EOP Loans & Leases

Avg Deposits

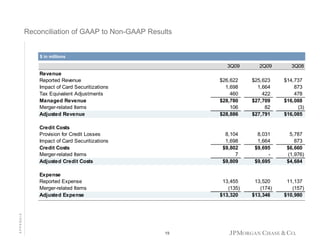

FINANCIAL RESULTS

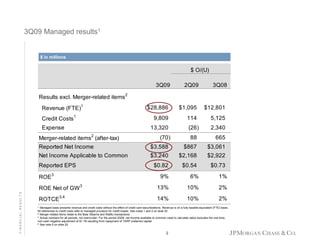

1

Actual numbers for all periods, not over/under

2 Calculated based on average equity; 3Q09 average equity was $2B

3 Excludes loans held-for-sale and loans at fair value

4 Calculated based on average equity; 3Q09 average equity was $2B

8

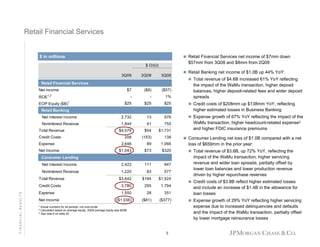

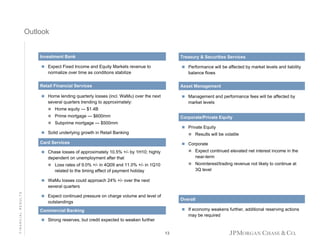

Total revenue of $1.5B up 4% YoY driven by growth in

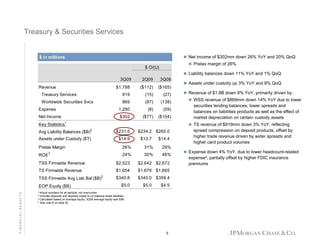

Middle Market Banking and Real Estate Banking, partially

offset by lower Commercial Term Lending revenue

Credit costs of $43mm reflect higher net charge-offs

Expense up 10

![]](https://cdn.slidesharecdn.com/ss_thumbnails/random-131208211325-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)