which a material

misstatement can occur and (2) identifying the controls that mitigate those potential

misstatements.

Case 15-8c: Controlling Revenue Page 2

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

T.

Key Trends Shaping the Future of Infrastructure.pdfCheryl Hung

Keynote at DIGIT West Expo, Glasgow on 29 May 2024.

Cheryl Hung, ochery.com

Sr Director, Infrastructure Ecosystem, Arm.

The key trends across hardware, cloud and open-source; exploring how these areas are likely to mature and develop over the short and long-term, and then considering how organisations can position themselves to adapt and thrive.

Slack (or Teams) Automation for Bonterra Impact Management (fka Social Soluti...Jeffrey Haguewood

Sidekick Solutions uses Bonterra Impact Management (fka Social Solutions Apricot) and automation solutions to integrate data for business workflows.

We believe integration and automation are essential to user experience and the promise of efficient work through technology. Automation is the critical ingredient to realizing that full vision. We develop integration products and services for Bonterra Case Management software to support the deployment of automations for a variety of use cases.

This video focuses on the notifications, alerts, and approval requests using Slack for Bonterra Impact Management. The solutions covered in this webinar can also be deployed for Microsoft Teams.

Interested in deploying notification automations for Bonterra Impact Management? Contact us at sales@sidekicksolutionsllc.com to discuss next steps.

More Related Content

Similar to Accounting_entires_for_Oracle_apps_R12.pdf

The published document gives overall view of OTC, is the end-to-end business process for receiving and processing customer orders. It also gives accounting and technical insight for Oracle application R12 OTC cycle.

Accounting is very easy to understand. This tutorial is design for them who does not know about accounting or has limited accounting knowledge. We have described it with hands on example. After viewing this students or business man can understand how reports look like and what important information can bring by structural accounting system. At the end we have shown, how to generate reports using accounting software.

Case 15-8 Controlling Revenue Page 1 Case 15-.docxannandleola

Case 15-8: Controlling Revenue Page 1

Case 15-8 Controlling Revenue

Handout 1 - Process Flow Diagrams

Order Processing

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8: Controlling Revenue Page 2

Shipping and Invoicing

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8 Controlling RevenueHandout 1 - Process Flow Diagrams

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

Case 15-8

Controlling Revenue

An engagement team is planning the audit of Always Better Care Company (ABC or the

“Company”), an SEC registrant that develops, manufactures, and sells a range of

products related to personal health and well-being. The engagement team is performing

an integrated audit for the year ended December 31, 2017, in accordance with the

standards of the PCAOB. This is the first year the team will serve as auditors of the

Company.

Paragraph .28 of PCAOB Auditing Standard 2201, An Audit of Internal Control Over

Financial Reporting That Is Integrated With an Audit of Financial Statements (PCAOB

AS 2201), states that “the auditor should identify significant accounts and disclosures and

their relevant assertions.” Accordingly, the engagement team has identified revenue as a

significant account balance.

In addition, paragraph .34 of PCAOB AS 2201 states:

To further understand the likely sources of potential misstatements, and as a part of

selecting the controls to test, the auditor should achieve the following objectives-

• Understand the flow of transactions related to the relevant assertions, including

how these transactions are initiated, authorized, processed, and recorded;

• Verify that the auditor has identified the points within the company’s processes at

which a misstatement—including a misstatement due to fraud—could arise that,

individually or in combination with other misstatements, would be material;

• Identify the controls that management has implemented to address these potential

misstatements; and

• Identify the controls that management has implemented over the prevention or

timely detection of unauthorized acquisition, use, or disposition of the company’s

assets that could result in a material misstatement of the financial statements.

In summary, the objective of understanding likely sources of misstatement is three-fold:

1. Understand the process.

2. Determine that the risks of material misstatement identified are complete and

appropriate.

3. Identify and understand the controls that address the identified risks.

Obtaining a robust understanding of the flow of transactions for significant accounts and

disclosures is the foundation for (1) identifying the points at which a material

misstatement can occur and (2) identifying the controls that mitigate those potential

misstatements.

Case 15-8c: Controlling Revenue Page 2

Copyright 2013 Deloitte Development LLC

All Rights Reserved.

T.

Key Trends Shaping the Future of Infrastructure.pdfCheryl Hung

Keynote at DIGIT West Expo, Glasgow on 29 May 2024.

Cheryl Hung, ochery.com

Sr Director, Infrastructure Ecosystem, Arm.

The key trends across hardware, cloud and open-source; exploring how these areas are likely to mature and develop over the short and long-term, and then considering how organisations can position themselves to adapt and thrive.

Slack (or Teams) Automation for Bonterra Impact Management (fka Social Soluti...Jeffrey Haguewood

Sidekick Solutions uses Bonterra Impact Management (fka Social Solutions Apricot) and automation solutions to integrate data for business workflows.

We believe integration and automation are essential to user experience and the promise of efficient work through technology. Automation is the critical ingredient to realizing that full vision. We develop integration products and services for Bonterra Case Management software to support the deployment of automations for a variety of use cases.

This video focuses on the notifications, alerts, and approval requests using Slack for Bonterra Impact Management. The solutions covered in this webinar can also be deployed for Microsoft Teams.

Interested in deploying notification automations for Bonterra Impact Management? Contact us at sales@sidekicksolutionsllc.com to discuss next steps.

DevOps and Testing slides at DASA ConnectKari Kakkonen

My and Rik Marselis slides at 30.5.2024 DASA Connect conference. We discuss about what is testing, then what is agile testing and finally what is Testing in DevOps. Finally we had lovely workshop with the participants trying to find out different ways to think about quality and testing in different parts of the DevOps infinity loop.

Smart TV Buyer Insights Survey 2024 by 91mobiles.pdf91mobiles

91mobiles recently conducted a Smart TV Buyer Insights Survey in which we asked over 3,000 respondents about the TV they own, aspects they look at on a new TV, and their TV buying preferences.

Neuro-symbolic is not enough, we need neuro-*semantic*Frank van Harmelen

Neuro-symbolic (NeSy) AI is on the rise. However, simply machine learning on just any symbolic structure is not sufficient to really harvest the gains of NeSy. These will only be gained when the symbolic structures have an actual semantics. I give an operational definition of semantics as “predictable inference”.

All of this illustrated with link prediction over knowledge graphs, but the argument is general.

Accelerate your Kubernetes clusters with Varnish CachingThijs Feryn

A presentation about the usage and availability of Varnish on Kubernetes. This talk explores the capabilities of Varnish caching and shows how to use the Varnish Helm chart to deploy it to Kubernetes.

This presentation was delivered at K8SUG Singapore. See https://feryn.eu/presentations/accelerate-your-kubernetes-clusters-with-varnish-caching-k8sug-singapore-28-2024 for more details.

Transcript: Selling digital books in 2024: Insights from industry leaders - T...BookNet Canada

The publishing industry has been selling digital audiobooks and ebooks for over a decade and has found its groove. What’s changed? What has stayed the same? Where do we go from here? Join a group of leading sales peers from across the industry for a conversation about the lessons learned since the popularization of digital books, best practices, digital book supply chain management, and more.

Link to video recording: https://bnctechforum.ca/sessions/selling-digital-books-in-2024-insights-from-industry-leaders/

Presented by BookNet Canada on May 28, 2024, with support from the Department of Canadian Heritage.

Builder.ai Founder Sachin Dev Duggal's Strategic Approach to Create an Innova...Ramesh Iyer

In today's fast-changing business world, Companies that adapt and embrace new ideas often need help to keep up with the competition. However, fostering a culture of innovation takes much work. It takes vision, leadership and willingness to take risks in the right proportion. Sachin Dev Duggal, co-founder of Builder.ai, has perfected the art of this balance, creating a company culture where creativity and growth are nurtured at each stage.

The Art of the Pitch: WordPress Relationships and SalesLaura Byrne

Clients don’t know what they don’t know. What web solutions are right for them? How does WordPress come into the picture? How do you make sure you understand scope and timeline? What do you do if sometime changes?

All these questions and more will be explored as we talk about matching clients’ needs with what your agency offers without pulling teeth or pulling your hair out. Practical tips, and strategies for successful relationship building that leads to closing the deal.

UiPath Test Automation using UiPath Test Suite series, part 4DianaGray10

Welcome to UiPath Test Automation using UiPath Test Suite series part 4. In this session, we will cover Test Manager overview along with SAP heatmap.

The UiPath Test Manager overview with SAP heatmap webinar offers a concise yet comprehensive exploration of the role of a Test Manager within SAP environments, coupled with the utilization of heatmaps for effective testing strategies.

Participants will gain insights into the responsibilities, challenges, and best practices associated with test management in SAP projects. Additionally, the webinar delves into the significance of heatmaps as a visual aid for identifying testing priorities, areas of risk, and resource allocation within SAP landscapes. Through this session, attendees can expect to enhance their understanding of test management principles while learning practical approaches to optimize testing processes in SAP environments using heatmap visualization techniques

What will you get from this session?

1. Insights into SAP testing best practices

2. Heatmap utilization for testing

3. Optimization of testing processes

4. Demo

Topics covered:

Execution from the test manager

Orchestrator execution result

Defect reporting

SAP heatmap example with demo

Speaker:

Deepak Rai, Automation Practice Lead, Boundaryless Group and UiPath MVP

State of ICS and IoT Cyber Threat Landscape Report 2024 previewPrayukth K V

The IoT and OT threat landscape report has been prepared by the Threat Research Team at Sectrio using data from Sectrio, cyber threat intelligence farming facilities spread across over 85 cities around the world. In addition, Sectrio also runs AI-based advanced threat and payload engagement facilities that serve as sinks to attract and engage sophisticated threat actors, and newer malware including new variants and latent threats that are at an earlier stage of development.

The latest edition of the OT/ICS and IoT security Threat Landscape Report 2024 also covers:

State of global ICS asset and network exposure

Sectoral targets and attacks as well as the cost of ransom

Global APT activity, AI usage, actor and tactic profiles, and implications

Rise in volumes of AI-powered cyberattacks

Major cyber events in 2024

Malware and malicious payload trends

Cyberattack types and targets

Vulnerability exploit attempts on CVEs

Attacks on counties – USA

Expansion of bot farms – how, where, and why

In-depth analysis of the cyber threat landscape across North America, South America, Europe, APAC, and the Middle East

Why are attacks on smart factories rising?

Cyber risk predictions

Axis of attacks – Europe

Systemic attacks in the Middle East

Download the full report from here:

https://sectrio.com/resources/ot-threat-landscape-reports/sectrio-releases-ot-ics-and-iot-security-threat-landscape-report-2024/

State of ICS and IoT Cyber Threat Landscape Report 2024 preview

Accounting_entires_for_Oracle_apps_R12.pdf

1. 7th July 2010

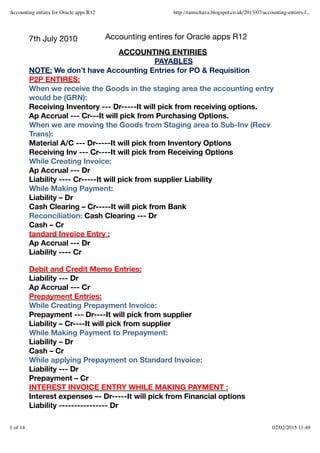

ACCOUNTING ENTIRIES

PAYABLES

NOTE: We don’t have Accounting Entries for PO & Requisition

P2P ENTIRES:

When we receive the Goods in the staging area the accounting entry

would be (GRN):

Receiving Inventory --- Dr-----It will pick from receiving options.

Ap Accrual --- Cr---It will pick from Purchasing Options.

When we are moving the Goods from Staging area to Sub-Inv (Recv

Trans):

Material A/C --- Dr-----It will pick from Inventory Options

Receiving Inv --- Cr----It will pick from Receiving Options

While Creating Invoice:

Ap Accrual --- Dr

Liability ---- Cr-----It will pick from supplier Liability

While Making Payment:

Liability – Dr

Cash Clearing – Cr-----It will pick from Bank

Reconciliation: Cash Clearing --- Dr

Cash – Cr

tandard Invoice Entry :

Ap Accrual --- Dr

Liability ---- Cr

Debit and Credit Memo Entries:

Liability --- Dr

Ap Accrual --- Cr

Prepayment Entries:

While Creating Prepayment Invoice:

Prepayment --- Dr----It will pick from supplier

Liability – Cr----It will pick from supplier

While Making Payment to Prepayment:

Liability – Dr

Cash – Cr

While applying Prepayment on Standard Invoice:

Liability --- Dr

Prepayment – Cr

INTEREST INVOICE ENTRY WHILE MAKING PAYMENT :

Interest expenses –- Dr-----It will pick from Financial options

Liability ---------------- Dr

Accounting entires for Oracle apps R12

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

1 of 14 02/02/2015 11:49

2. Cash ---------------------Cr

EXPENSE REPORT ENTRY :

Item Expense A/C --- Dr

Liability --- Cr

PAYMENT REQUEST INVOICE ENTRY :

Item Expense --- Dr

Liability – Cr

FUTURE DATED PAYMENT ENTRY :

When Bills Issued:

Item Expense – Dr

Bills Payable --- Cr

When Maturity Date Confirmed:

Bills Payable – Dr---It will pick from Supplier or Financial options

Liability – Cr

WITH HOLDING TAX ENTRY :

When Withholding tax applied on standard Invoice:

Item Expense --- Dr

Liability --- Cr

Withholding --- Cr-----It will pick from WHT codes

Auto Generated WHT Entry:

Item Expense – Dr

Liability --- Cr

RETAINAGE RELEASE ACCOUNTING ENTRY:

When Invoice matched with PO accounting entry would be:

Accrual ------ Dr

Liability ---- Cr

Retainage ---Cr----It will pick from financial options

While making payment to the invoice matched with PO:

Liability ---- Dr

Cash --------Cr

When Retainage Release Invoice Matched with PO accounting entry

would be:

Retainage --------Dr

Liability ----------- Cr

While making Payment to Retainage Release:

Liability ---Dr

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

2 of 14 02/02/2015 11:49

3. Cash -------Cr

RECEIVABLES

O2C ENTRIES:

Pick Release:

Receiving Inventory ---- Dr

Item Expense/Material ac ---- Cr

Ship Confirmation:

COGS ---- Dr----It will pick from Inv Information

Receiving Inv (Sub-Inv) ---- Cr

While Creating Transaction:

Receivable ---- Dr

Revenue ------- Cr

Freight --------Cr

Tax -------------Cr

While Recording Receipt: WHEN STATE IS CONFIRMED

Confirmed Cash--------------Dr

Receivables ----Cr

When Remitted: WHEN STATE IS REMITTED

Remitted Cash ---- Dr

Confirmed Cash--------Cr

When Reconciled: WHEN STATE IS CLEARED

Cash -------Dr

Remitted Cash --- Cr

DEPOSIT ACCOUNTING ENTRY:

When we create DEPOSIT invoice the accounting entry would be:

Receivable --- Dr

Accrual (Unearned Revenue) -------- Cr

When we create Sales Invoice:

Receivable---Dr

Revenue----- Cr

When Deposit adjusts with actual transaction invoice the entry would be:

Unearned Rev (Accrual) -----Dr

Receivables-------Cr

GAURANTEE ACCOUNTING ENTRY:

When we crate Guarantee transaction:

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

3 of 14 02/02/2015 11:49

4. Unbilled receivable----Dr

Unearned Revenue ---Cr

When we create sales Invoice:

Receivable ----Dr

Revenue -------Cr

When Guarantee transaction adjusts with sales invoice:

Unearned Revenue ---Dr

Unbilled Receivable—Cr

REVENUE RECOGNISATION:

INVOICE ADVANCE:

When we create sales invoice and set invoicing rule as

INADVANCE(FIXED SCH):

Receivables ---- Dr

Unearned Revenue -------- Cr

Once we recognize the Revenue the accounting entry would be:

Unearned Revenue ---- Dr

Revenue------------------Cr

And the final entry would be:

Receivable ------Dr

Revenue ---------Cr

INVOICE ARREARS:

REVENUE RECOGNISATION using Invoice Arrears Schedule:

Unbilled Receivables—Dr

Revenue-----------------Cr

Once we have billed the customer

Receivables---------------Dr

Unbilled Receivables--Cr

ONACCOUNT ACCOUNTING ENTRY:

When we created the Receipt and applied to OnAccount :

Cash ---Dr

Receivables ----CR, ONACCOUNT -----Cr

CUSTOMER REFUND ACCOUNTING ENTRY :

When we release the On account and Refund the Amount:

Cash ----Dr

Receivables----Cr

On Account Cash ---Cr

Unapplied Cash -----Dr

Refund----------------Cr

Assets:

Asset Addition :

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

4 of 14 02/02/2015 11:49

5. The process of adding a Fixed Asset either through detailed, quick or mass addition is

called asset addition. Detail and quick addition are carried out only in Oracle Assets.

The journal entry in Oracle Assets during detailed or quick addition is

Dr. Asset Cost

Cr. Asset clearing account

In Oracle Assets the journal entry remains the same

Dr. Asset Cost

Cr. Asset clearing account

Dr Asset Clearing Account

Cr Accounts Paya

Changes:

Changes refer to change in Asset Cost or Depreciation method or

Depreciation rate for one or more assets. Oracle Assets would use the new

cost or depreciation method or rate from the period of change to arrive at

the depreciation amount. Also it recalculates the depreciation that should

have been calculated so far, compares with the actual depreciation and

passes an adjusting entry.

If the transaction results in addition to the cost of asset, then the journal entry

created is

Dr. Asset Cost

Cr. Asset Clearing

Hence an adjusting entry to incorporate depreciation as per the new cost of the asset

should be incorporated. Also due to change in method or rate the new depreciation

calculated may be lower or greater than the depreciation calculated so far.

If the accumulated depreciation recalculated is lower than the accumulated

depreciation calculated until now,

Dr. Accumulated Depreciation

Cr. Depreciation Expense (Adjustment)

If it is greater than the Accumulated depreciation until now,

Dr. Depreciation Expense (Adjustment)

Asset clearing account is used to reconcile the transactions between Oracle

Payables and Oracle Assets. When an asset is added through detailed or quick

additions, the credit goes to the asset clearing account. Also for mass addition

process, oracle assets use Asset Clearing account for reconciliation.

In AP

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

5 of 14 02/02/2015 11:49

6. Cr. Accumulated Depreciation

Transfers refer to change in Location, expense account, and employee

assignment. If there is a change in expense account, for e.g. If an asset is

transferred from department 001 to department 002,

The journal entry for accounting the asset cost is

Dr. Asset Cost (002)

Cr. Asset Cost (001)

The journal entry for accounting the accumulated depreciation is

Dr. Accumulated Depreciation (001)

Cr. Accumulated Depreciation (002)

Revaluation is a process so as to reflect current market price of the Asset.

The journal entry created by revaluing a fixed asset is as follows:

Revalue Accumulated Depreciation is enabled at the Book Controls level:

The amount of revaluation would be credited to Accumulated Depreciation

and Revaluation reserve in the same proportion as the existing

Accumulates Depreciation and Net Book value.

Dr. Asset Cost

Cr. Accumulated Depreciation

Cr. Revaluation Reserve

Revalue Accumulated Depreciation is disabled at the Book Controls

level:

To the extend of the revaluation amount, the following journal entry would

be passed.

Dr. Asset Cost

Cr. Revaluation Reserve

Also the existing depreciation reserve would also be transferred to the

Revaluation Reserve

Transfers

Revaluation

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

6 of 14 02/02/2015 11:49

7. Dr. Accumulated Depreciation

Cr. Revaluation Reserve

Oracle Assets passes the following journal entry for retirement.

If the retirement transaction resulted in a Gain, the journal entry passed

would be.

Dr. Accumulated Depreciation

Dr. Proceeds of sale

Cr. Asset Cost

Cr. Gain / Loss

If the retirement transaction resulted in a Loss, the journal entry passed

would be.

Dr. Accumulated Depreciation

Dr. Proceeds of sale

Dr. Gain / Loss

Cr. Asset Cost

Depreciation:

Running depreciation (as applicable to a particular asset) during the period

end would pass a journal entry

Dr. Depreciation Expense

Cr. Accumulated Depreciation

ACCOUNTING ENTIRIES

PAYABLES

NOTE: We don’t have Accounting Entries for PO & Requisition

P2P ENTIRES:

When we receive the Goods in the staging area the accounting entry

would be (GRN):

Receiving Inventory --- Dr-----It will pick from receiving options.

Ap Accrual --- Cr---It will pick from Purchasing Options.

When we are moving the Goods from Staging area to Sub-Inv (Recv

Trans):

Material A/C --- Dr-----It will pick from Inventory Options

Receiving Inv --- Cr----It will pick from Receiving Options

While Creating Invoice:

Ap Accrual --- Dr

Retirements

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

7 of 14 02/02/2015 11:49

8. Liability ---- Cr-----It will pick from supplier Liability

While Making Payment:

Liability – Dr

Cash Clearing – Cr-----It will pick from Bank

Reconciliation: Cash Clearing --- Dr

Cash – Cr

tandard Invoice Entry :

Ap Accrual --- Dr

Liability ---- Cr

Debit and Credit Memo Entries:

Liability --- Dr

Ap Accrual --- Cr

Prepayment Entries:

While Creating Prepayment Invoice:

Prepayment --- Dr----It will pick from supplier

Liability – Cr----It will pick from supplier

While Making Payment to Prepayment:

Liability – Dr

Cash – Cr

While applying Prepayment on Standard Invoice:

Liability --- Dr

Prepayment – Cr

INTEREST INVOICE ENTRY WHILE MAKING PAYMENT :

Interest expenses –- Dr-----It will pick from Financial options

Liability ---------------- Dr

Cash ---------------------Cr

EXPENSE REPORT ENTRY :

Item Expense A/C --- Dr

Liability --- Cr

PAYMENT REQUEST INVOICE ENTRY :

Item Expense --- Dr

Liability – Cr

FUTURE DATED PAYMENT ENTRY :

When Bills Issued:

Item Expense – Dr

Bills Payable --- Cr

When Maturity Date Confirmed:

Bills Payable – Dr---It will pick from Supplier or Financial options

Liability – Cr

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

8 of 14 02/02/2015 11:49

9. WITH HOLDING TAX ENTRY :

When Withholding tax applied on standard Invoice:

Item Expense --- Dr

Liability --- Cr

Withholding --- Cr-----It will pick from WHT codes

Auto Generated WHT Entry:

Item Expense – Dr

Liability --- Cr

RETAINAGE RELEASE ACCOUNTING ENTRY:

When Invoice matched with PO accounting entry would be:

Accrual ------ Dr

Liability ---- Cr

Retainage ---Cr----It will pick from financial options

While making payment to the invoice matched with PO:

Liability ---- Dr

Cash --------Cr

When Retainage Release Invoice Matched with PO accounting entry

would be:

Retainage --------Dr

Liability ----------- Cr

While making Payment to Retainage Release:

Liability ---Dr

Cash -------Cr

RECEIVABLES

While Creating Transaction:

Receivable ---- Dr

Revenue ------- Cr

Freight --------Cr

Tax -------------Cr

While Recording Receipt: WHEN STATE IS CONFIRMED

Confirmed Cash--------------Dr

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

9 of 14 02/02/2015 11:49

10. Receivables ----Cr

When Remitted: WHEN STATE IS REMITTED

Remitted Cash ---- Dr

Confirmed Cash--------Cr

When Reconciled: WHEN STATE IS CLEARED

Cash -------Dr

Remitted Cash --- Cr

DEPOSIT ACCOUNTING ENTRY:

When we create DEPOSIT invoice the accounting entry would be:

Receivable --- Dr

Accrual (Unearned Revenue) -------- Cr

When we create Sales Invoice:

Receivable---Dr

Revenue----- Cr

When Deposit adjusts with actual transaction invoice the entry would be:

Unearned Rev (Accrual) -----Dr

Receivables-------Cr

GAURANTEE ACCOUNTING ENTRY:

When we crate Guarantee transaction:

Unbilled receivable----Dr

Unearned Revenue ---Cr

When we create sales Invoice:

Receivable ----Dr

Revenue -------Cr

When Guarantee transaction adjusts with sales invoice:

Unearned Revenue ---Dr

Unbilled Receivable—Cr

REVENUE RECOGNISATION:

INVOICE ADVANCE:

When we create sales invoice and set invoicing rule as

INADVANCE(FIXED SCH):

Receivables ---- Dr

Unearned Revenue -------- Cr

Once we recognize the Revenue the accounting entry would be:

Unearned Revenue ---- Dr

Revenue------------------Cr

And the final entry would be:

Receivable ------Dr

Revenue ---------Cr

INVOICE ARREARS:

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

10 of 14 02/02/2015 11:49

11. REVENUE RECOGNISATION using Invoice Arrears Schedule:

Unbilled Receivables—Dr

Revenue-----------------Cr

Once we have billed the customer

Receivables---------------Dr

Unbilled Receivables--Cr

ONACCOUNT ACCOUNTING ENTRY:

When we created the Receipt and applied to OnAccount :

Cash ---Dr

Receivables ----CR, ONACCOUNT -----Cr

CUSTOMER REFUND ACCOUNTING ENTRY :

When we release the On account and Refund the Amount:

Cash ----Dr

Receivables----Cr

On Account Cash ---Cr

Unapplied Cash -----Dr

Refund----------------Cr

Assets:

Asset Addition :

The process of adding a Fixed Asset either through detailed, quick or mass addition is

called asset addition. Detail and quick addition are carried out only in Oracle Assets.

The journal entry in Oracle Assets during detailed or quick addition is

Dr. Asset Cost

Cr. Asset clearing account

In Oracle Assets the journal entry remains the same

Dr. Asset Cost

Cr. Asset clearing account

Dr Asset Clearing Account

Cr Accounts Paya

Changes:

Changes refer to change in Asset Cost or Depreciation method or

Depreciation rate for one or more assets. Oracle Assets would use the new

Asset clearing account is used to reconcile the transactions between Oracle

Payables and Oracle Assets. When an asset is added through detailed or quick

additions, the credit goes to the asset clearing account. Also for mass addition

process, oracle assets use Asset Clearing account for reconciliation.

In AP

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

11 of 14 02/02/2015 11:49

12. cost or depreciation method or rate from the period of change to arrive at

the depreciation amount. Also it recalculates the depreciation that should

have been calculated so far, compares with the actual depreciation and

passes an adjusting entry.

If the transaction results in addition to the cost of asset, then the journal entry

created is

Dr. Asset Cost

Cr. Asset Clearing

Hence an adjusting entry to incorporate depreciation as per the new cost of the asset

should be incorporated. Also due to change in method or rate the new depreciation

calculated may be lower or greater than the depreciation calculated so far.

If the accumulated depreciation recalculated is lower than the accumulated

depreciation calculated until now,

Dr. Accumulated Depreciation

Cr. Depreciation Expense (Adjustment)

If it is greater than the Accumulated depreciation until now,

Dr. Depreciation Expense (Adjustment)

Cr. Accumulated Depreciation

Transfers refer to change in Location, expense account, and employee

assignment. If there is a change in expense account, for e.g. If an asset is

transferred from department 001 to department 002,

The journal entry for accounting the asset cost is

Dr. Asset Cost (002)

Cr. Asset Cost (001)

The journal entry for accounting the accumulated depreciation is

Dr. Accumulated Depreciation (001)

Cr. Accumulated Depreciation (002)

Transfers

Revaluation

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

12 of 14 02/02/2015 11:49

13. Revaluation is a process so as to reflect current market price of the Asset.

The journal entry created by revaluing a fixed asset is as follows:

Revalue Accumulated Depreciation is enabled at the Book Controls level:

The amount of revaluation would be credited to Accumulated Depreciation

and Revaluation reserve in the same proportion as the existing

Accumulates Depreciation and Net Book value.

Dr. Asset Cost

Cr. Accumulated Depreciation

Cr. Revaluation Reserve

Revalue Accumulated Depreciation is disabled at the Book Controls

level:

To the extend of the revaluation amount, the following journal entry would

be passed.

Dr. Asset Cost

Cr. Revaluation Reserve

Also the existing depreciation reserve would also be transferred to the

Revaluation Reserve

Dr. Accumulated Depreciation

Cr. Revaluation Reserve

Oracle Assets passes the following journal entry for retirement.

If the retirement transaction resulted in a Gain, the journal entry passed

would be.

Dr. Accumulated Depreciation

Dr. Proceeds of sale

Cr. Asset Cost

Cr. Gain / Loss

If the retirement transaction resulted in a Loss, the journal entry passed

would be.

Dr. Accumulated Depreciation

Dr. Proceeds of sale

Dr. Gain / Loss

Cr. Asset Cost

Depreciation:

Retirements

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

13 of 14 02/02/2015 11:49

14. Running depreciation (as applicable to a particular asset) during the period

end would pass a journal entry

Dr. Depreciation Expense

Cr. Accumulated Depreciation

Posted 7th July 2010 by ramschava

Comment as: Select profile...

Publish

Publish Preview

Preview

0 Add a comment

Accounting entires for Oracle apps R12 http://ramschava.blogspot.co.uk/2013/07/accounting-entires-f...

14 of 14 02/02/2015 11:49