Downloaded 20 times

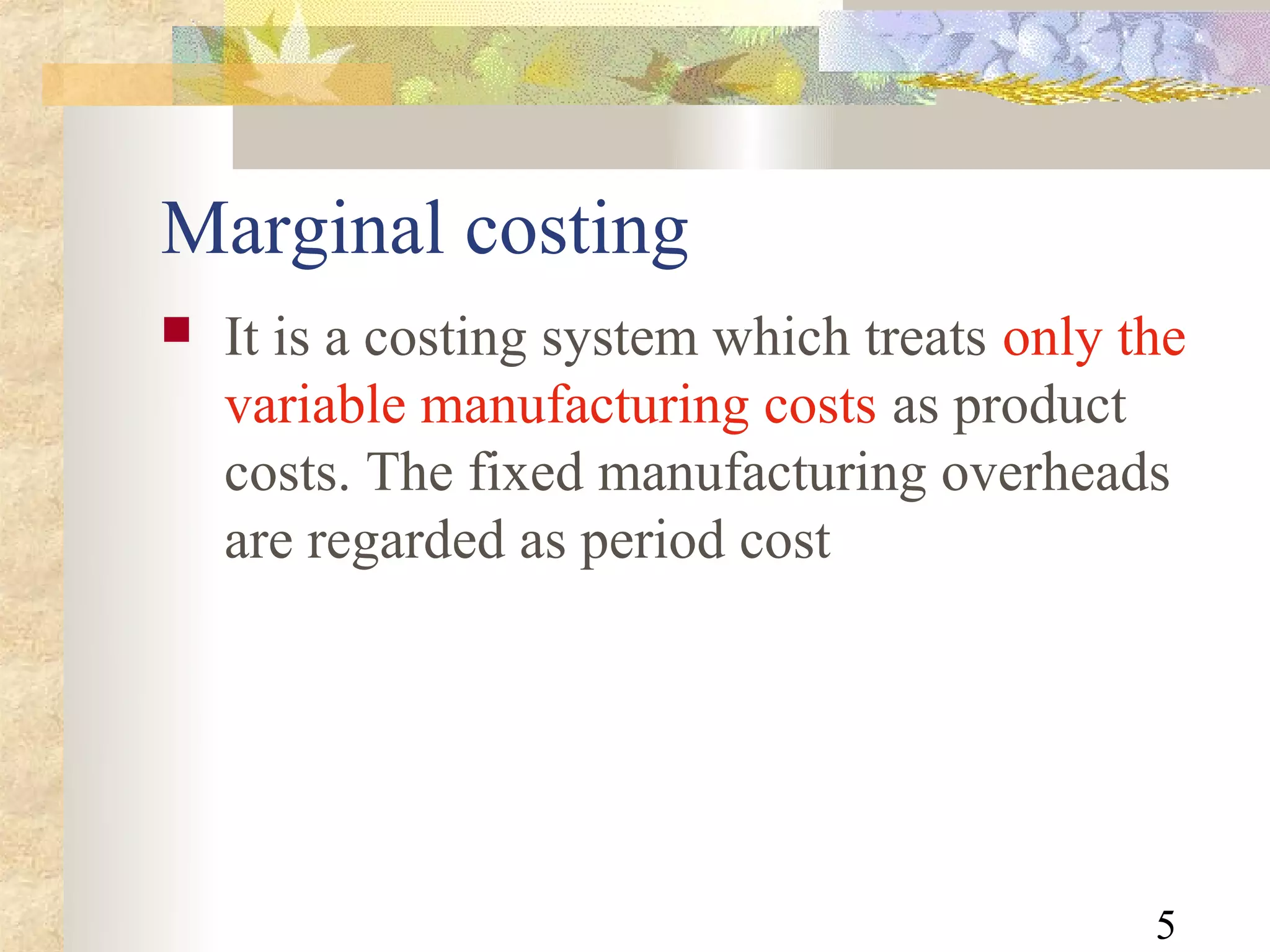

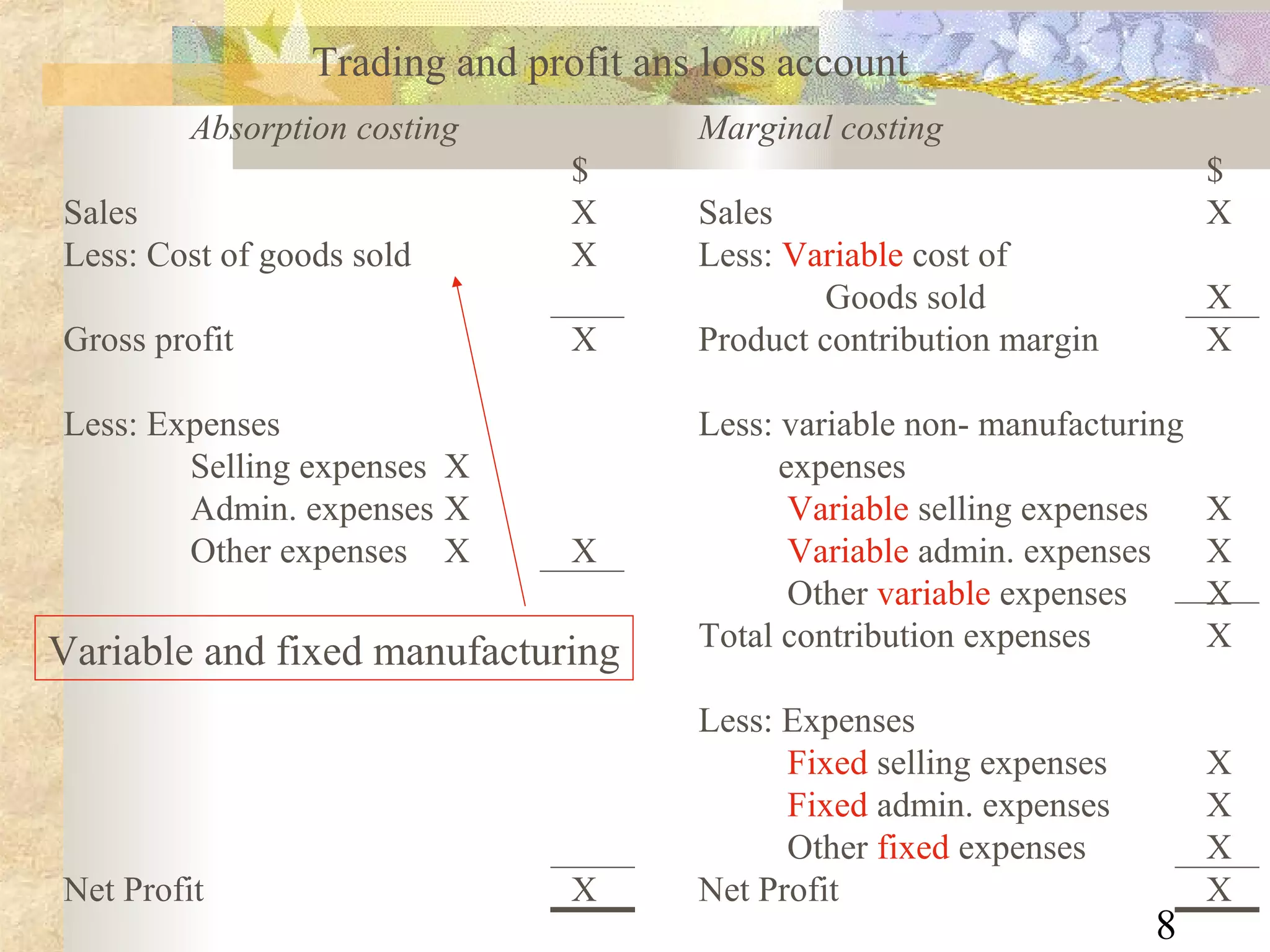

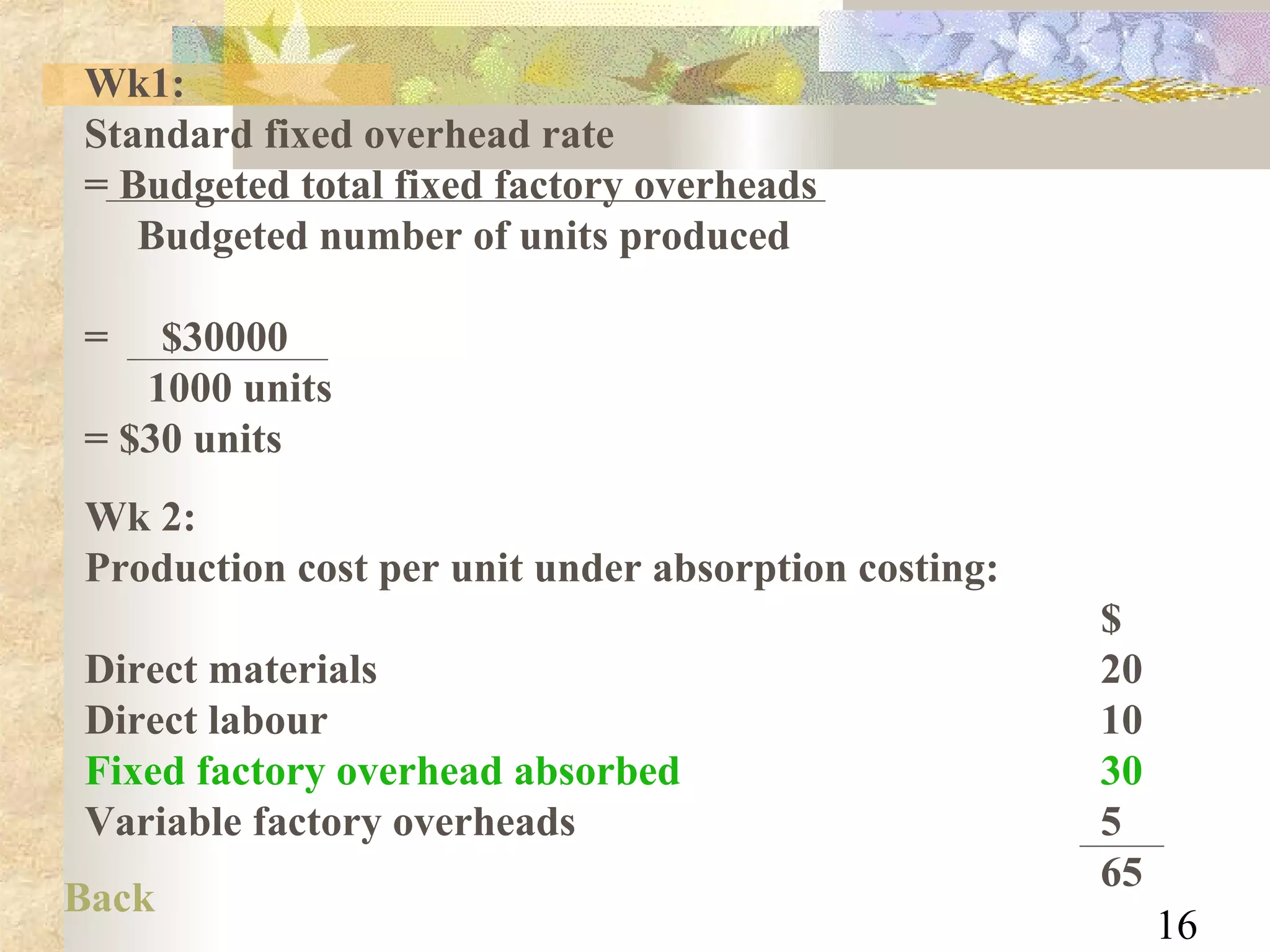

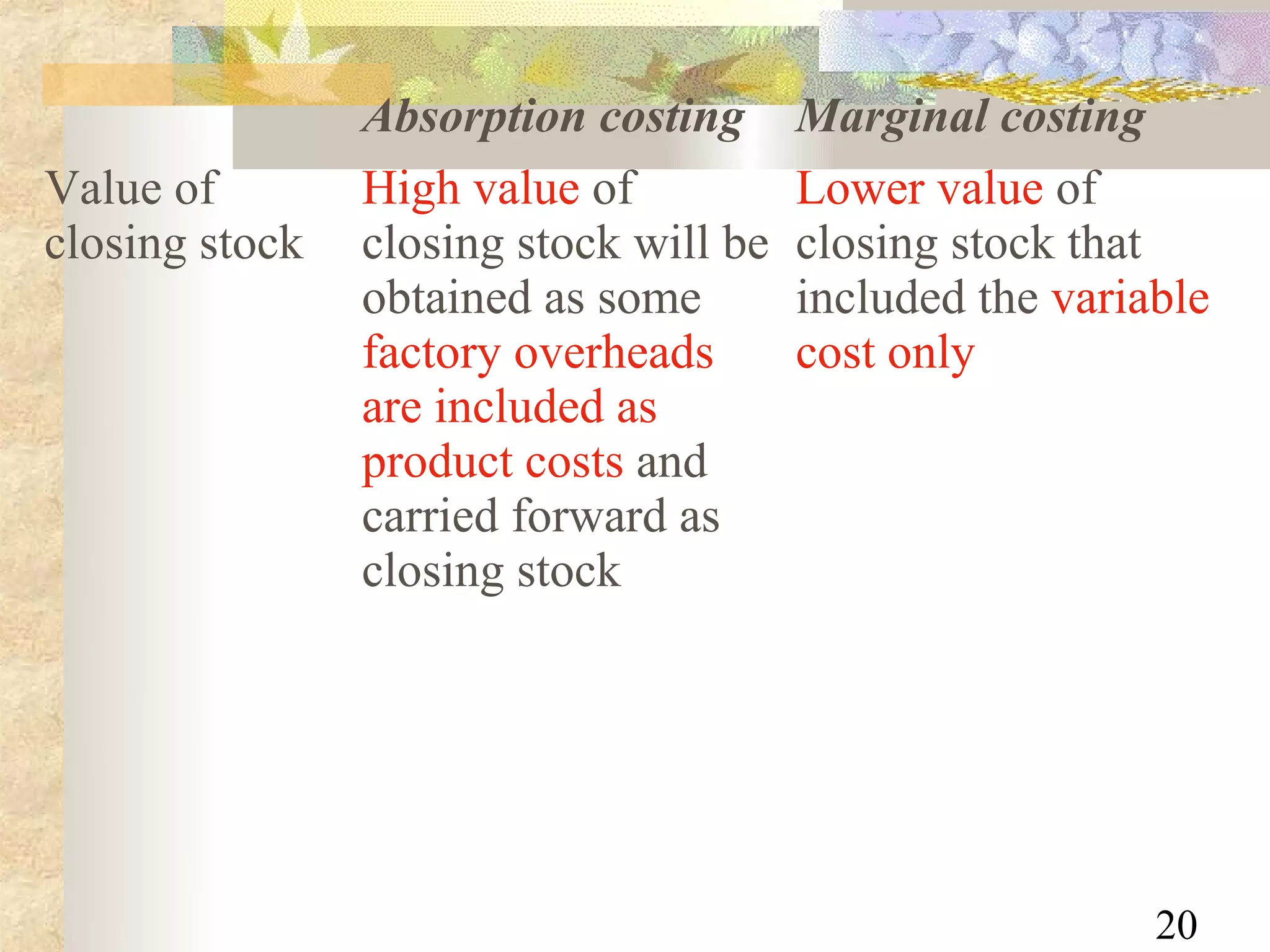

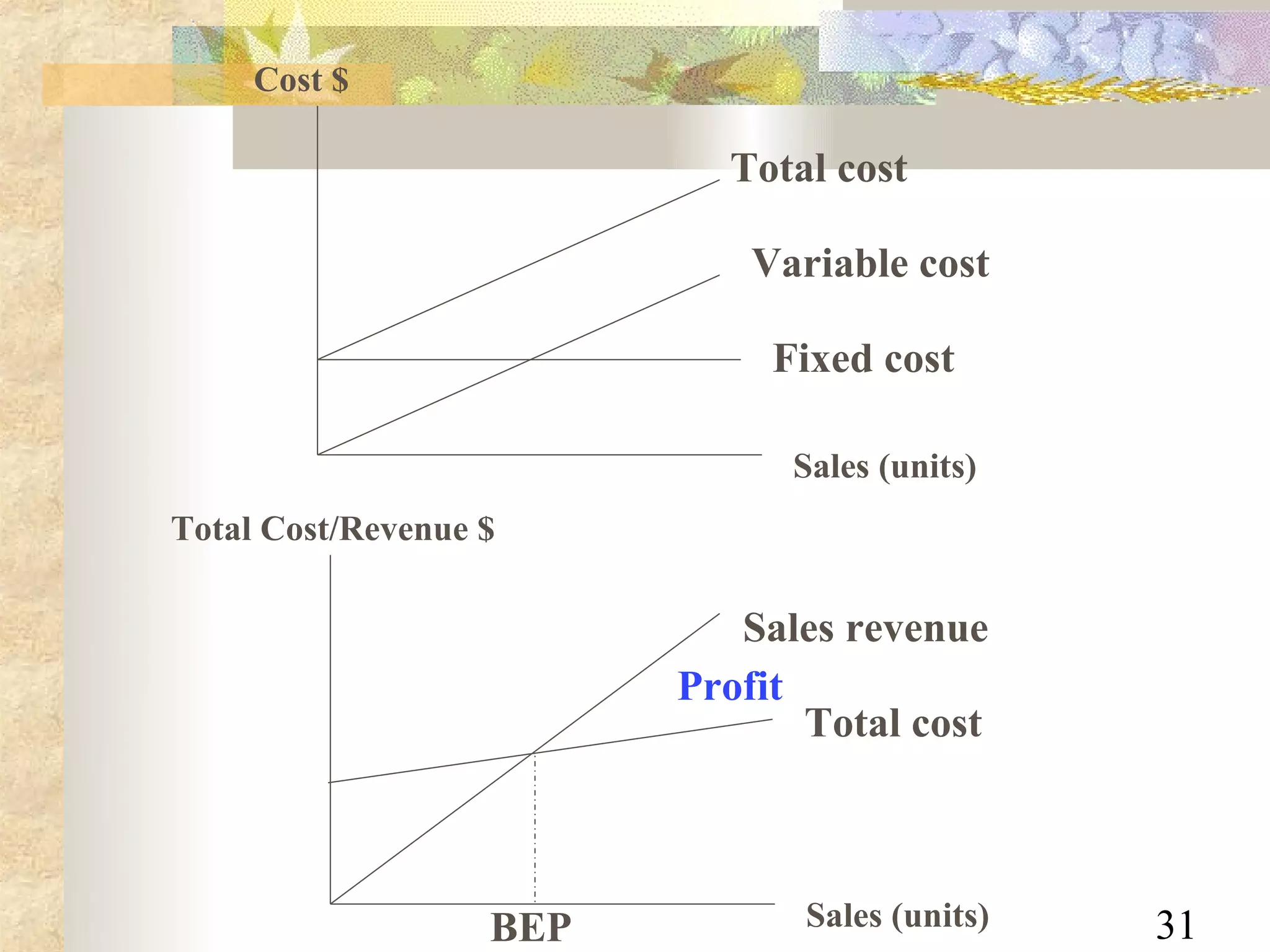

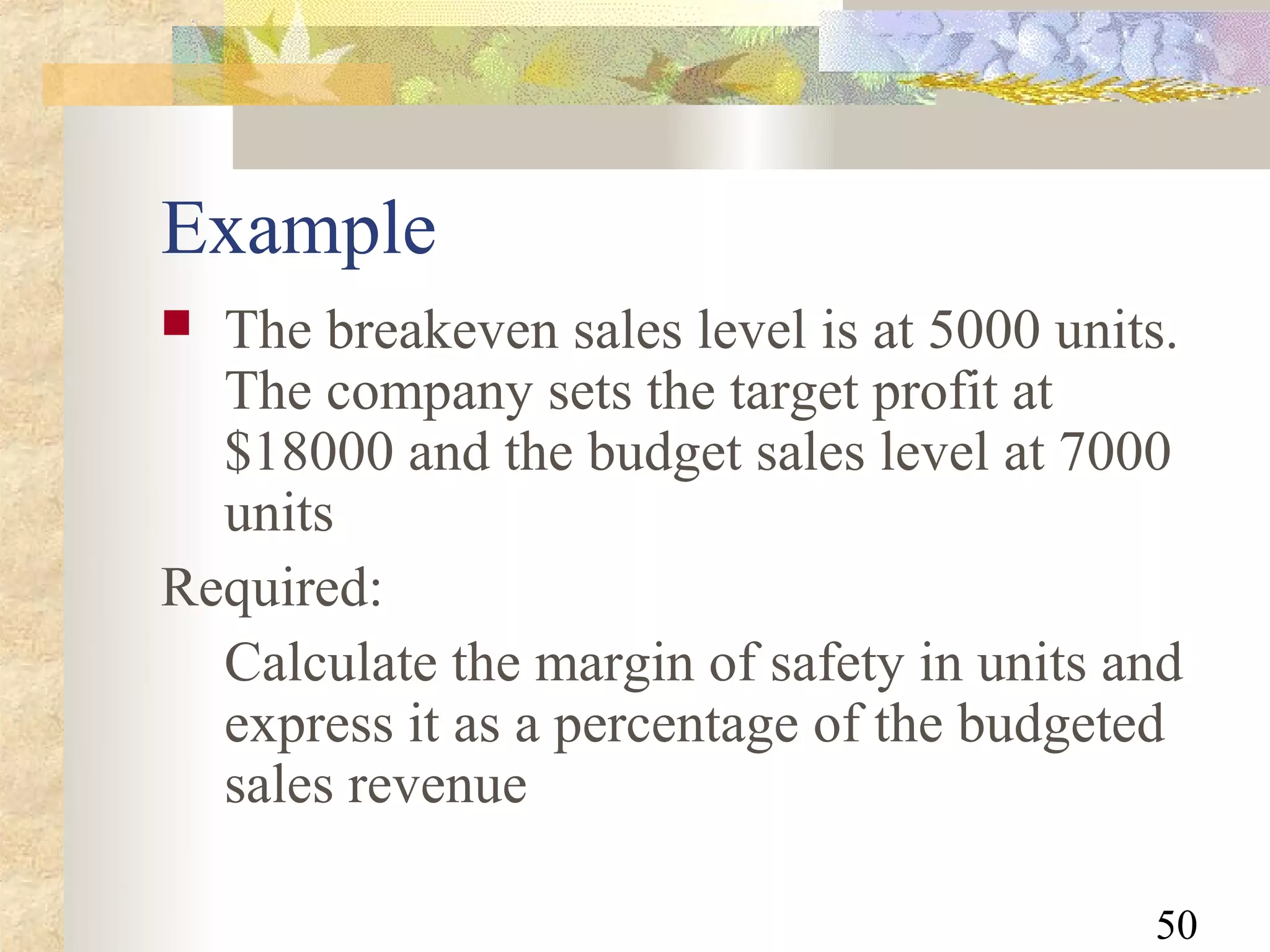

The document discusses absorption costing and marginal costing. Absorption costing treats all manufacturing costs, including fixed costs, as product costs. Marginal costing treats only variable manufacturing costs as product costs and regards fixed costs as period costs. Absorption costing results in a higher value of closing stock and reported profit compared to marginal costing. Breakeven analysis is also covered, including calculating the breakeven point, target profit, margin of safety, and the impact of changes in cost and revenue components. Limitations of breakeven analysis are that it assumes linear behavior and 100% sales of production.

![Manufacturing-account[1]](https://cdn.slidesharecdn.com/ss_thumbnails/manufacturing-account1-130307085801-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)