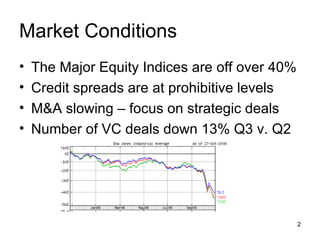

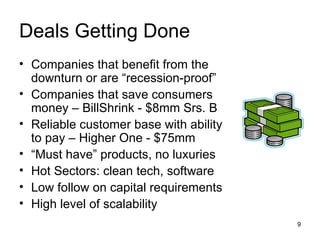

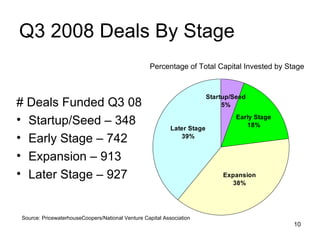

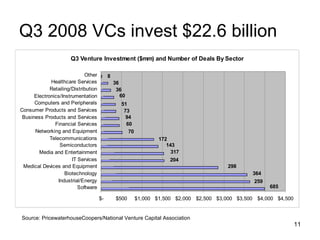

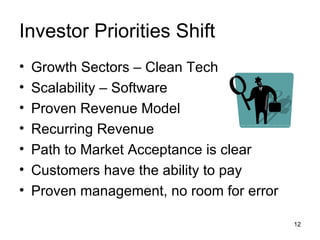

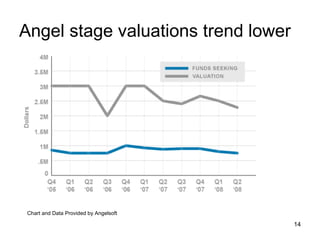

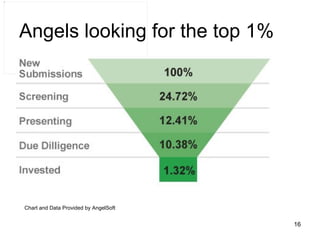

The document discusses the challenges facing young entrepreneurs amid a significant downturn in equity markets and venture capital funding, emphasizing the need for cost conservation and sustainable cash flow strategies. It highlights shifts in investor priorities towards recession-proof sectors and emphasizes the importance of creating a strong capital strategy and effective investor networks. Key advice includes understanding market conditions, establishing a reliable board of advisors, and preparing thoroughly for funding presentations.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)