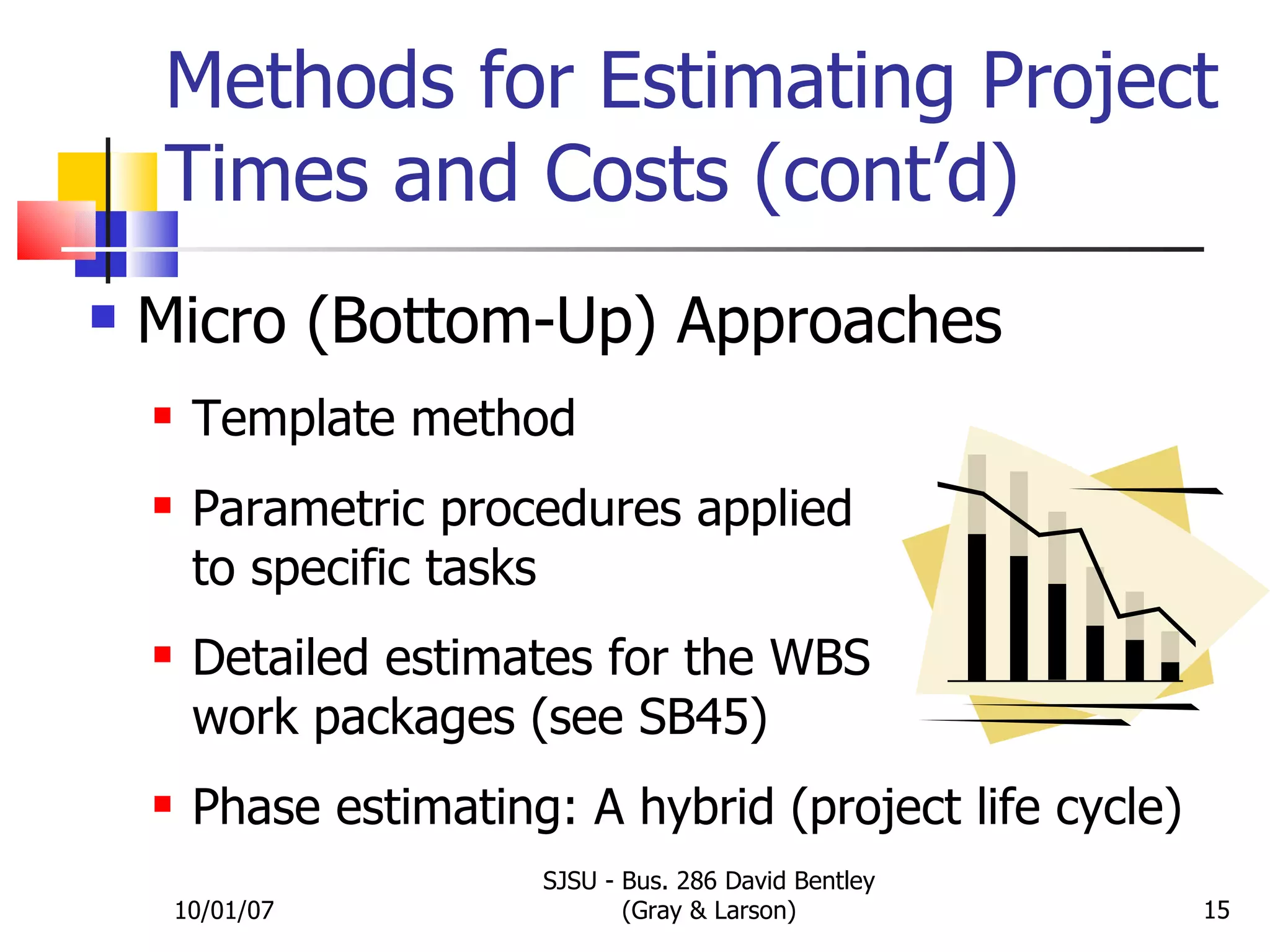

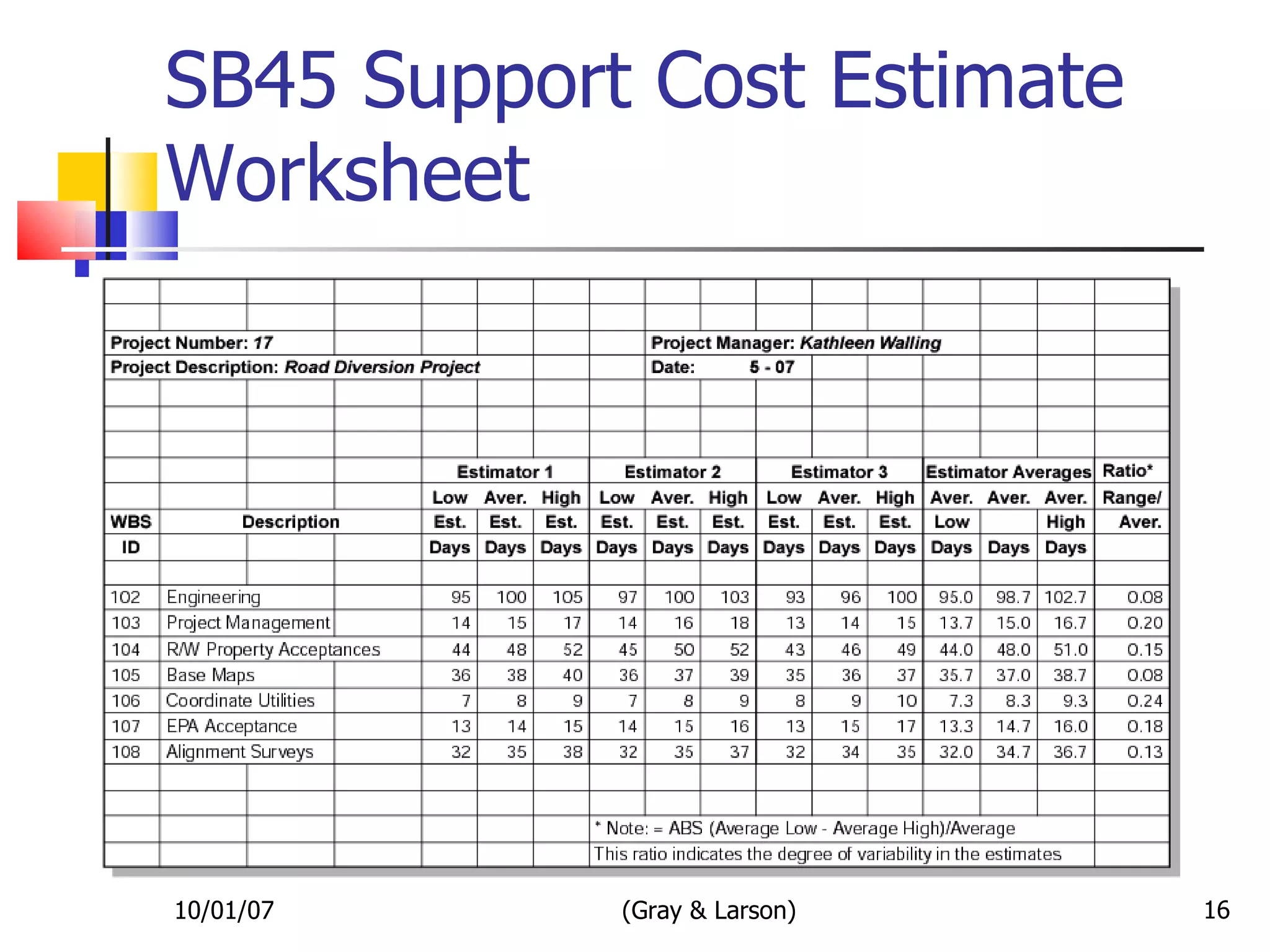

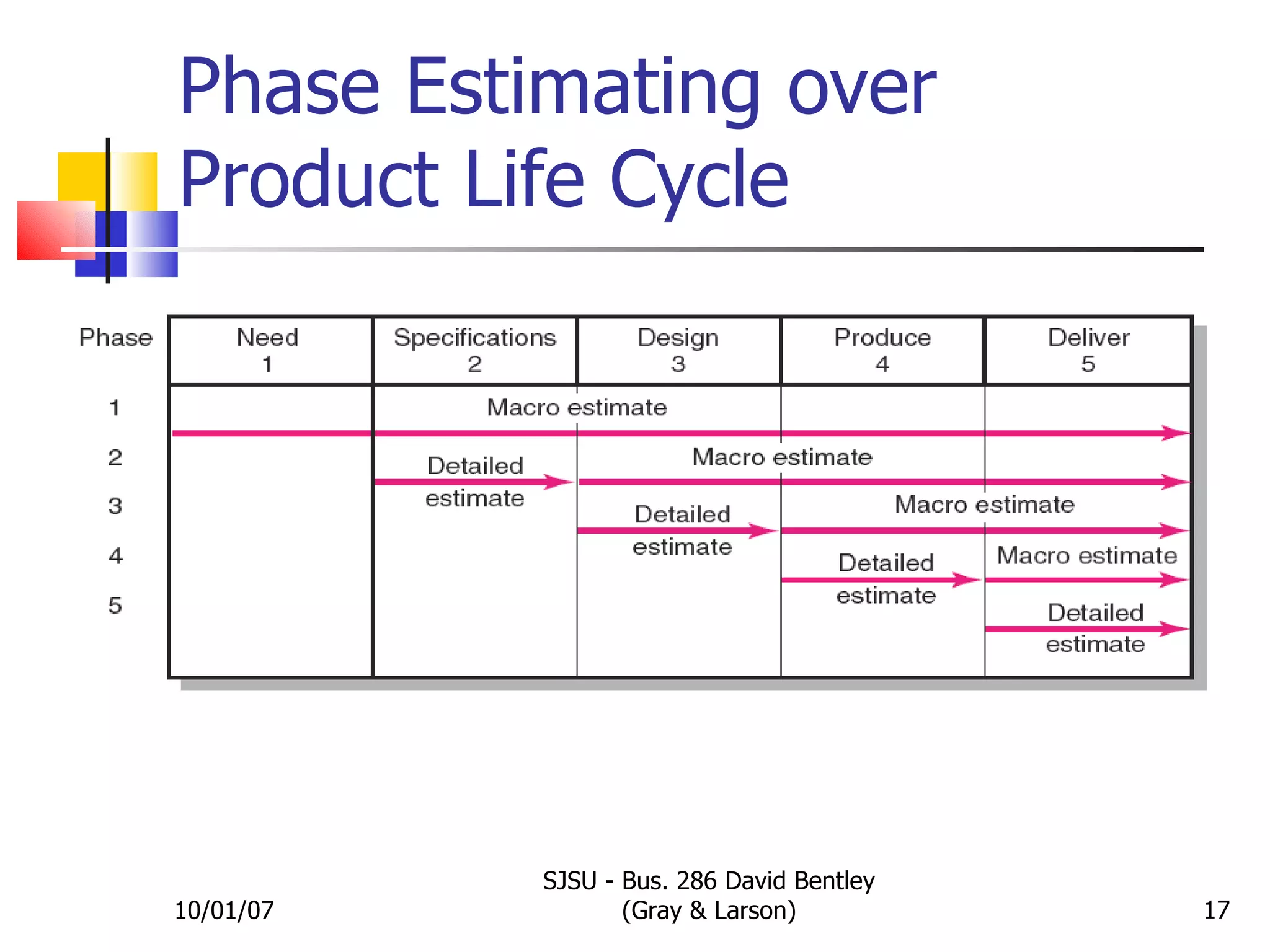

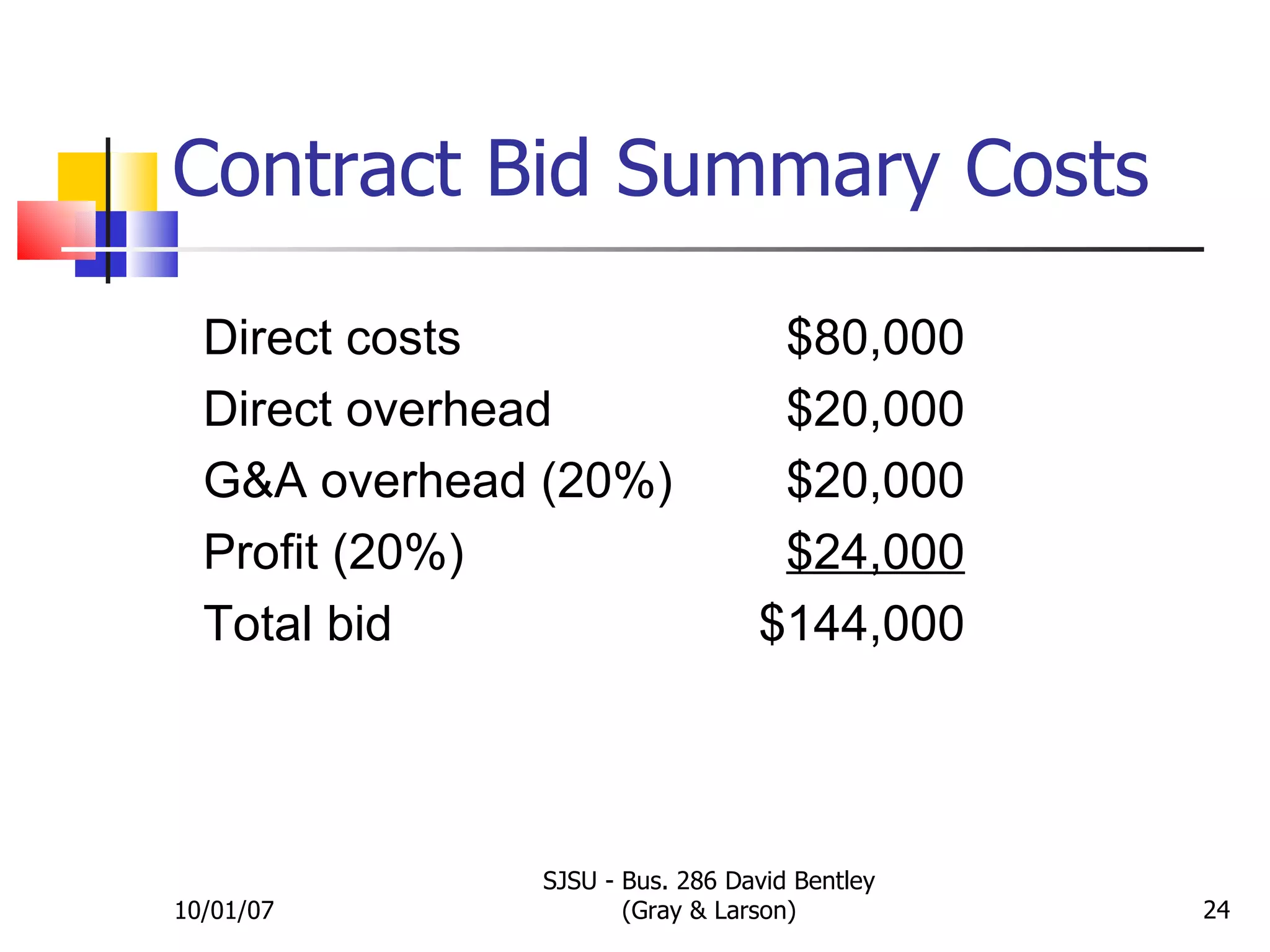

Chapter 5 discusses the process of estimating project times and costs, highlighting the types of estimates (top-down vs. bottom-up) and the factors that influence their quality. It provides guidelines for effective estimation, methods for calculating costs and timelines, and emphasizes the importance of refining estimates as project details become clearer. The chapter also differentiates between direct costs, project overhead costs, and general administrative costs.