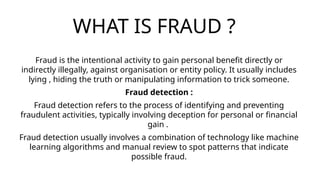

WHAT IS FRAUD?

Fraud is the intentional activity to gain personal benefit directly or

indirectly illegally, against organisation or entity policy. It usually includes

lying , hiding the truth or manipulating information to trick someone.

Fraud detection :

Fraud detection refers to the process of identifying and preventing

fraudulent activities, typically involving deception for personal or financial

gain .

Fraud detection usually involves a combination of technology like machine

learning algorithms and manual review to spot patterns that indicate

possible fraud.

3.

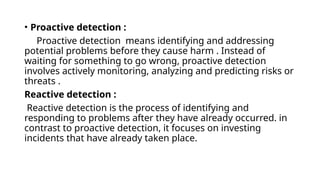

• Proactive detection:

Proactive detection means identifying and addressing

potential problems before they cause harm . Instead of

waiting for something to go wrong, proactive detection

involves actively monitoring, analyzing and predicting risks or

threats .

Reactive detection :

Reactive detection is the process of identifying and

responding to problems after they have already occurred. in

contrast to proactive detection, it focuses on investing

incidents that have already taken place.

4.

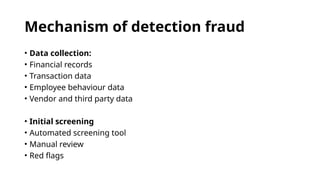

Mechanism of detectionfraud

• Data collection:

• Financial records

• Transaction data

• Employee behaviour data

• Vendor and third party data

• Initial screening

• Automated screening tool

• Manual review

• Red flags

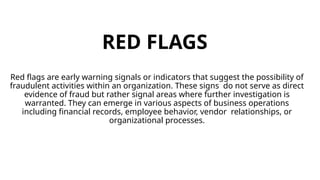

RED FLAGS

Red flagsare early warning signals or indicators that suggest the possibility of

fraudulent activities within an organization. These signs do not serve as direct

evidence of fraud but rather signal areas where further investigation is

warranted. They can emerge in various aspects of business operations

including financial records, employee behavior, vendor relationships, or

organizational processes.

8.

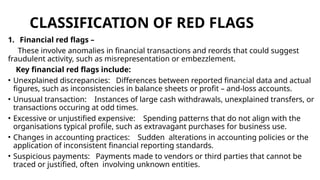

CLASSIFICATION OF REDFLAGS

1. Financial red flags –

These involve anomalies in financial transactions and reords that could suggest

fraudulent activity, such as misrepresentation or embezzlement.

Key financial red flags include:

• Unexplained discrepancies: Differences between reported financial data and actual

figures, such as inconsistencies in balance sheets or profit – and-loss accounts.

• Unusual transaction: Instances of large cash withdrawals, unexplained transfers, or

transactions occuring at odd times.

• Excessive or unjustified expensive: Spending patterns that do not align with the

organisations typical profile, such as extravagant purchases for business use.

• Changes in accounting practices: Sudden alterations in accounting policies or the

application of inconsistent financial reporting standards.

• Suspicious payments: Payments made to vendors or third parties that cannot be

traced or justified, often involving unknown entities.

9.

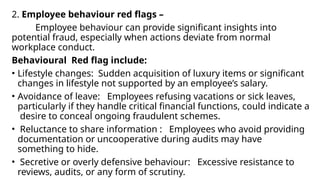

2. Employee behaviourred flags –

Employee behaviour can provide significant insights into

potential fraud, especially when actions deviate from normal

workplace conduct.

Behavioural Red flag include:

• Lifestyle changes: Sudden acquisition of luxury items or significant

changes in lifestyle not supported by an employee’s salary.

• Avoidance of leave: Employees refusing vacations or sick leaves,

particularly if they handle critical financial functions, could indicate a

desire to conceal ongoing fraudulent schemes.

• Reluctance to share information : Employees who avoid providing

documentation or uncooperative during audits may have

something to hide.

• Secretive or overly defensive behaviour: Excessive resistance to

reviews, audits, or any form of scrutiny.

10.

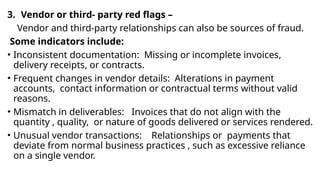

3. Vendor orthird- party red flags –

Vendor and third-party relationships can also be sources of fraud.

Some indicators include:

• Inconsistent documentation: Missing or incomplete invoices,

delivery receipts, or contracts.

• Frequent changes in vendor details: Alterations in payment

accounts, contact information or contractual terms without valid

reasons.

• Mismatch in deliverables: Invoices that do not align with the

quantity , quality, or nature of goods delivered or services rendered.

• Unusual vendor transactions: Relationships or payments that

deviate from normal business practices , such as excessive reliance

on a single vendor.

11.

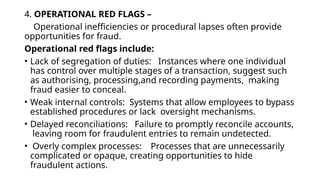

4. OPERATIONAL REDFLAGS –

Operational inefficiencies or procedural lapses often provide

opportunities for fraud.

Operational red flags include:

• Lack of segregation of duties: Instances where one individual

has control over multiple stages of a transaction, suggest such

as authorising, processing,and recording payments, making

fraud easier to conceal.

• Weak internal controls: Systems that allow employees to bypass

established procedures or lack oversight mechanisms.

• Delayed reconciliations: Failure to promptly reconcile accounts,

leaving room for fraudulent entries to remain undetected.

• Overly complex processes: Processes that are unnecessarily

complicated or opaque, creating opportunities to hide

fraudulent actions.

12.

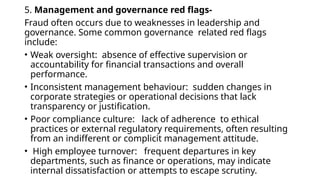

5. Management andgovernance red flags-

Fraud often occurs due to weaknesses in leadership and

governance. Some common governance related red flags

include:

• Weak oversight: absence of effective supervision or

accountability for financial transactions and overall

performance.

• Inconsistent management behaviour: sudden changes in

corporate strategies or operational decisions that lack

transparency or justification.

• Poor compliance culture: lack of adherence to ethical

practices or external regulatory requirements, often resulting

from an indifferent or complicit management attitude.

• High employee turnover: frequent departures in key

departments, such as finance or operations, may indicate

internal dissatisfaction or attempts to escape scrutiny.

13.

TECHNIQUES OF FRAUD

DETECTION

1.Horizontal analysis: horizontal analysis also known as trend

analysis, is a valuable tool used to evaluate financial data across

multiple periods, offering insights into trends, anomalies and

unusual changes that may signal fraud. By examining fluctuations

in financial accounts, organisations can identify patterns that

deviate from expected behaviour prompting further

investigation.

14.

KEY COMPONENTS OFHORIZONTAL ANALYSIS IN FRAUD

DETECTION

1. Trend identification: horizontal analysis helps uncover abrupt

increases or decreases in key financial metrics, such as revenue,

expenses or asset balances . Unusual trends may point to fraudulent

activities, including revenue inflation or cost management.

• Example : A significant increase in revenue without a proportional rise

in accounts receivable or inventory could indicate fictitious sales.

2. Pattern analysis: Auditors analyze consistency in financial growth

over time. Fraudsters may try to manipulate data to show

unrealistically positive results, leading to irregular patterns.

• Example: A sudden spike in revenue during a typically slow season,

without a corresponding uptick in customer orders, could raise

suspicion.

15.

3. Focus onsuspicious line items: Certain line items, such as

accounts receivable, inventory, or expenses, may display

disproportionate changes year over year. These shifts could

signal fraudulent practices like false billing, skimming, or

inventory theft.

• Example: A sharp increase in inventory but no

corresponding increase in sales could suggest

overstatement of inventory to manipulate financial ratios.

16.

STEPS FOR USINGHORIZONTAL

ANALYSIS IN FRAUD DETECTION

1. Gather historical data : Collect financial statements for

multiple periods to ensure sufficient data for comparison.

2. Identify unusual variances: Look for significant year over

year changes in key accounts.

3. Investigate further: For accounts with unusual changes,

analyze underlying documentation, such as invoices,

contracts, or transaction records, to verify authenticity.

4. Correlate metrics: Ensure consistency between related

accounts (e.g revenue, receivables and cash flow).

17.

Vertical Analysis

Vertical analysis,also known as common size analysis, is a

financial tool that helps to assess the relative size of each item

within a financial statement, typically by expressing each line

item as a percentage of a base figure. In the case of an income

statement, this would involve calculating the percentage of each

expense item relative to total revenue. In a balance sheet,

vertical analysis expresses each asset, liability, and equity item

as a percentage of total assets. This method is particularly useful

in identifying discrepancies and inconsistencies in the structure of

financial statements, which may indicate fraudulent activity.

18.

Role Of VerticalAnalysis

Vertical analysis plays a crucial role in:

1. Financial statement analysis: It helps analyze financial

statements, identifying trends and patterns.

2. Comparison: Enables comparison between companies,

industries, or time periods.

3. Decision-making: Informs business decisions, investments,

or lending.

4. Identifying areas for improvement: Highlights areas of

strength and weakness in financial performance.

By using vertical analysis, stakeholders can gain valuable

19.

Prevention Of Fraud

Fraudprevention involves implementing strategies to deter,

detect, and mitigate fraudulent activities, safeguarding assets

and data. It's a proactive approach that includes establishing

strong internal controls, conducting thorough background checks,

providing fraud awareness training, and using technology for

monitoring and analysis. A comprehensive fraud prevention

program also involves incident response planning and regular

audits to identify weakness and improve existing measures.

20.

Strategies Organizations CanUsed To

Prevent Fraud

Here are some strategies to prevent fraud:

1. Implement Strong Internal Controls: Establish policies, procedures, and

systems to prevent and detect fraud.

2. Conduct Regular Audits: Perform regular audits to identify and address

potential fraud risks.

3. Train Employees: Educate employees on fraud prevention and detection

techniques.

4. Use Technology: Implement technology solutions, such as data analytics

and AI, to detect and prevent fraud.

5. Monitor Transactions: Regularly monitor transactions for suspicious activity.

21.

6. Implement AccessControls: Limit access to sensitive data

and systems based on user roles and permissions.

7. Encourage Whistleblowing: Create a culture where

employees feel comfortable reporting suspicious activity.

8. Conduct Background Checks: Perform background checks

on employees and vendors.

9. Implement Anti-Fraud Policies: Develop and enforce anti-

fraud policies and procedures.

10. Stay Up-to-Date with Regulations: Stay informed about

regulatory changes and industry best practices.

By implementing these strategies, organizations can reduce the

risk of fraud and protect their assets.

22.

STRATEGIES ORGANISATION CANUSE TO PREVENT FRAUD

Implementing Robust Internal Controls to Prevent Fraud

Internal controls play a critical role in preventing fraud by ensuring that all financial transactions and activities are

authorized recorded, and monitored. These controls are designed to safeguard an organization's assets, enhance the

reliability of financial reporting, and en compliance with laws and regulations, Effective internal controls help minimize

opportunities for fraudulent activities by creating checks and balances within the organization's operation framework.

A. Segregation of duties: Reducing the Risk of fraud

Segregation of duties (SOD) is one of the cornerstones of an effective internal control sym It is a preventive measure

that ensures no single employee has the authority to execute multiple critical steps of a financial transaction. By

dividing responsibilities among different individual organizations can reduce the risk of fraud, as no one person has

complete control over the process.

Key Aspects of Segregation of Duties

Authorization: The employee who authorizes a payment should not be the same as the one who records the

transaction or handles the cash.

Custody: Those responsible for handling physical assets, such as cash or inventory, should not be involved in

recording the transactions related to those assets.

Recording: The person responsible for accounting and recording transactions should nut be involved in

authorizing payments or handling assets.

23.

. Authorization andApproval Processes: Clear Levels of Approval

Establishing clear levels of authorization and approval for financial transactions is a crucial element of internal controls. By specifying who can

approve different types of transactions and at what levels, organizations can ensure that financial decisions are subject to appropriate scrutiny.

Key Components of Authorization and Approval Processes

(1) Authorization Hierarchy:

Define levels of authority within the organization to ensure that only certain individuals are authorized to approve specific transactions. For

instance, low-value expenses may be approved by department managers, while lass or unusual transactions should require the approval of

senior management or the board.

Transaction Limits

Establish thresholds for approval based on transaction amounts Transactions above a certain threshold should require multiple approvals or be

subjected to more rigorous review.

Review of Unusual Transactions:

Large or unusual transactions, especially those that fall outside regular business practices, should undergo additional scrutiny. This helps identify

potential fraud or errors early. For example, payments made to new vendors outside normal operational channels should be verified by more

than one individual.

C. Access Controls: Protecting Sensitive Financial Systems

Access controls are essential for safeguarding an organization's critical financial data ensuring that only authorized individuals have access to

sensitive systems and information. This is particularly important in the digital age , where financial information is stored and processed

electronically.

24.

Key Components ofAccess Controls

(i) Role-Based Access: Assign access to financial systems based on the employee's role within the organization. For example, a

staff member responsible for payroll should not have access to accounting systems that record sales transactions.

(ii) Least Privilege Principle: Limit access to the minimum level necessary for an employee to perform their tasks. This reduces

the risk of unauthorized access modification of critical data.

(iii) Password Protection: Ensure strong password policies that require employees to use complex passwords and change them

regularly. Weak passwords are an easy target for fraudsters to gain unauthorized access.

(iv) Two-Factor Authentication (2FA) Implement two-factor authentication for systems that store sensitive financial

information or process transactions. This adds an additional layer of security by requiring employees to provide two forms of

identification-something they know (a password) and something they have (a token or mobile device).

D. Integrating These Controls into a Holistic Fraud Prevention System

Together, segregation of duties, authorization and approval processes, and access controls form a robust system of internal controls

that can prevent fraud at various levels within the organization. These controls should not operate in isolation but rather be part of

an integrated fraud prevention framework that includes continuous monitoring, regular audits, and strong reporting mechanisms.

Holistic Fraud Prevention

(i) Continuous Monitoring: Ongoing monitoring of financial activities, especially high-risk transactions, ensures that any

irregularities or anomalies are detected in real-time.

(ii) Regular Audits: Periodic internal and external audits help ensure that internal controls are being followed and that there are

no significant weaknesses in the control systems

25.

(iii) Reporting Mechanisms:Establishing clear reporting channels (such as whistleblower hotlines) allows employees to report suspected

fraud or violations of internal cod without fear of retaliation

3. Regular Audits and Inspections: A Key Fraud Prevention Strategy

Audits are an essential part of a robust fraud detection and prevention strategy. They serve as a mechanism to assess the integrity of an

organization's financial processes, ensure compliance with policies, and identify potential fraud or operational inefficiencies Regular audits

help organizations stay vigilant, maintaining transparency and accountability within their systems.

(i)Internal Audits: Internal audits are a vital component of an organization's internal control system. Conducted by the company's own

auditing team or designated personnel internal audits are designed to regularly review and evaluate the effectiveness of internal controls,

policies, and procedures.

The primary goal of an internal audit is to ensure that the organization is adhering to it established policies and procedures, assessing

financial transactions for accuracy, and ensuring that resources are being used efficiently.

(ii) External Audits :- provides an unbiased evaluation of the company's financial statements, they are a true and fair representation of the

organization's helping to ensure that financial position,

The primary function of an external audit is to give stakeholders such as shareholders, regulators, and investors-confidence that the

company's financial statements are accurate and reliable External auditors are also responsible for reviewing the internal control ensure they

are adequate and functioning properly.

(iii) Surprise Audits: Surprise audits, or unscheduled inspections, are conducted without prior notice to the employees or departments being

audited. The unpredictable nature of surprise audits serves as an effective deterrent against fraudulent behavior as employees are aware

that they could be audited at any time.

The primary purpose of surprise audits is to keep employees on their toes and ensure that organizational processes are being followed

consistently.

26.

4. Implementing FraudDetection Tools and Technology

A. Transaction Monitoring Systems: Transaction monitoring systems are automated tools

that track financial transactions in real time to detect irregularities or suspicious activities.

The Key aspects of this system are:

(i) Real-Time Monitoring: These systems continuously track financial transactions, such as payments, wire

transfers, and credit card transactions, as they occur. This enables immediate detection of suspicious

transactions, including duplicate payments unauthorized transfers, or payments that exceed predefined

thresholds.

(ii) Automated Alerts: When a suspicious transaction is flagged, the system automatically generates an alert,

notifying relevant personnel, such as compliance officers of auditors, to investigate further. For example, if a

company’s policy is to limit payments over 50,000, the system will automatically alert management when a

transaction exceeds that limit without appropriate approval.

(iii) Risk-Based Analysis: Transaction monitoring tools often allow for risk-based parameter settings. This means

that transactions can be flagged based on risk levels which are determined by factors such as the location of

the transaction, the nature of the transaction, and the profile of the person involved in the transaction.

27.

B. Data Analyticsand Machine Learning:

Some of the key features and applicator’s of these technologies are:

(i) Pattern Recognition: By analyzing historical data, ML. algorithms can identify normal transaction patterns and behaviour

within the organization. Once these patterns are established, the system can quickly detect anomalies that deviate from the

norm. For instance, if an employee usually makes small transactions but suddenly processes a large payment to an

unapproved vendor, the system will flag this as unusual behaviour.

(ii) Predictive Analytics: ML tools can also predict potential fraud based on previous occurrences, using statistical models to

assess the likelihood of fraud in certain transactions or activities. These models improve over time, learning from new data

and evolving to detect increasingly sophisticated fraudulent schemes.

(iii) Anomaly Detection: By analyzing employee behaviour, purchase orders, payment histories, and financial records, data

analytics tools can uncover patterns that suggest fraud, such as an employee who repeatedly approves invoices from

unapproved vendors or someone consistently processing high-value transactions without proper documentation.

C. Continuous Monitoring:

(i) Automated Data Tracking: Continuous monitoring software tracks all financial and operational data across systems, from

procurement to sales, and flags discrepancies or unusual activities immediately. For example, if an employee repeatedly

accesses financial systems outside of working hours or alters records without proper authorization, the software can alert

security or management in real time

(ii) Proactive Fraud Detection: Continuous monitoring not only helps detect fraud in real time but also enables proactive

action to prevent potential fraudulent behaviusar.

28.

(iii) Cost andTime Efficiency: Continuous monitoring reduces the need for manual reviews, saving both time and resources.

This ensures that no potential fraud slips through the cracks, providing a more comprehensive and consistent approach to fraud

detection.

5. Whistleblower Mechanisms and Reporting Channels

A. Anonymous Reporting: Anonymity is one of the key features that makes whistleblower mechanisms effective in

fraud detection. Many employees may hesitate to report fraudulent activities due to fear of retaliation, such as

job loss, demotion, or harassment. By offering anonymous reporting options organizations provide a safe and

confidential way for employees to raise concerns without exposing themselves to personal risk. Various reporting

options are:

(i) Whistleblower Hotlines: Setting up anonymous whistleblower hotlines (either through phone calls or online

platforms) allows employees to report fraud confidentially. These hotlines can be managed internally or by a

third-party service provider to ensure impartiality and protect the anonymity of the person making the report.

(ii) Digital Platforms: In addition to phone lines, organizations can offer digital platforms that allow employees and

external stakeholders to submit reports or documents securely. These platforms may include online portals,

encrypted emails, or third-party apps specifically designed for confidential whistleblowing. The ability to submit

evidence, such as screenshots, documents, or transaction details, further strengthens the credibility of the report.

(iii) Encouragement of Use: It is important that organizations actively encourage employees to utilize these anonymous

channels by promoting them regularly. The anonymity provided by these reporting systems increases the

likelihood that employees will report unethical behaviour without fearing personal repercussions.

29.

B. Clear ReportingProcedures:

The key features of efficient reporting procedures are

(i) Accessibility: Reporting mechanisms should be easily accessible to all employees, regardless of their level within the organization or their

physical location.

(ii) Multiple Channels for Reporting: Organizations should offer various options for reporting fraud to accommodate the preferences of different

individuals

C. Protection Against Retaliation: An effective whistleblower program cannot succeed without a culture of trust and protection for those who report

fraudulent activities. One of the most critical elements in ensuring the success of whistleblower mechanisms is to guarantee that individuals

who report fraud will not face retaliation from their peers, supervisors, or management. The ways to ensure protation against retaliation are:

(i) Anti-Retaliation Policies

(ii) Legal protection

(iii) Fostering a culture of trust

(iv) Confidential and transparency

(v) 6. Employee Rotation and Mandatory Vacations: Fraud prevention is largely about minimizing the opportunities for fraudulent behaviour to take

place and go unnoticed. Employee rotation and mandatory vacations are two effective strategies that organizations can use to reduce

the risk of fraud. Both of these practices ensure that no individual maintains control over sensitive tasks for too long, making it more

difficult for fraudulent activities to be concealed.

A. Employee Rotation: Employee rotation involves periodically changing the roles or responsibilities of employees, especially those in

positions of financial control, accounting, or other areas where fraud might occur. This approach serves multiple purposes in fraud

prevention:

30.

(i) Limits Controland Access

(ii) Encourages Vigilance

(iii) Cross-Training and Knowledge Sharing

(iv) Detecting Irregularities

B. Mandatory Vacations:Mandatory vacation policies require employees to take time off from their job for a set period, which

is especially important for employees in positions with access to financial data or significant control over processes that could be

exploited for fraudulent purpose.

(i) Disruption of Continuous Fraud: Fraudulent schemes often rely on the employee’s ability to remain involved in their activities

over extended periods. By requiring employees to take mandatory vacations, their work is temporarily handed over to another person.

During this time, it may be easier to spot discrepancies or suspicious activities that the employee may have been hiding.

(ii) Detecting Hidden Fraud: When someone else takes over an employee’s responsibilities during their absence, they may uncover

fraudulent activities that were previously concealed. For example, an employee responsible for approving payments might be forging

signatures or altering records. When that employee takes a vacation, another person may notice unusual patterns or missing

documents that point to potential fraud.

(iii) Preventing Collusion: Mandatory vacations also help prevent collusion, where an employee works with others to commit

fraudulent activities. If a fraudster knows that someone else will temporarily take over their responsibilities during a mandatory break,

they may be less likely to engage in fraudulent activities in the first place. This added layer of unpredictability makes it harder to

coordinate and conceal fraud.

(iv) Ensuring Consistency and Accountability: During the employee’s absence, a temporary replacement or supervisor can review

the individual’s recent work for any signs of fraudulent activity. This ensures that the organization maintains consistent oversight over

its processes and helps identify irregularities before they lead to significant financial loss.

31.

Remaining strategies

A.Strong vendormanagement:-

1.Venter background checks- before entering into any business relationship, it is essential for organisations

to perform background checks on vendors ot assess their credibility and reliability. This includes investigating

their financial health, past performance, business practices and reputation with in the industry.

Various ways to conduct background checks are:

● Financial and legal due diligence

● Reputation and reference

● Third party audits

2. Monitoring vendor transactions -once a vendor relationship is established it’s important to regularly

monitoring and verify vendor transactions to ensure they are legitimate and un compliance in company

policy. Vendor transactions can be monitoring by:

● Reconciliation of documents

● Auditing payment schedules

● Spotting unusual patterns .

3. Establishing clear vendor contracts -clear and detailed vendor contracts are one of the most effective

ways to prevent fraud as they set expaction upfront and provide a legal framework fro dealing with non-

compliance. Well defined contracts should have following features:

● Defining expectations and deliverables

● Payment term and schedules

● Penalties for non-compliance

32.

Legal and regulatorycompliance

A.Regulatory framework- strong regulatory compliance

framework is essential for organisations to stay compliant

with law and regulations that protect stakeholder , prevent

fraudulent activities and promote financial transparency.

The following regulatory guidelines are key in India :

1.Companies act,2013:-the companies act governs

corporate governance and financial practice in india.it

require company yo maintain accurate financial records

disclose , material fact and ensure transparency in

transactions.

33.

2. Sarbanes oxleyact (sox):-

International compliance although the sarbanes oxleyact is primarily a U.S regulations,

india companies listed on U.S. stock exchange or oprating internationally are required to

comply with Sox.

3.anti-money laundering (AML)laws:-india prevention of money laundering act

(pmla) 2002governs prevention of money laundering activities. The laws mandate

organisations to follow stringent procedures to monitor and report suspicious financial

transactions ,especially in financial institutions and banks.

4. International financial reporting standards:- for multinational companies and those

with international stakeholders to IFRS standard ensure that financial statements are

transparent,reliable and free from manipulation.

34.

Legal actions andpenalties:-

1. Internal investigation and disciplinary action:-when fraud is suspected organisations most promptly initiate an internal

investigation to determine the scope of the issue and identify those responsible .the organisation may take internal action

such as-

● Suspension or termination

● Internal sanction

1. Civil and crime charges:-in India, the legal framwork allow for both civil and criminal penalties ,for fraud depending on

the nature and extent of the crime. Fraud under te India penal code(ipc) 1860can lead to criminal charges and may

face imprisonment fines are both.

● Section 420(ipc)

● Section 447 of the company's act 2013

● Penalties for non-compliance

4. Sever penalties and sanction:- fraudulent activities especially those that result in significant financial loss and

harm to stakeholders can lead to sever penalties for the organisations and its leadership.

● Corporate penalties

● Liability for directors

35.

Auditors and regulatorsrole in fraud detection and prevention

1. Auditors role:-

● Internal auditors: internal audit focus on evaluating an organisation internal control, policies and risk management systems.

● External auditors: external audit provide independent assessment of a organisations financial statements. They ensure that

financial report are accurate and free from manipulation.

● Data analytics:auditors increasingly use data analytics as a tool to enhance theirfraud detection capabilities.

● Forensic auditors: forensic auditors specialize in investigating suspected fraud cases. They collect and analyse evidence

fraudulent activities often preparing report can be used in legal proceedings.

1. Regulator’s role:-

● Monitoring compliance:regulatory bodies such as the securities and exchange board of india, reserve bank of India

(rbi)monitoring companies to ensure compliance with Financial regulation.

● Inspection and investigation:- regulator have the authority to conduct inspection and investigation into companies operations.

This includes reviewing financial record ,assessing internal control a d ensuring to law governing corporate behaviour.

● Established reporting framework:- regulatory established mandatory reporting framework that requires companies to disclose

relevant financial information.

● Imposing penalties:regulators have the authority to impose to penalties to organisations that fail to meet compliance

standards.

36.

Financial Statement Fraud

Financialstatement fraud refers to the deliberate misrepresentation or omission of material information from a

company’s financial reports, leading to an inaccurate portrayal of its financial health.

Impact of Financial Statement Fraud

1. Impact on Investors

I. Financial Loses and Erosion of Trust:- Misleading financial reporting leads them to make

investment decision based on accurate information, resulting in financial losses. When the fraud

was exposed, investors suffered significant losses as stock prices plummeted. The trust of

investors in the company and its management is severely undermined and creates a perception

of an untrustworthy financial ecosystem.

II. Long Term Consequences: It can cause long term damage to investors confidence, especially if a

fraud is significant or widespread.

III. Example:- Satyam Computers

2. Impact on Creditors

I. Increased Risk and Financial Losses: Creditors, including banks, lenders and suppliers, are

impacted by financial statement fraud as they base their lending and credit decisions on the

financial health of the company.

II. Regulatory Scrutiny & Cost:- Creditors are also impacted by the increased regulatory scrutiny

following major fraud cases.

37.

3. Impact onEmployees

I. Job Loss & Career Uncertainty: Employees of companies that are caught in fraud scandals face the direct

impact of job losses, salary cuts and a general loss of job security.

II. Erosion of Workplace Morale:- Employee may feel betrayed by management, especially if they were

unaware of the fraudulent activities.

III. Example:- Kingfisher Airlines

4. Impact on Regulators

I. Increased Pressure and Costs:- Fraudulent activities force regulators to intensify their scrutiny of

companies, leading to an increase in compliance costs for both the regulators and the company oversee.

II. Loss of Credibility and Investor confidence: When frauds are not detected in time, the credibility of

regulators is called into question. Investors and the public lose confidence in the regulatory frameworks

designed to protect them, which can undermine the functioning of the entire financial system.

5. Impact on the Trust & Credibility of Financial Markets

I. General Decline in Market Confidence

II. Long Term Market Consequences

38.

Role of Auditors

1.Assessing the Risk of Material Misstatements.

I. This Process involves understanding the company’s internal controls, the nature of its operations, and its financial

reporting environment. The goal is to identify areas where fraud is more likely to occur.

Factors Influencing Fraud Risk Assessment:

II. Incentives and Pressure

III. Opportunities for Fraud

IV. Attitudes and Rationalizations

V. Complex Transactions

2. Procedures to Identify Fraudulent Activities.

I. Analytical Procedures

II. Examination of Supporting Documentation

III. Fraud Risk Interviews

IV. Testing of Internal Controls

V. Special Forensic Procedures

VI. Review of Related Party Transactions

39.

Audit Failures andSuccesses in Detecting Fraud

Audit Failures:- Some major examples of Audit Failure are under:-

• Satyam Scandal:- where the company’s founder Ramalinga Raju, falsely inflated the company’s revenue

and profits. Auditors(PWC-Price water house Coopers) were responsible for checking Satyam’s financial

statements, they failed to detect the fraud. As a result, the financial statements overstated cash balances

by over $1 Billion, leading to massive collapse.

Audit Successes:- Some examples from real life of Audit Success are presented below

• Tata Group Companies:- The auditors of the Tata Group, one of India’s most respected corporate group ,

have consistently upheld high standards of integrity in detecting fraudulent activities. For Example: when

an issue regarding the misappropriation of funds at Tata Motors was suspected, the auditors performed

detailed tests on internal controls, preventing the issue from escalating into a full- Blown fraud.

40.

Financial statements frauds

Financialstatement fraud refers to the deliberate misrepresentation or omission of

material information from a company's financial reports, thereby misrepresenting its

financial health. Such fraud undermines confidence in financial reporting, harms

investors and leads to legal consequences. High profile corporate scandals in India

have highlighted the prevalence of financial statement fraud. The types of fraud that

occur in financial statements are discussed in detail below.

41.

India hasestablished a comprehensive legal and regulatory framework to

prevent and report financial statement fraud. This framework consists of

laws, regulations and provisions designed to ensure transparency,

accountability and fairness in financial reporting. The major components

include the Companies Act, 2013, Securities and Exchange Board of India

(SEBI) regulations and the role of forensic auditors. Each of these

components plays a vital role in promoting ethical business practices and

detecting financial fraud.

Legal and regulatory framework in

india

42.

The companies Act,2013

1. Key provisions relevent to financial statement fraud

2. Securities and exchange board of India (SEBI )

regulations

Role of forensic auditors

Forensic auditing has gained prominence as a specialized field that focuses on

investigating financial fraud. Forensic auditors conduct detailed investigations to identify

discrepancies, irregularities or fraud in a company’s financial statements. Their role is

particularly important when fraud is suspected that is not immediately detectable through

regular financial auditing.

1. Road detection

2. Financial statement verification

3. Litigation support

4. Reporting and recommendations

43.

Impact and effectivenessof the legal and

regulatory framework

The legal and regulatory framework in India, which aims to prevent financial statement

fraud, has both its strengths and weaknesses. While significant progress has been made

in improving transparency and accountability through laws such as the Companies Act,

2013 and the SEBI Regulations, there are still challenges that limit the effectiveness of

these measures. Let us take a deeper look at both the strengths and weaknesses of the

current system.

44.

Strength of thelegal and regulatory

framework

1. Increased transparency

2. Stronger corporate governance

3. Deterrence through penalties

4. Active enforcement

45.

Weakness of thelegal and regulatory

framework

1. Delay in legal proceedings

2. Limited resources for enforcement

3. Weakness in internal controls

46.

Types of auditevidence for detecting

financial statement fraud

1. Documentary evidence

2. Physical evidence

3. Third party confirmations

4. Management and employee interviews

5. Analytical procedures

47.

Auditor procedures fordetecting

fraud

Analytical procedures

1. Horizontal and vertical analysis

2. Ratio analysis

3. Trend analysis

Substantive testing

1. Test of transactions

2. Test of balances

3. Cut off testing

Forensic audit methods

1. fraud detection software

2. Document examination

3. Data mining