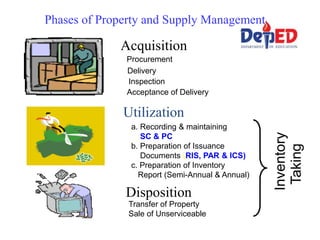

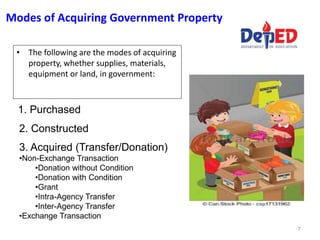

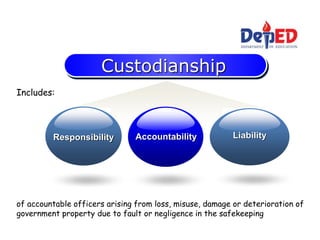

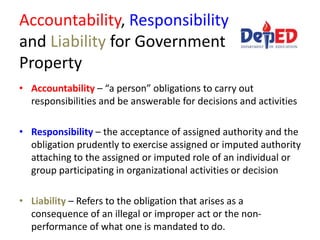

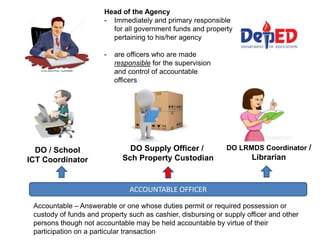

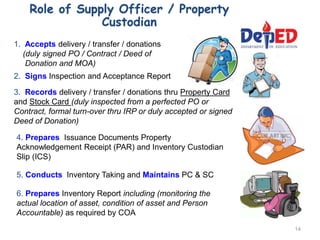

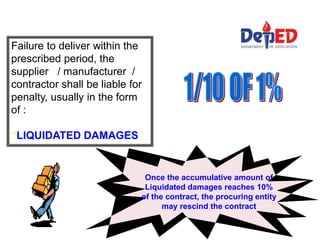

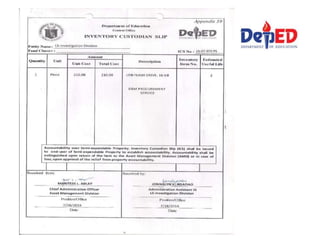

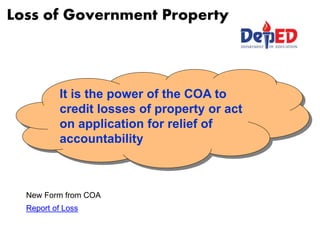

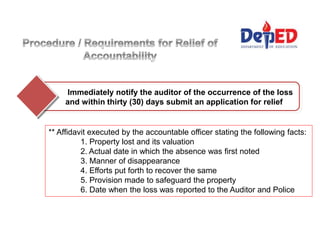

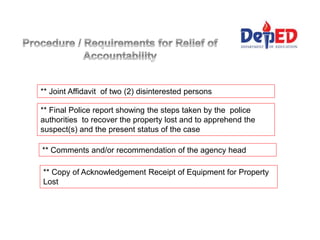

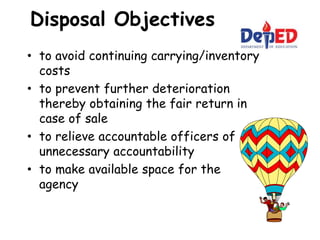

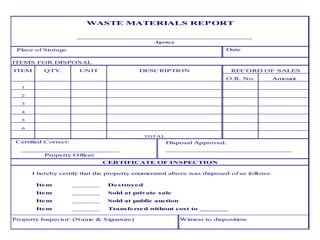

This document discusses government property management. It defines key terms like accountability, responsibility and liability. It outlines the different phases of property management including acquisition, utilization, and disposition. It describes the different modes of acquiring government property such as purchase, construction, transfer, donation. It provides details on topics like recording assets, inventory taking, relief from accountability for lost property, and disposal of unserviceable property. The document is a comprehensive reference on policies and procedures for managing government assets.