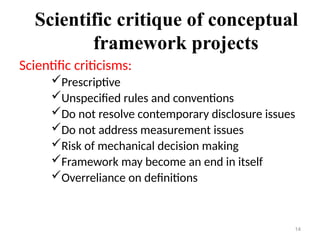

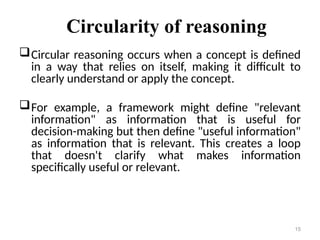

The document outlines a conceptual framework in accounting, which provides principles and guidelines for financial reporting, ensuring information is relevant, reliable, and comparable for stakeholders. It distinguishes between principles-based and rule-based standards, emphasizing the importance of the decision-theory approach in aiding informed decisions. Additionally, it addresses essential qualities of financial information and critiques the conceptual framework for its potential issues, such as circular reasoning and mechanical decision-making.