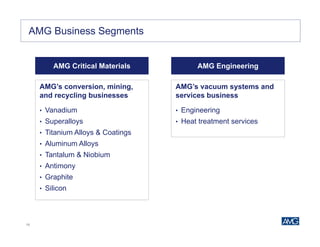

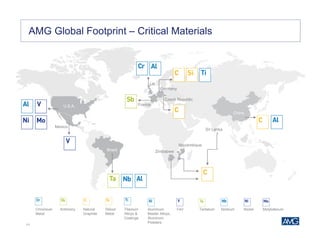

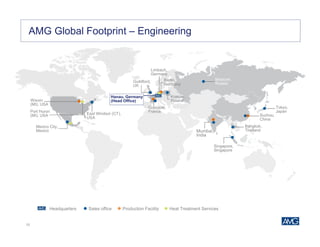

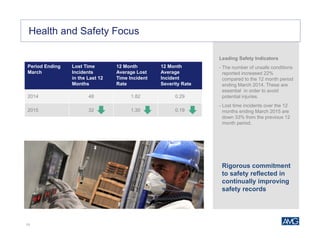

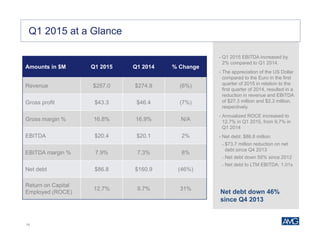

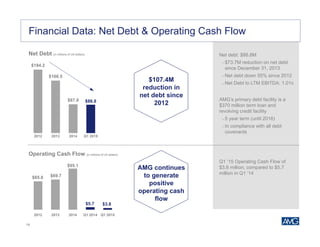

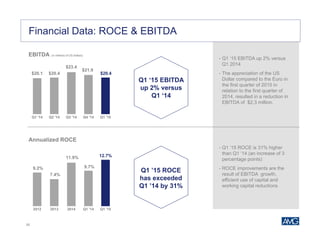

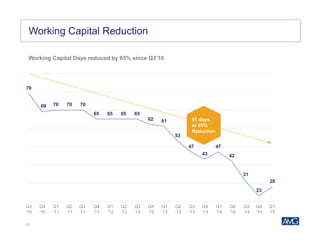

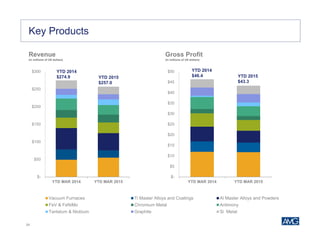

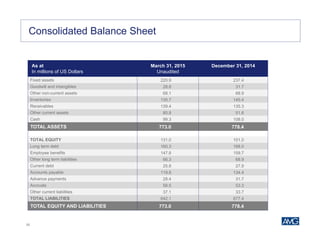

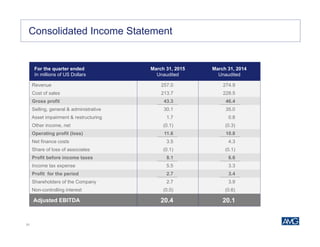

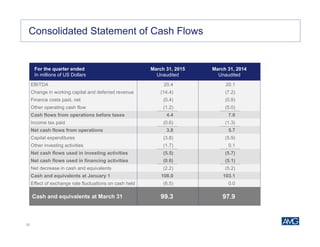

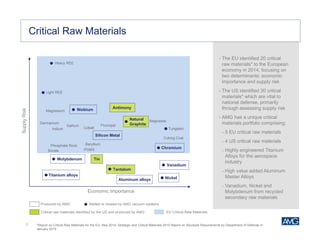

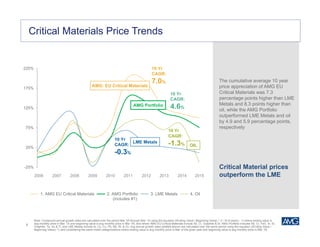

This investor presentation by AMG provides an overview of the company and the critical materials industry. AMG is a global leader in supplying critical materials to industries like aerospace, electronics, and clean energy. It has production facilities and sales offices around the world. The presentation discusses key global trends driving increased demand for critical materials, such as CO2 emission reduction and new technologies. It also outlines AMG's business segments, product portfolio, and financial highlights. Overall, the presentation aims to introduce investors to AMG's position as an expert in critical materials and its global operations.

![9

1.7

0.6 0.8 0.7

3.5

1.2

1.7

4.5

5.7

1.8

0

2.5

5

7.5

10

Scale

Metals

Note: Metal Positions are measured on a scale of 0 to 10, with 0 being the minimum price and 10 being the maximum price. They are calculated using the formula [(Mar 2005 month avg –

min. monthly avg) / (max. monthly avg – min. monthly avg) *10] where maximum and minimum monthly averages are measured over the period 1 Mar 2005 through 31 Mar 2015.

Critical Materials Prices: 10 Year Perspective

• Metal prices are measured on a

scale of 0 to 10, with 0 and 10

representing the minimum and

maximum average quarterly

prices occurring during the past

10 years

• The positions demonstrate the

current price level of each metal

with respect to their various

historical price points over the

past 10 years

AMG has significant

potential upside within

certain critical materials

based on historical price

ranges

Cr

Mo Ni FeV

Ti

Sponge

Al

Si

Ta

Sb

Spec. Metals & Chem.Energy Transportation Infrastructure

Graphite](https://image.slidesharecdn.com/2015mayamginvestorpresentation-150507151645-lva1-app6892/85/Investor-Presentation-May-2015-9-320.jpg)