Downloaded 35 times

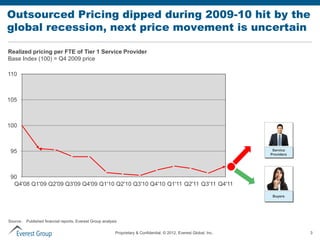

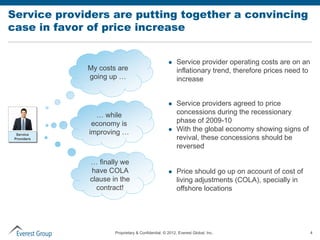

This document provides an overview of arguments made by service providers in favor of increasing IT outsourcing pricing and potential counterarguments from buyers. It discusses 3 main reasons given by service providers: 1) increasing operating costs, 2) an improving global economy, and 3) cost of living adjustment clauses in contracts. The document then presents ways buyers could potentially counter each argument, such as increasing offshore leverage or optimizing resource utilization. It aims to help buyers and service providers effectively negotiate pricing changes in outsourcing contracts.