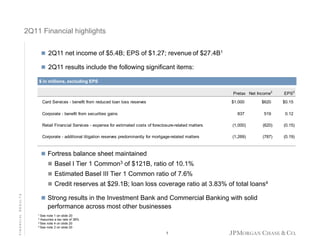

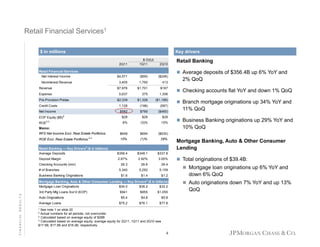

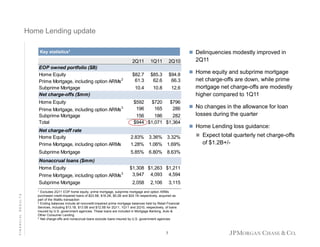

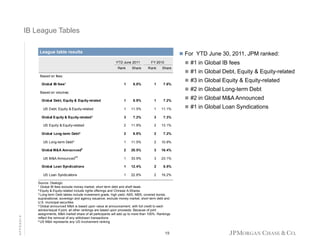

1. In 2Q11, JPMorgan Chase reported net income of $5.4 billion on revenue of $27.4 billion, with EPS of $1.27 per share.

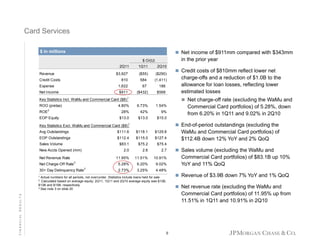

2. Significant items impacting results included a $1 billion benefit from reduced loan loss reserves in Card Services, $620 million in securities gains in Corporate, a $1 billion expense for estimated foreclosure costs in Retail Financial Services, and $787 million in additional litigation reserves in Corporate.

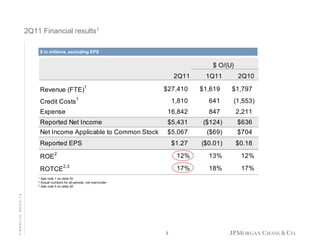

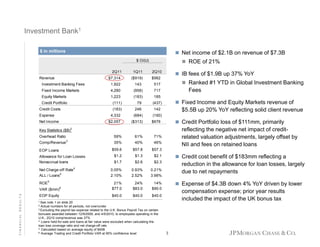

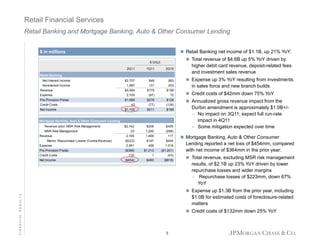

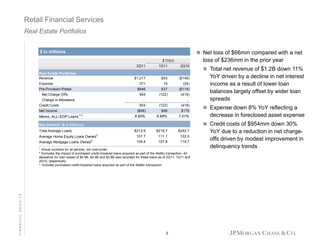

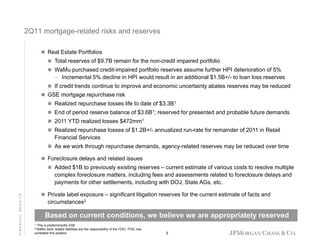

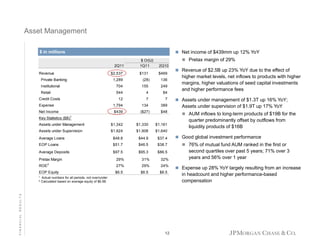

3. The Investment Bank reported net income of $2.1 billion on revenue of $7.3 billion, with strong performance across most businesses. Retail Financial Services reported a net loss of $454 million due to