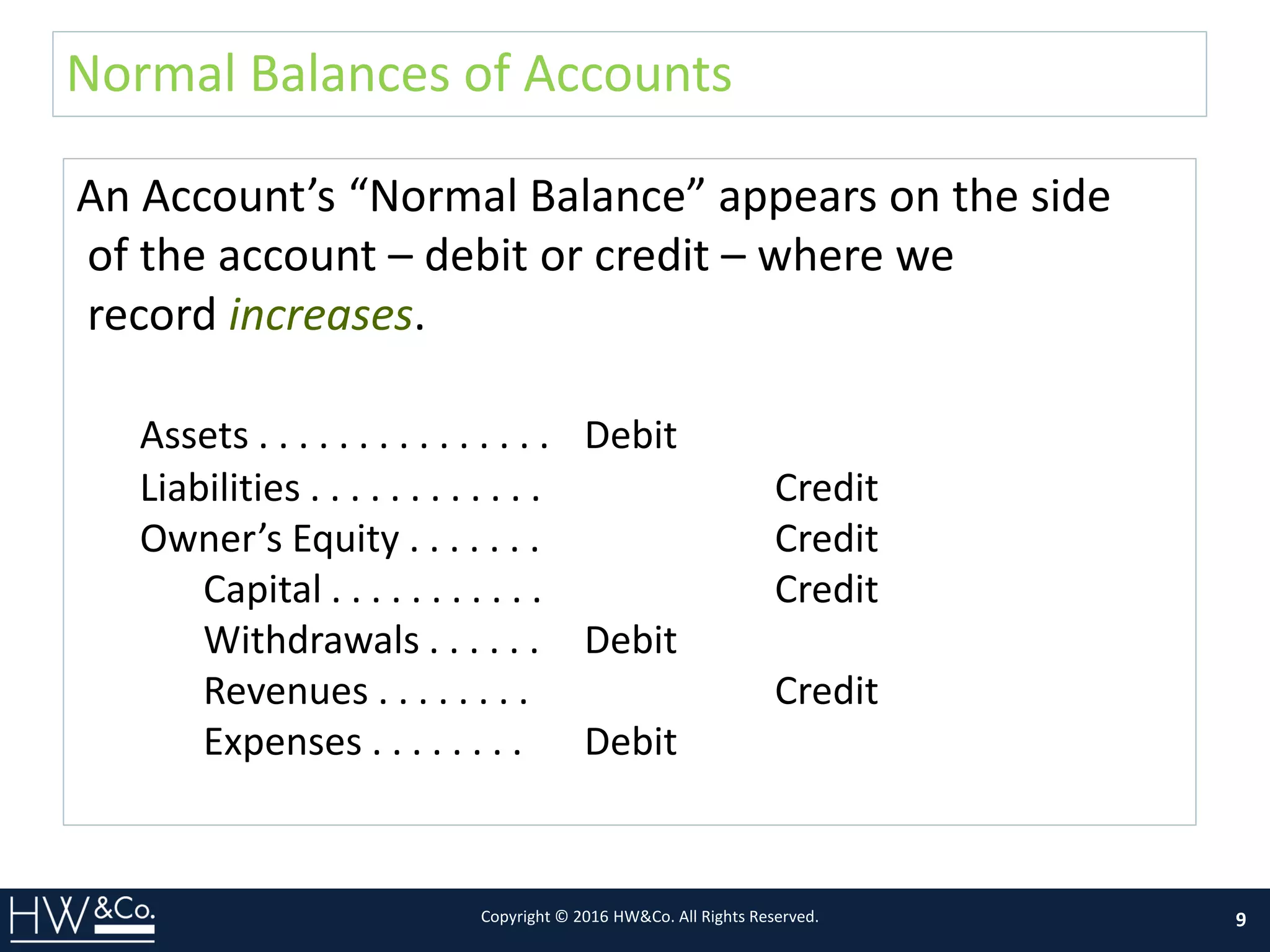

The document provides an overview of basic accounting concepts and principles for non-profit organizations. It discusses key accounting equations, account categories for assets, liabilities, and owner's equity. Examples of journal entries are provided for revenue, expenses, adjustments, and the accounting close process. Financial statements including the income statement and balance sheet are also briefly explained. The presentation aims to familiarize audiences with fundamental accounting concepts.