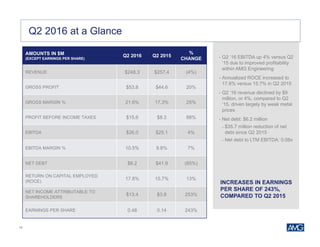

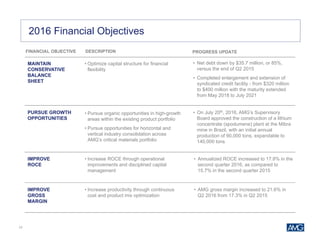

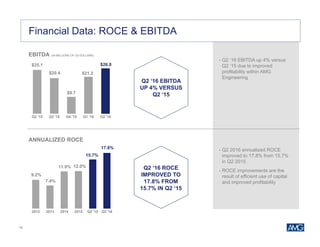

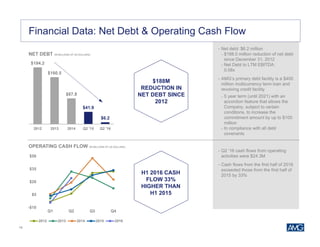

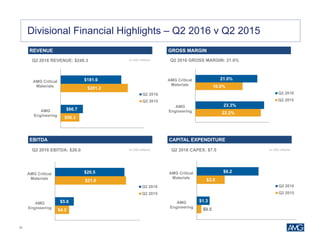

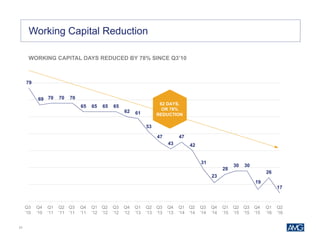

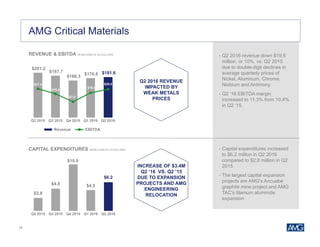

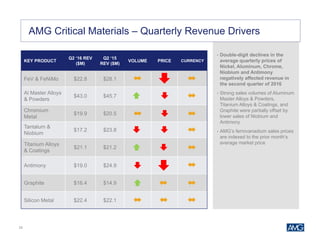

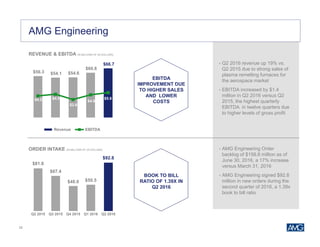

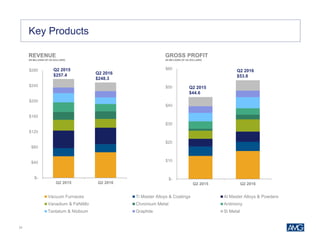

The document is an investor presentation by AMG Advanced Metallurgical Group N.V. that provides an overview of the company. It discusses AMG's business segments which involve sourcing, processing, and supplying critical raw materials. It highlights AMG's focus on enabling technologies to reduce CO2 emissions and notes several critical raw materials identified by the EU and US that AMG produces. The presentation provides financial highlights for Q2 2016, showing increases in earnings per share, EBITDA, and gross profit compared to Q2 2015. It outlines AMG's 2016 financial objectives of improving return on capital employed and gross margin while pursuing growth opportunities and maintaining a conservative balance sheet.

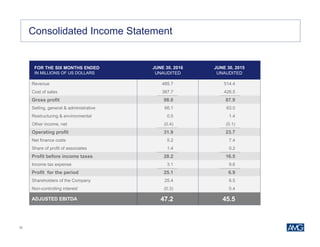

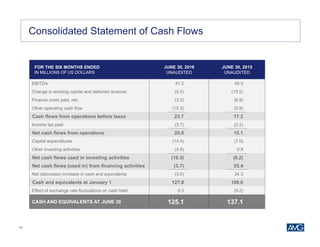

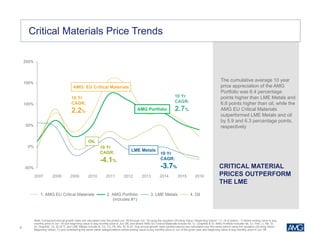

![9

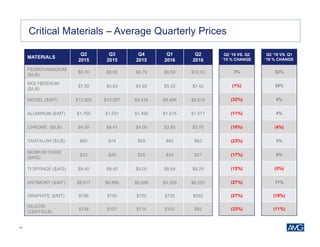

Critical Materials Prices: 10 Year Perspective

AMG has significant

potential upside within

certain critical materials

based on historical price

ranges

Note: Metal Positions are measured on a scale of 0 to 10, with 0 being the minimum price and 10 being the maximum price. They are calculated using the formula [(Jun ‘06 month avg –

min. monthly avg) / (max. monthly avg – min. monthly avg) *10] where maximum and minimum monthly averages are measured over the period 1 Jun ‘06 through 30 Jun ‘16.

1.9

1.2

0.3

1.5

2.5

1.7

0.9

1.7

5.8

0.8

1.8

3.9

0.8

1.1 1.1

4.5

2.1 2.2

5.3

5.8

1.7

3.2

0

2.5

5

7.5

10

Scale

Metals

Jun 2016 Position Jun 2015 Position

Cr Mo Ni FeV Ti Al C Si Ta Sb

Highest

Price in

10 years

Lowest

Price in

10 years

[unchanged]

• Metal prices are measured on a

scale of 0 to 10, with 0 and 10

representing the minimum and

maximum average quarterly

prices occurring during the past

10 years

• The positions demonstrate the

current price level of each metal

with respect to their various

historical price points over the

past 10 years

Nb](https://image.slidesharecdn.com/amginvestorpresentationaugust2016final-160804133809/85/AMG-Investor-Presentation-August-2016-9-320.jpg)