Download to read offline

The document discusses menu planning and cost control. It provides definitions of key terms like menu and explains that effective menu planning requires considering guests' needs as well as the financial goals of the foodservice operation. It also discusses how understanding standard product costs allows managers to know how much it should cost to produce each menu item. Finally, it explains that after standard costs are established, managers can use various pricing methods like markups or contribution margin pricing to determine selling prices for menu items.

Introduction to Menu Planning and Cost Control in food service operations.

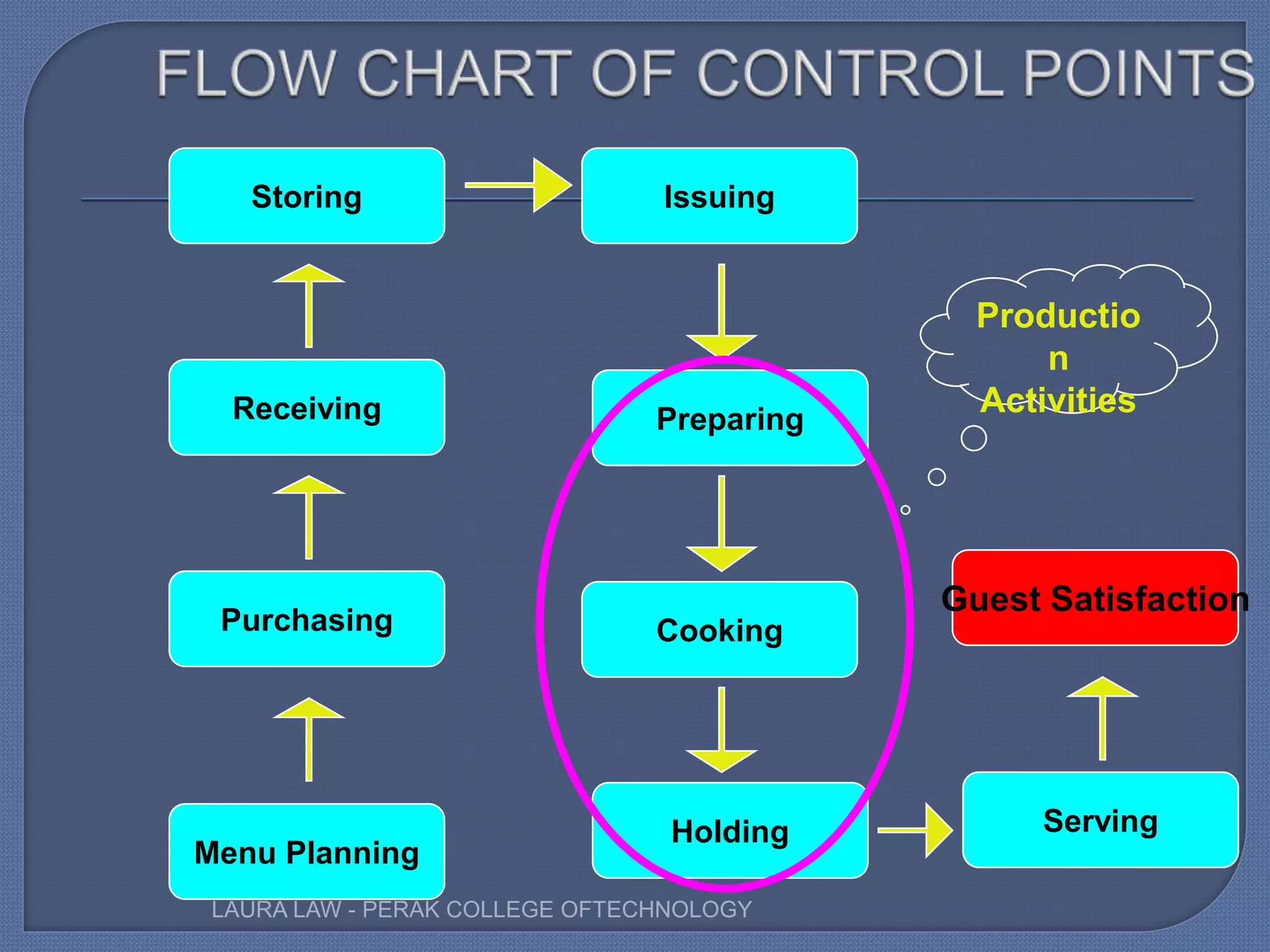

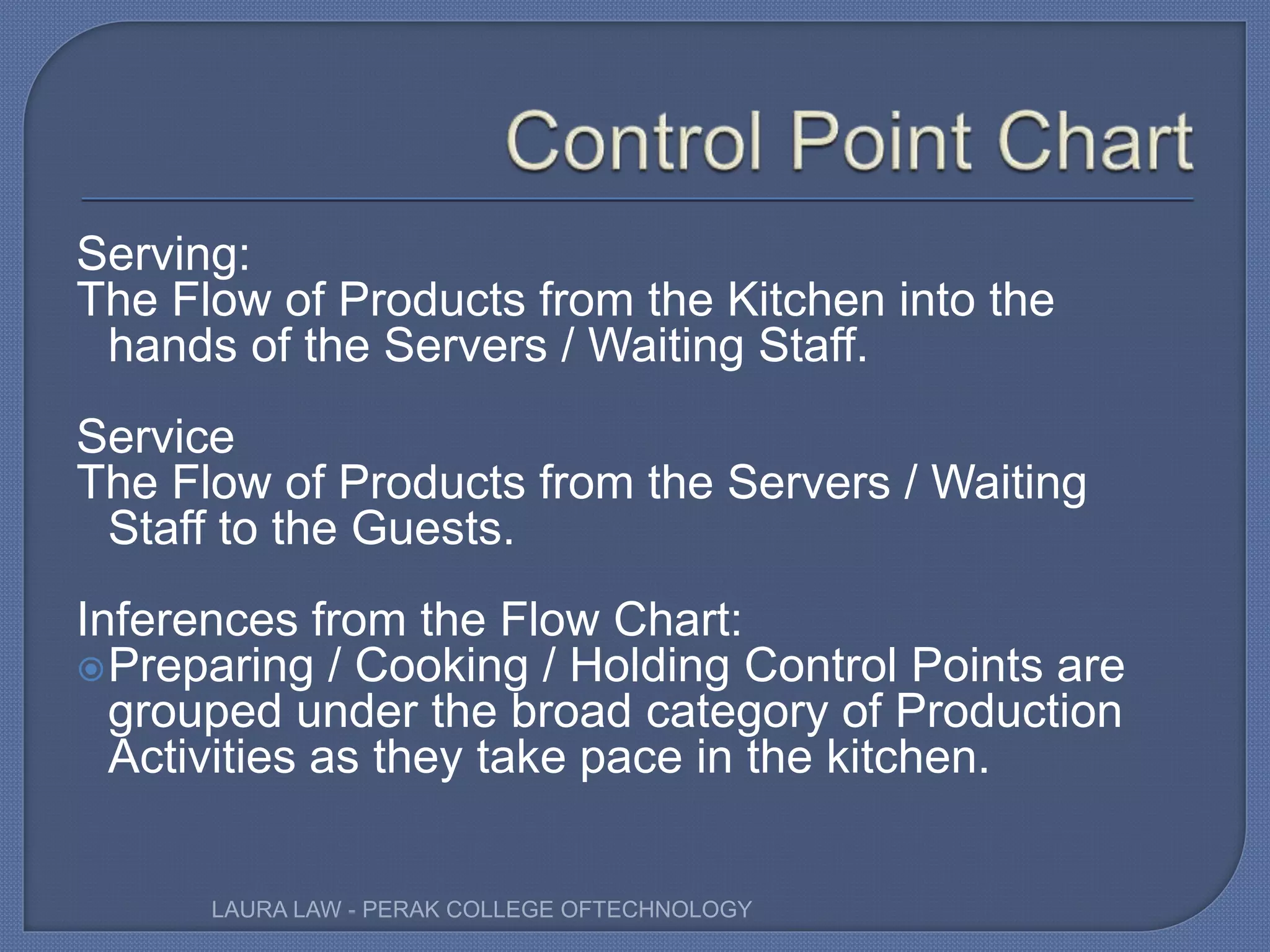

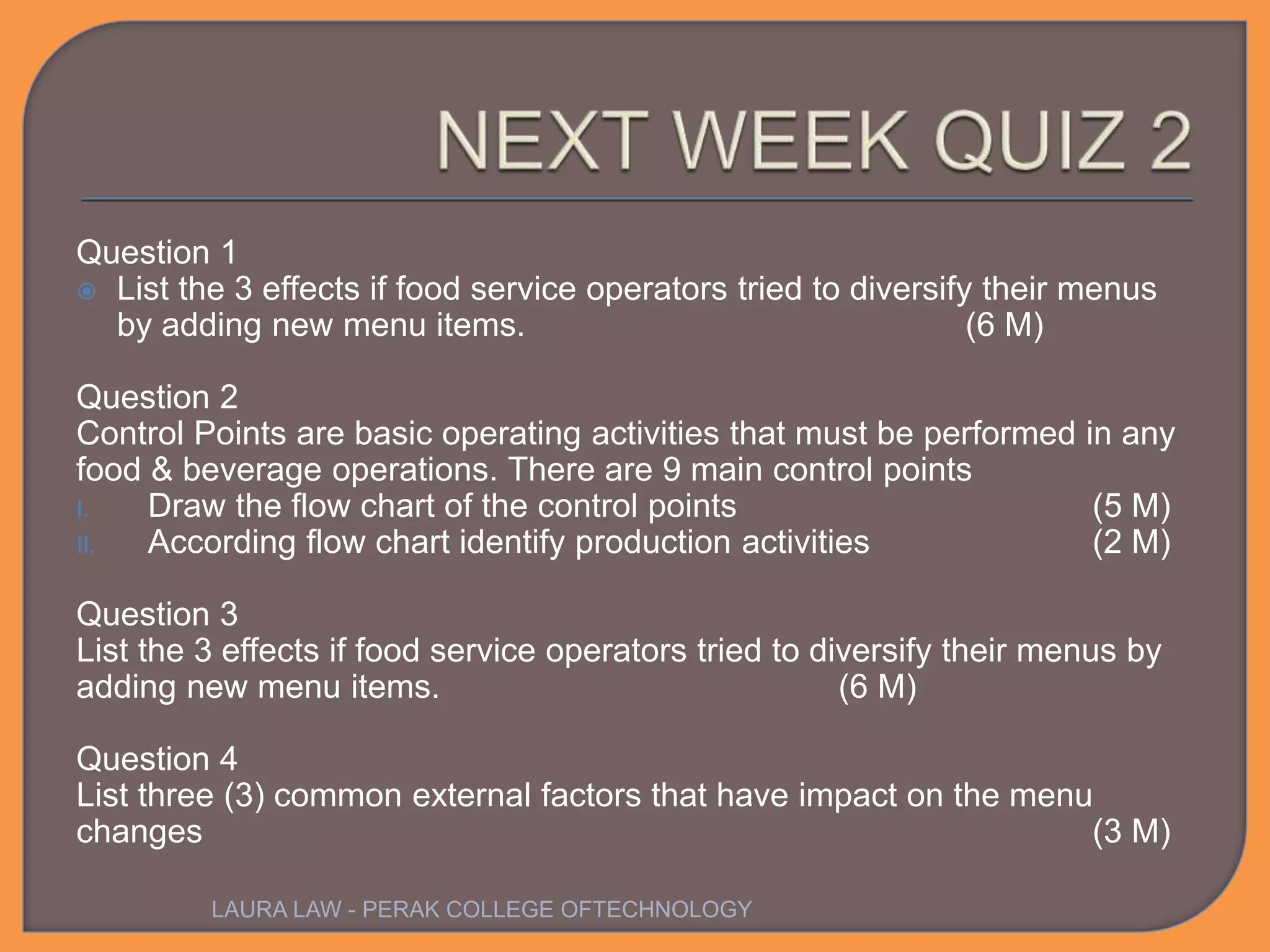

Identifies 9 main control points crucial for success in food & beverage operations.

Describes the production activities and ongoing nature of menu planning focusing on guest satisfaction.

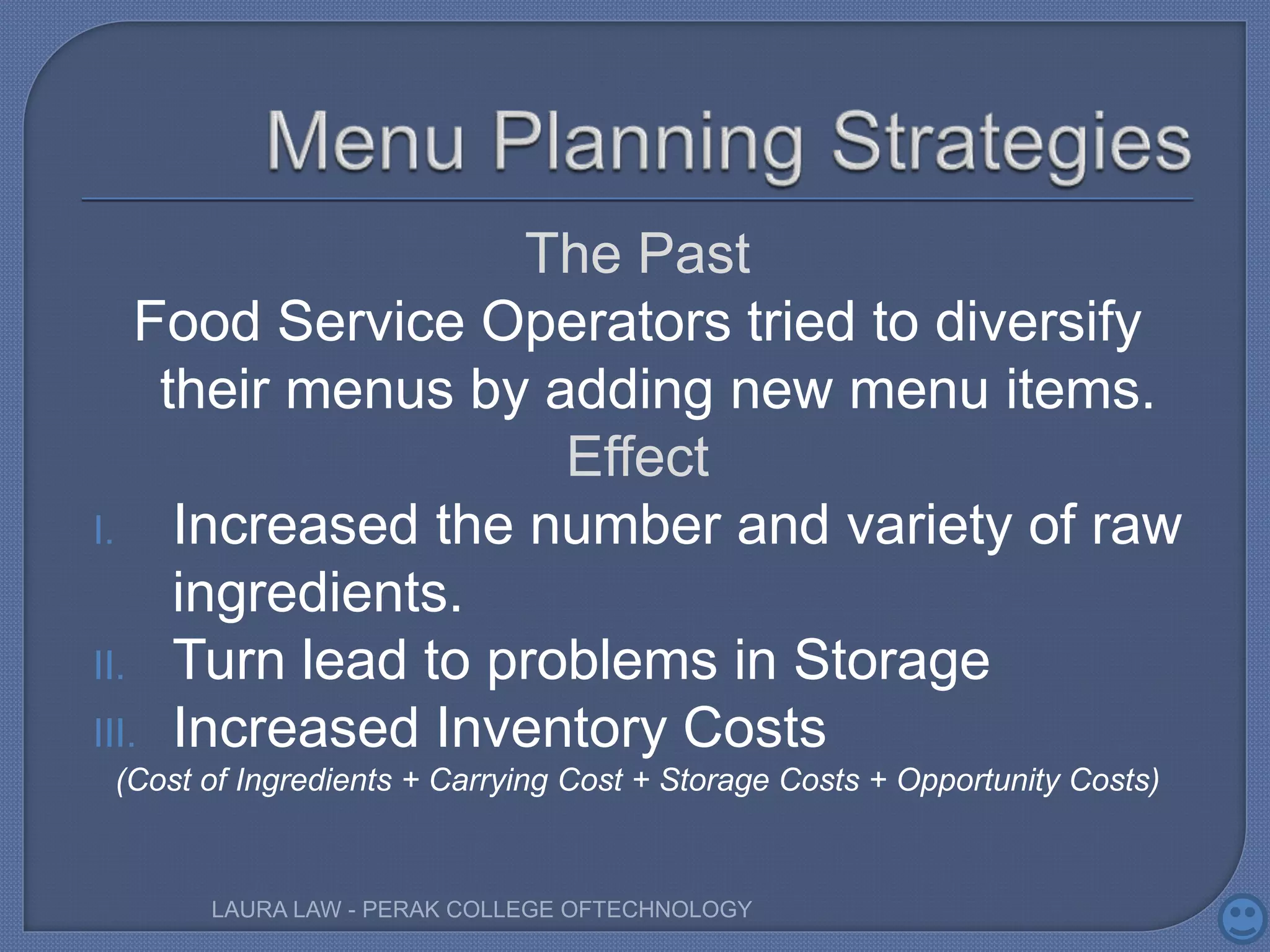

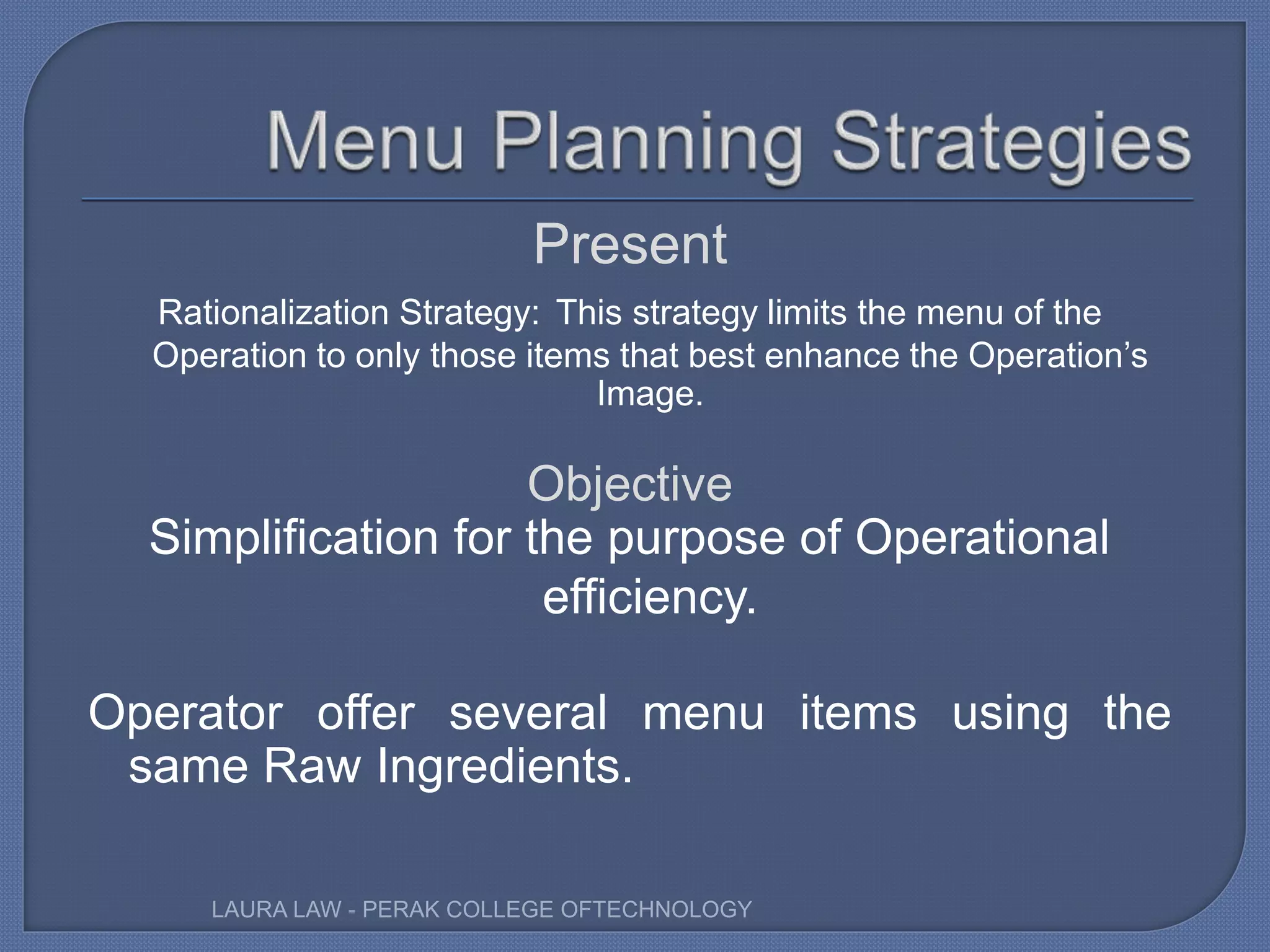

Past diversification of menus led to increased costs; current strategies focus on rationalization for efficiency.

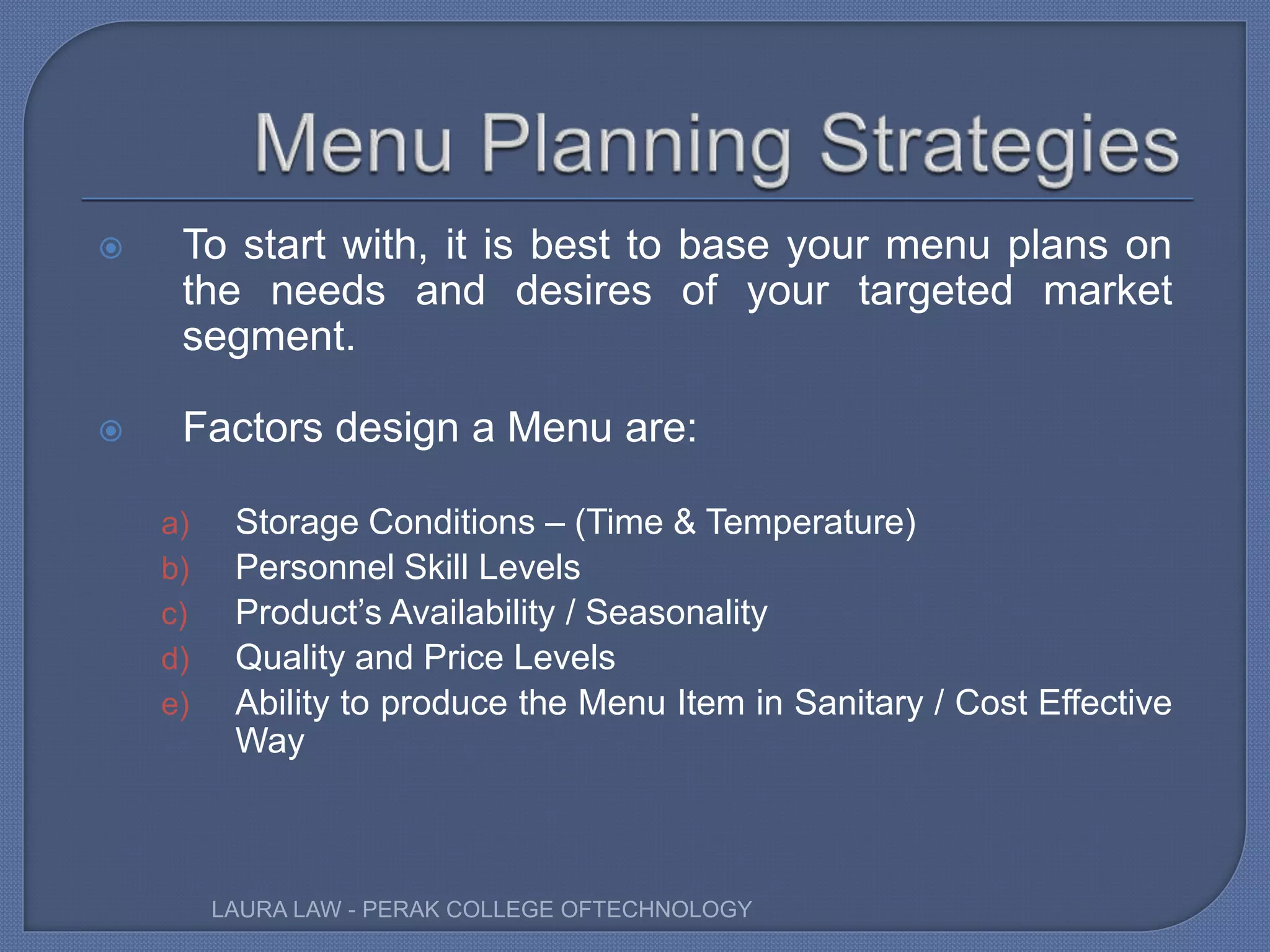

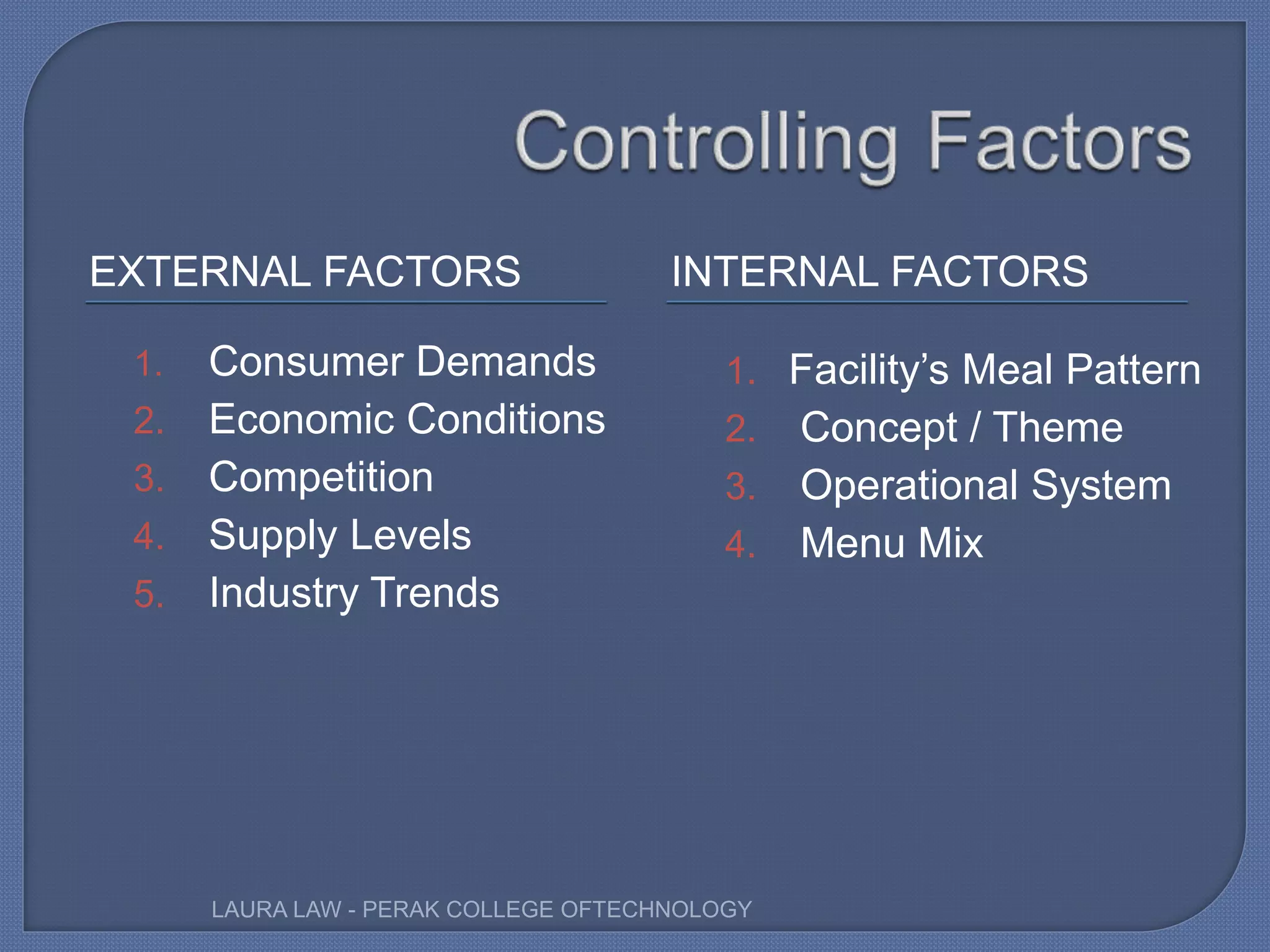

Discusses external and internal factors that impact menu design to meet market needs.

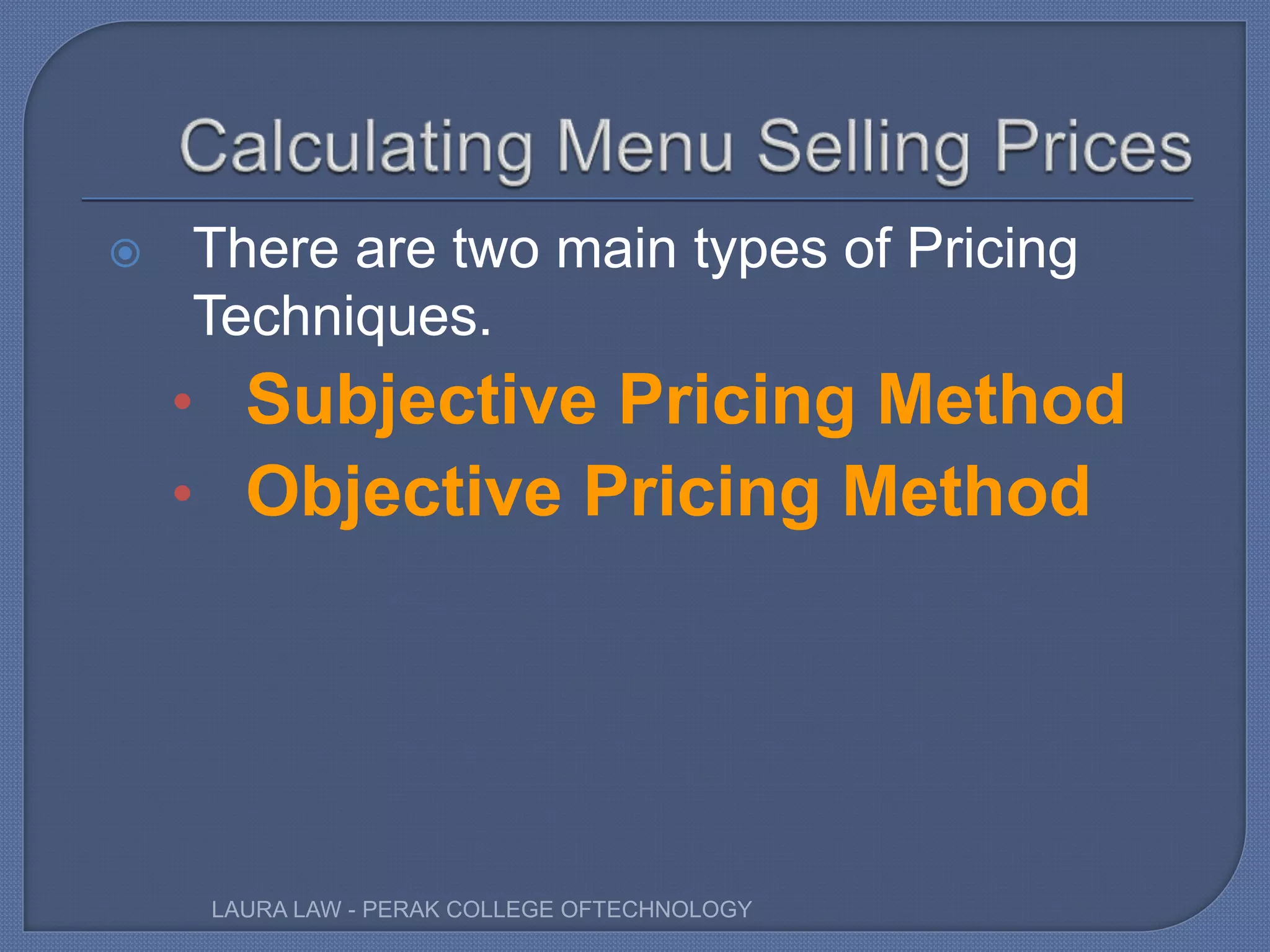

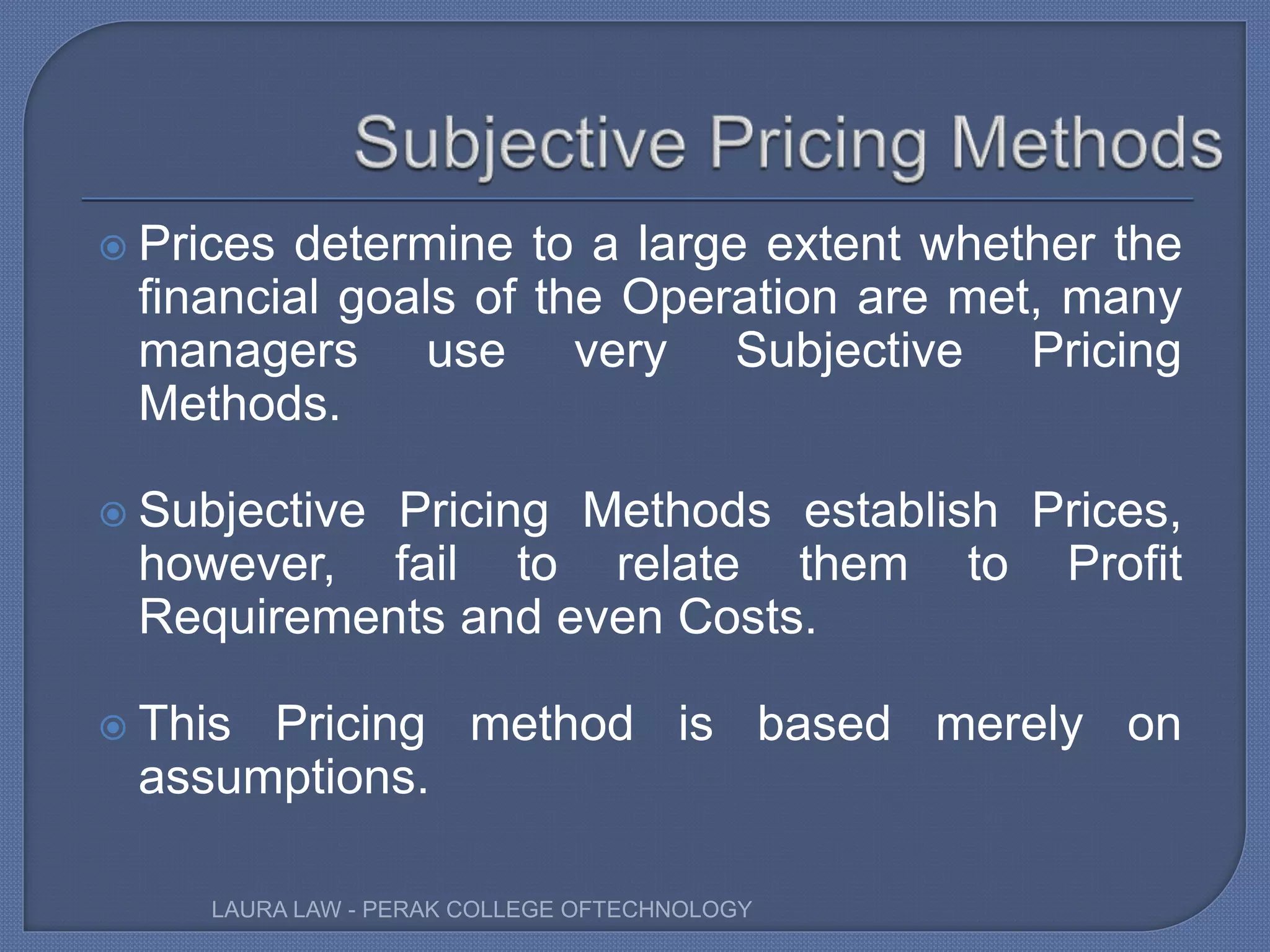

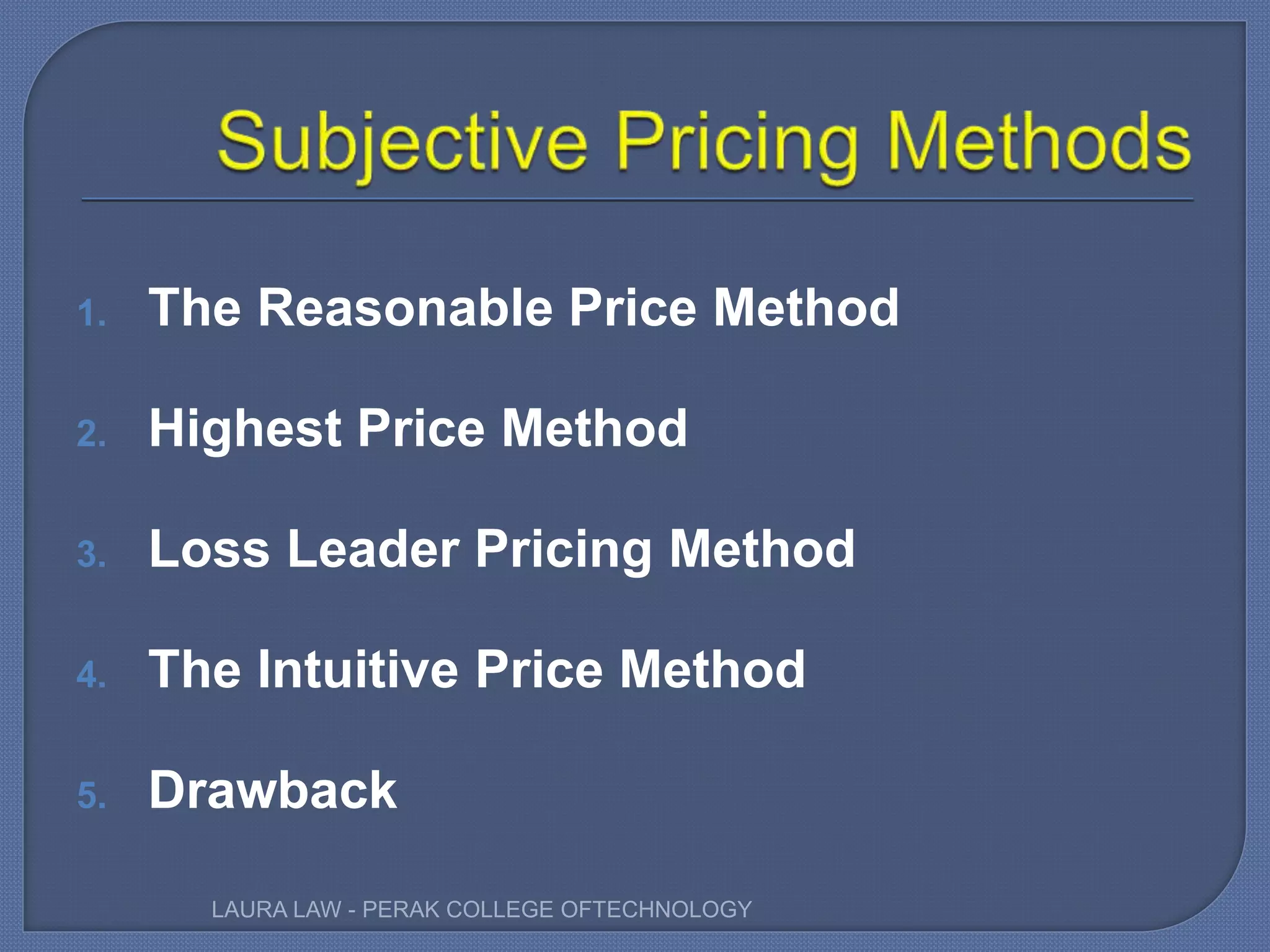

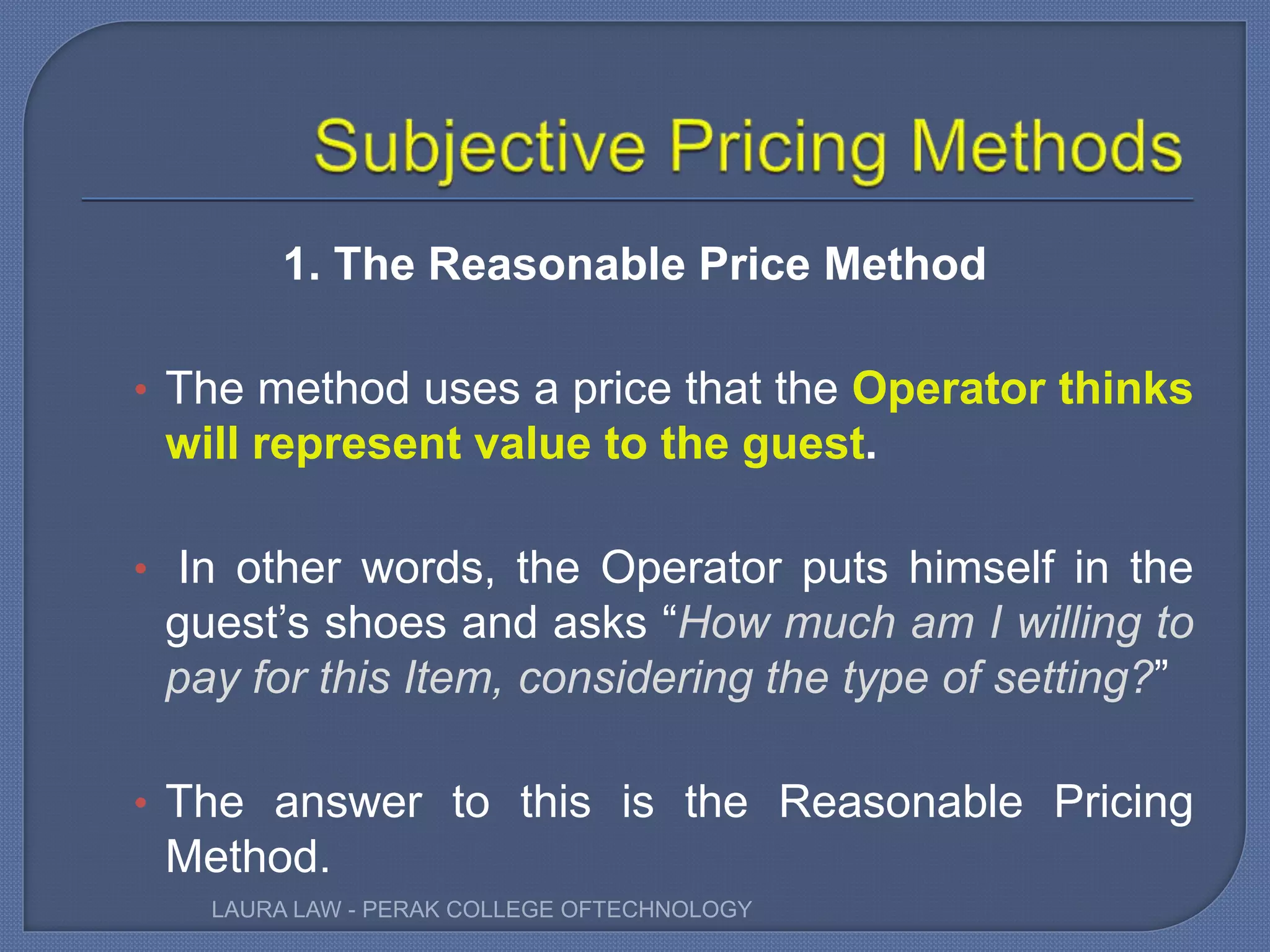

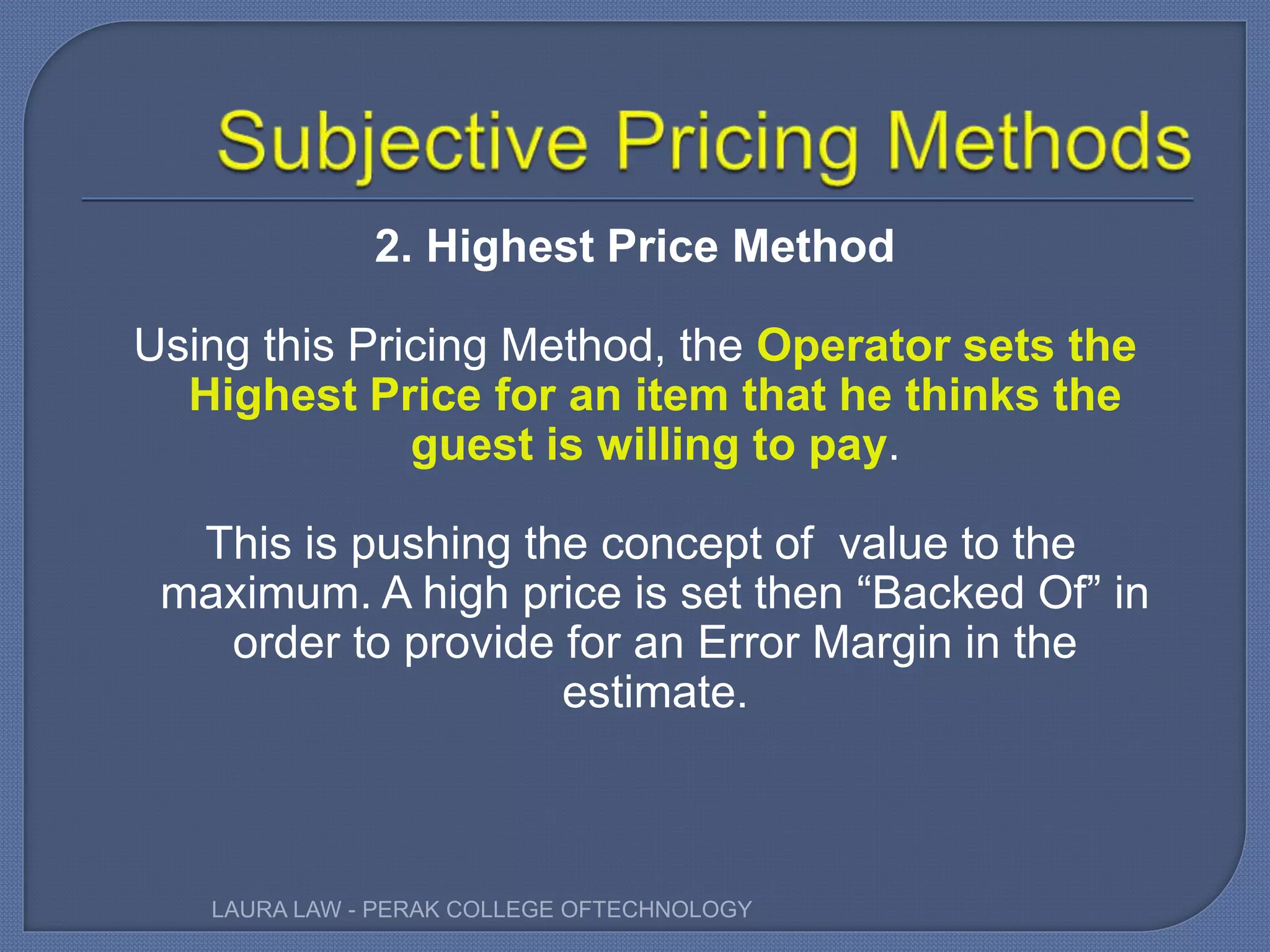

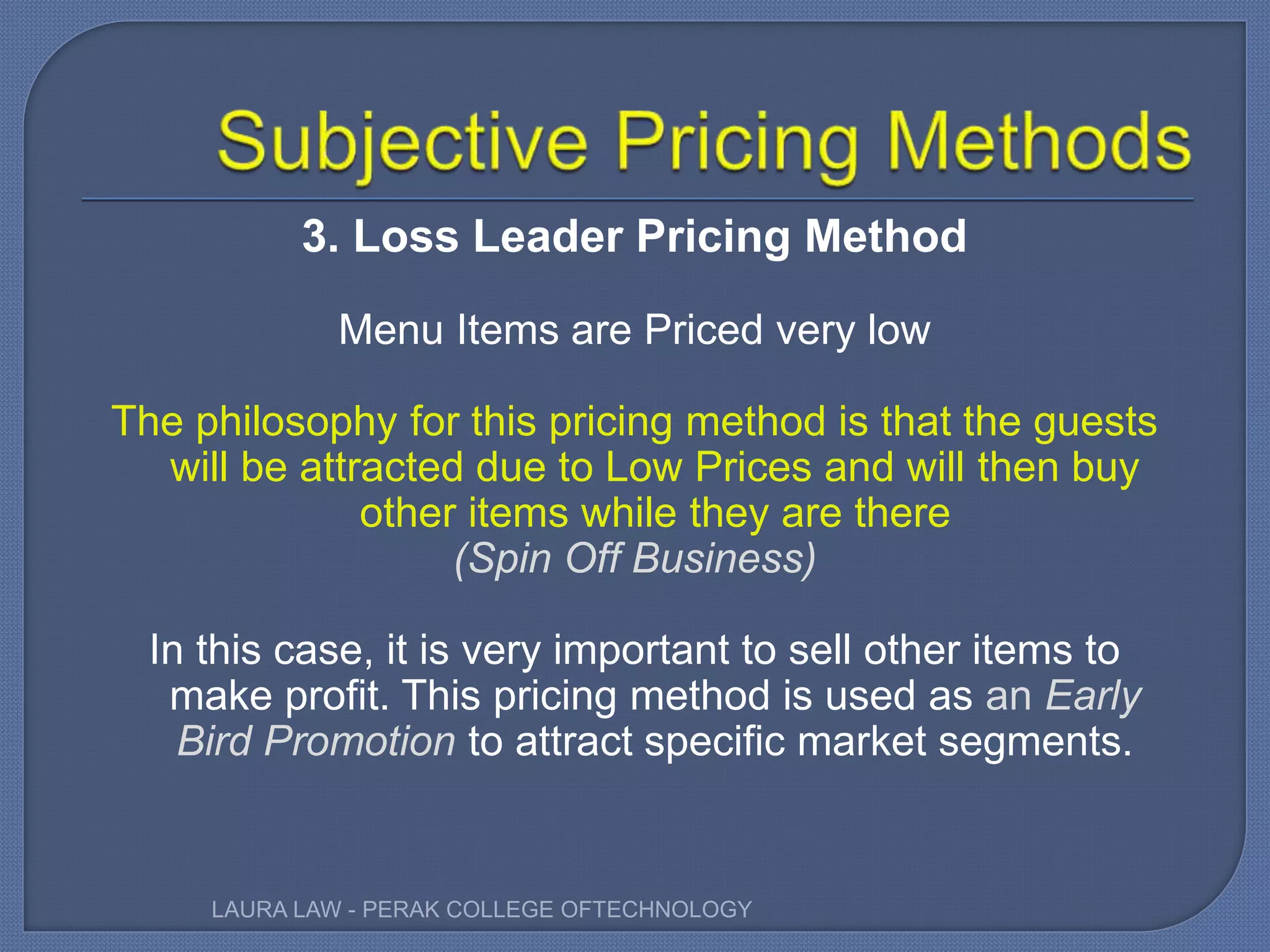

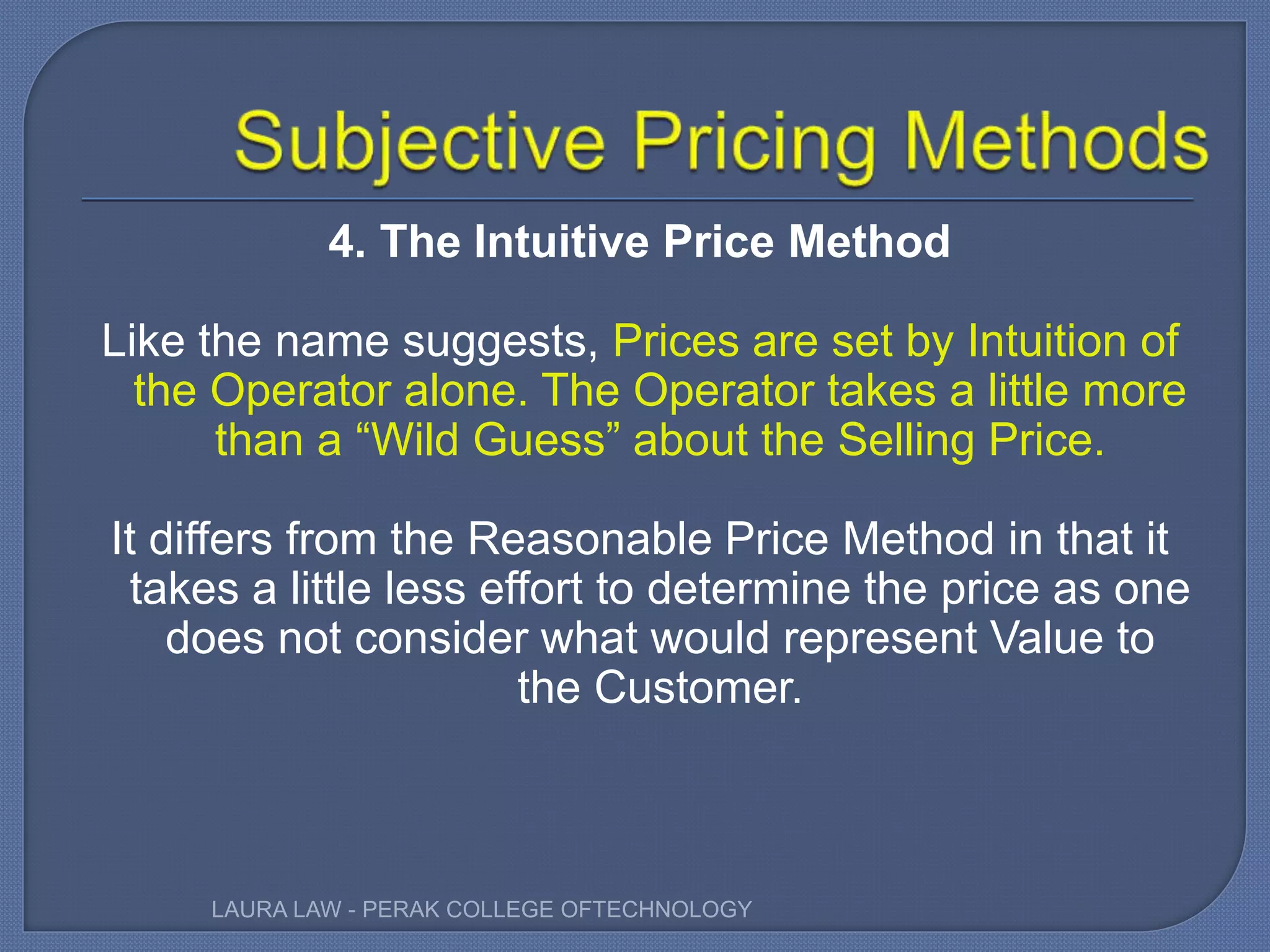

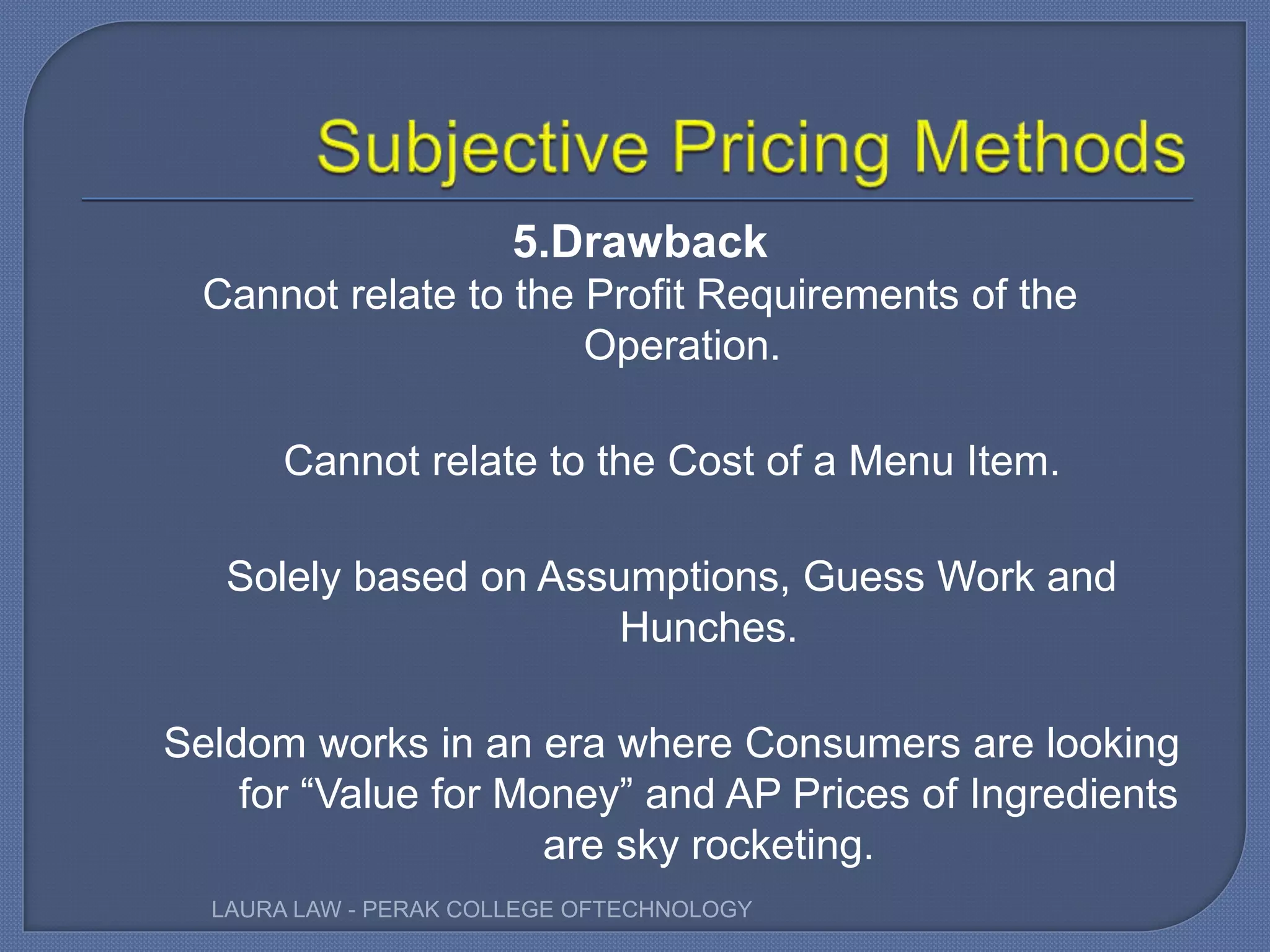

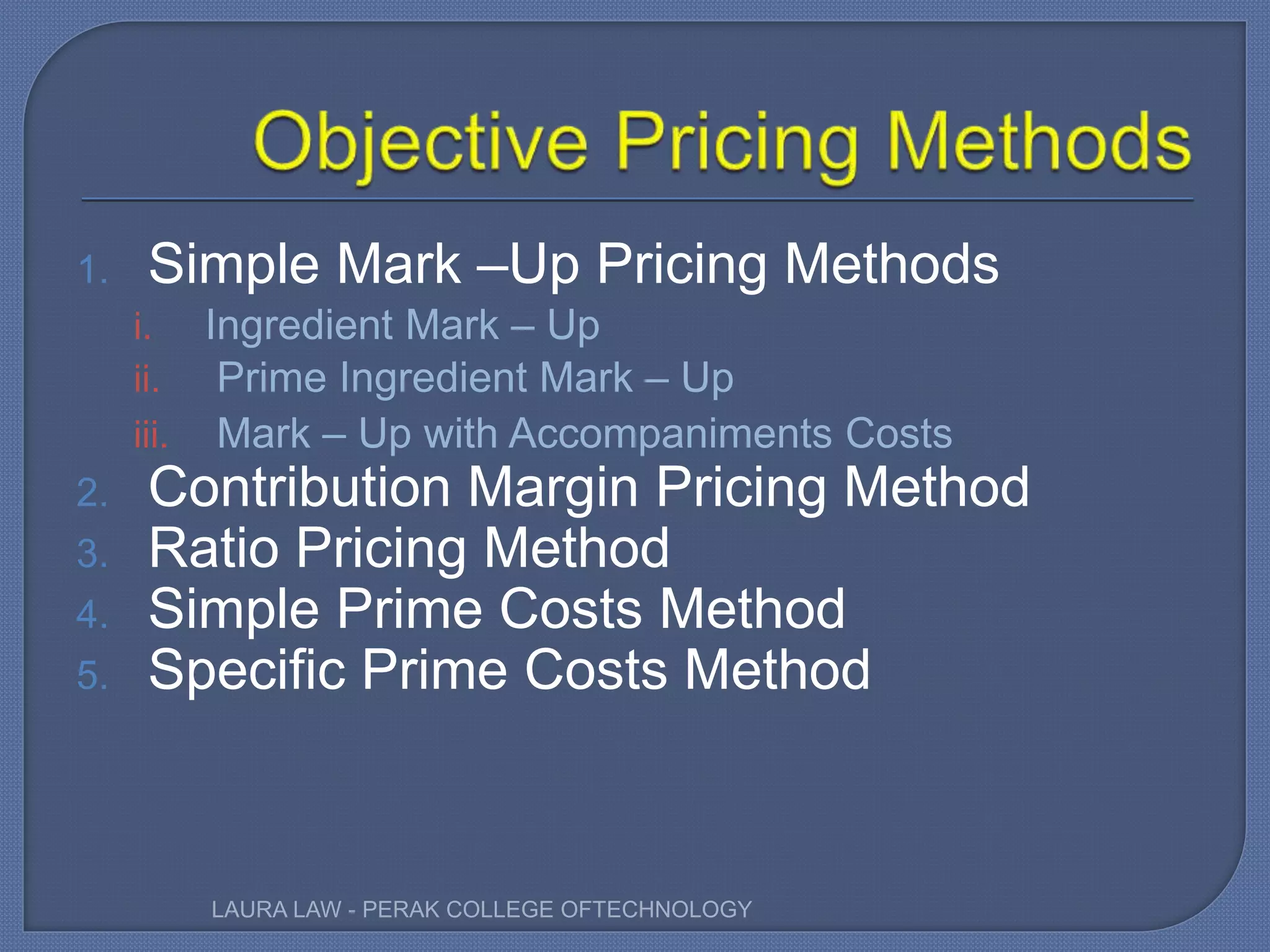

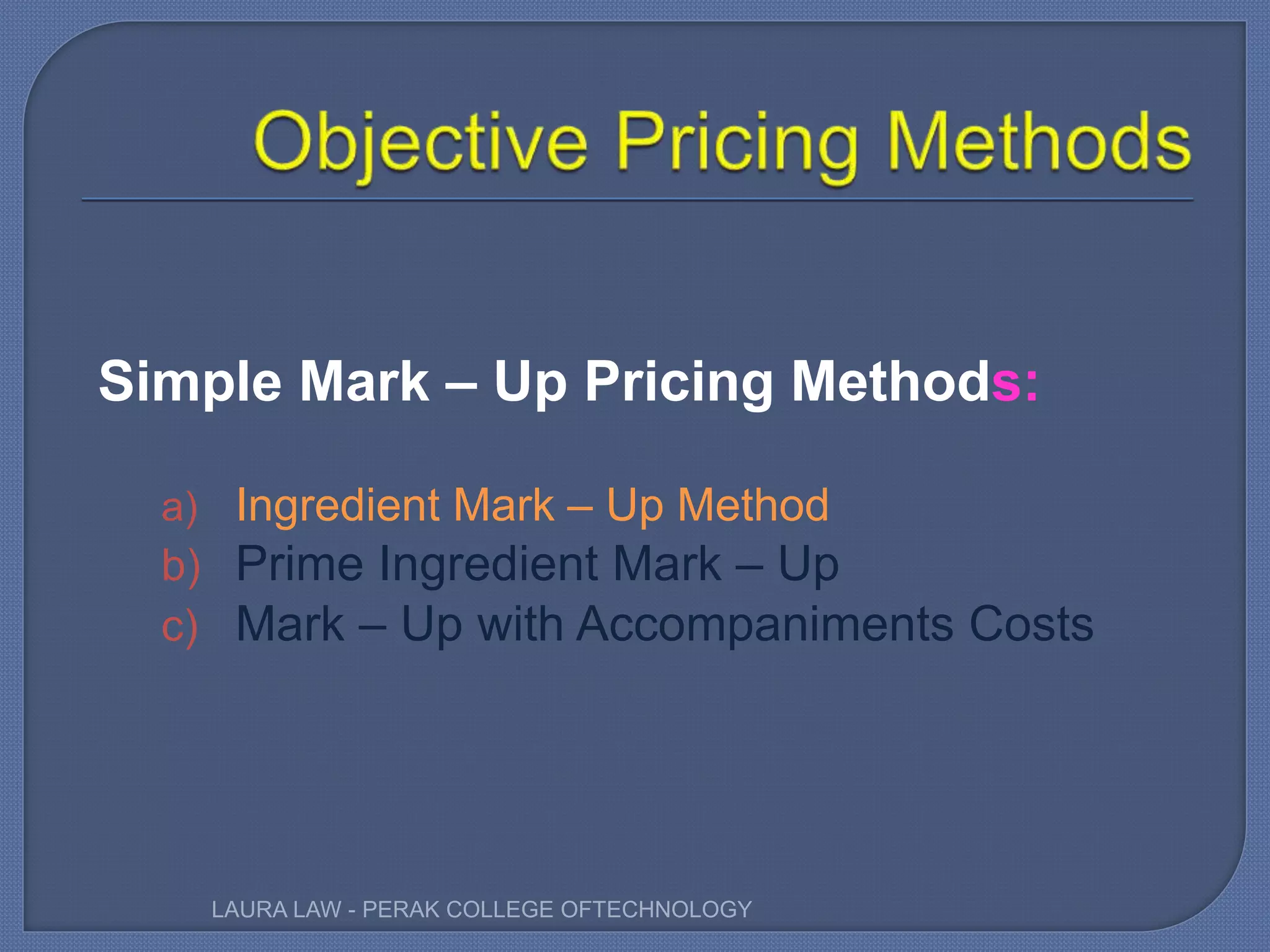

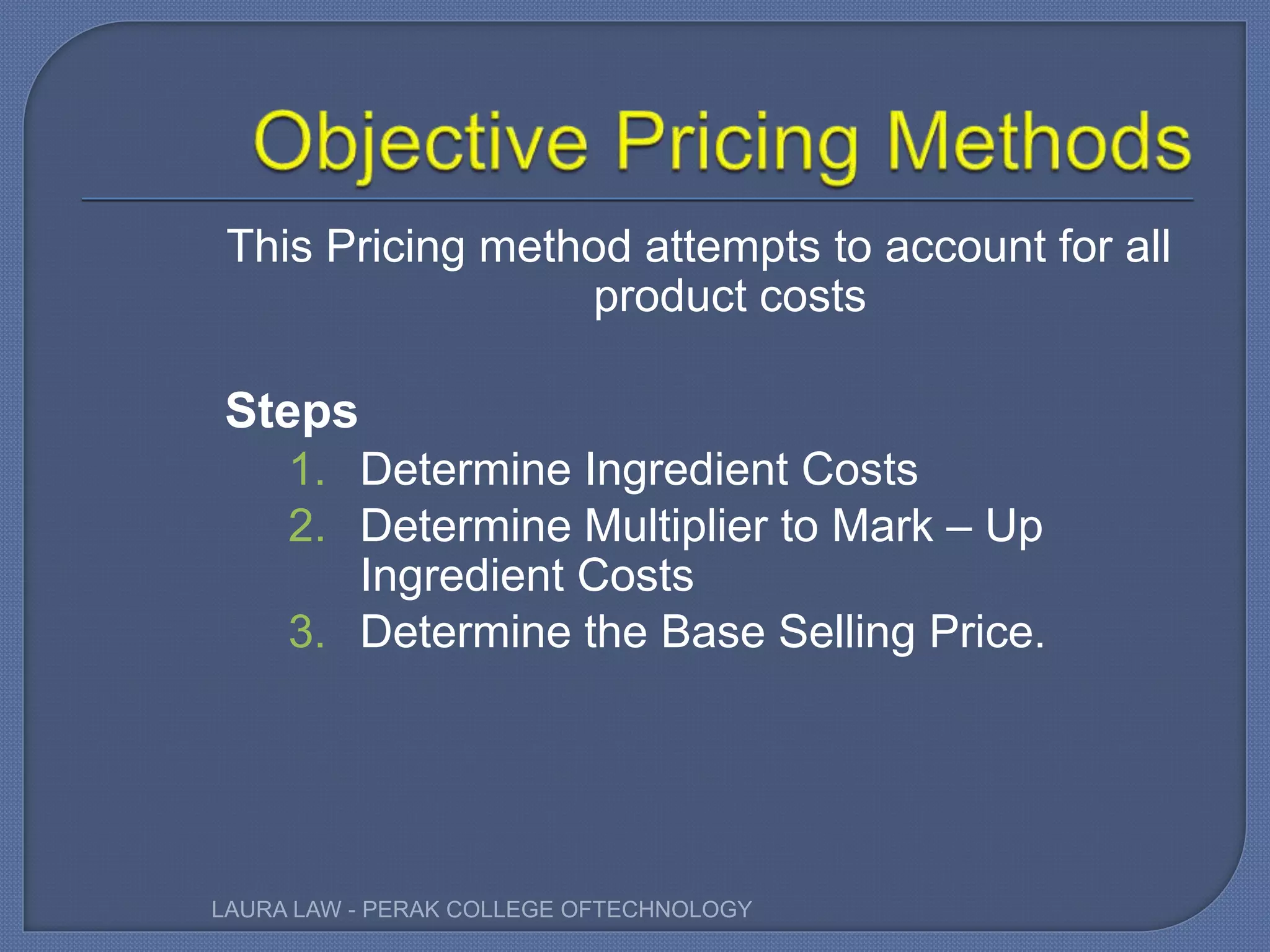

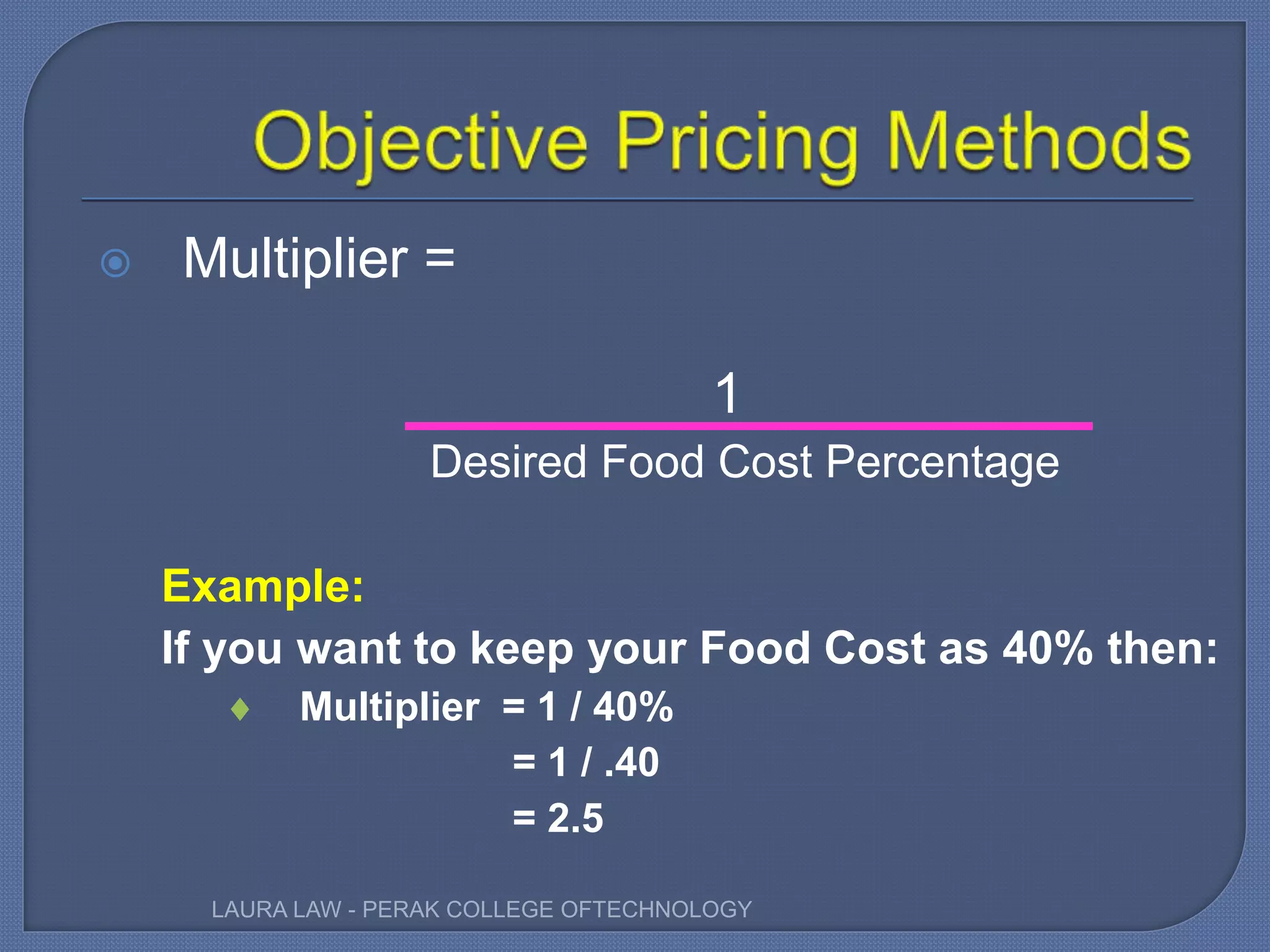

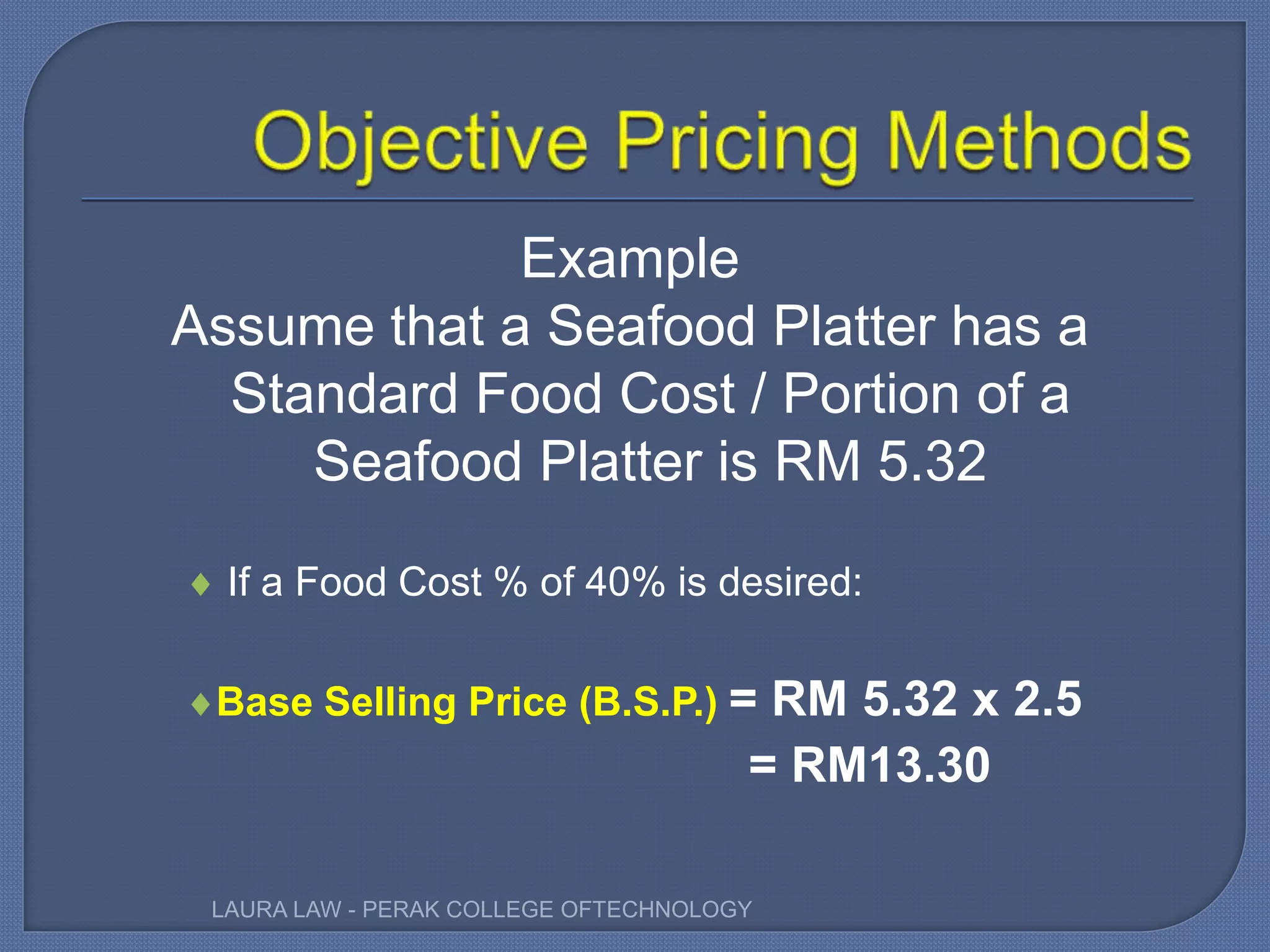

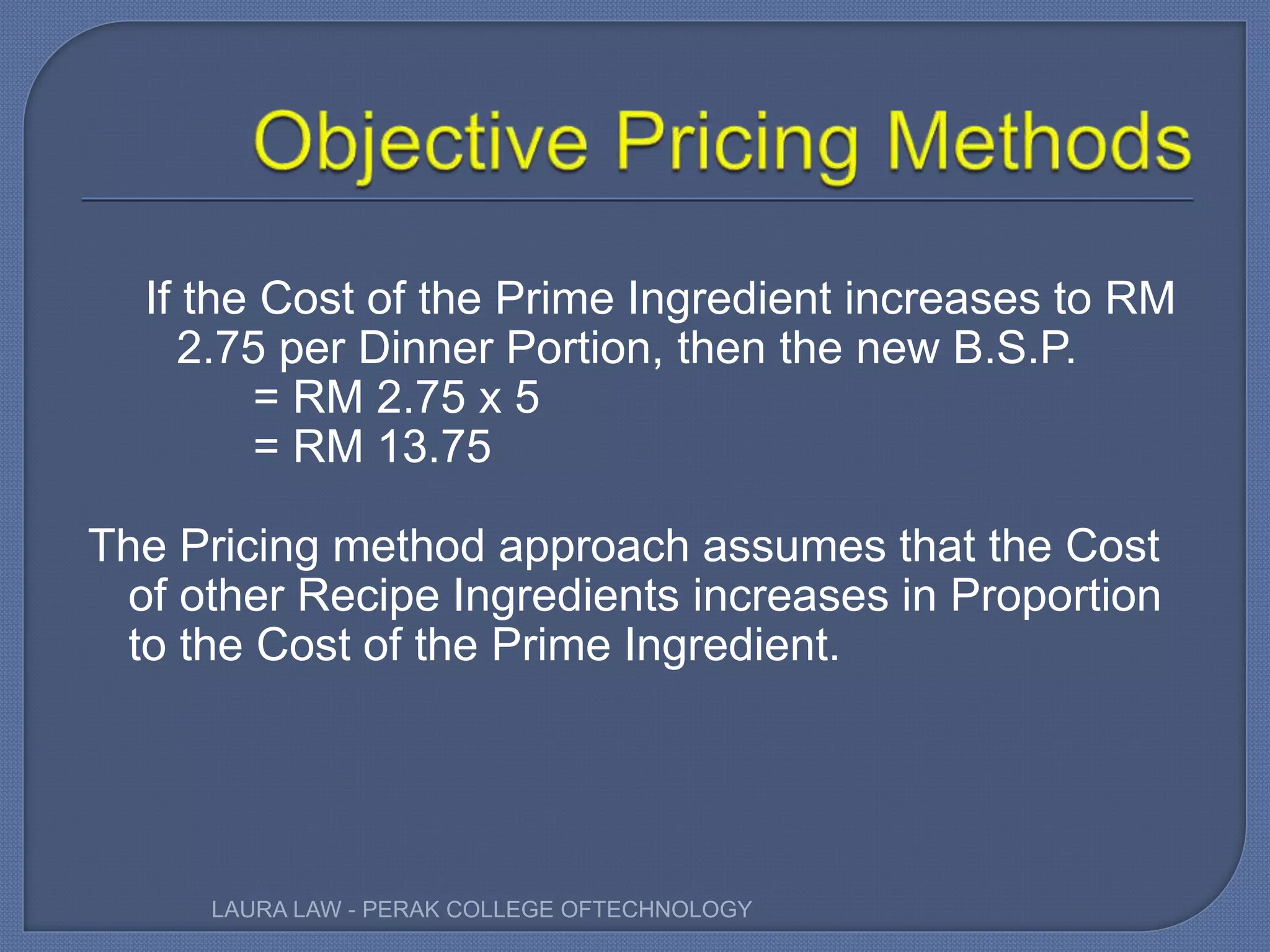

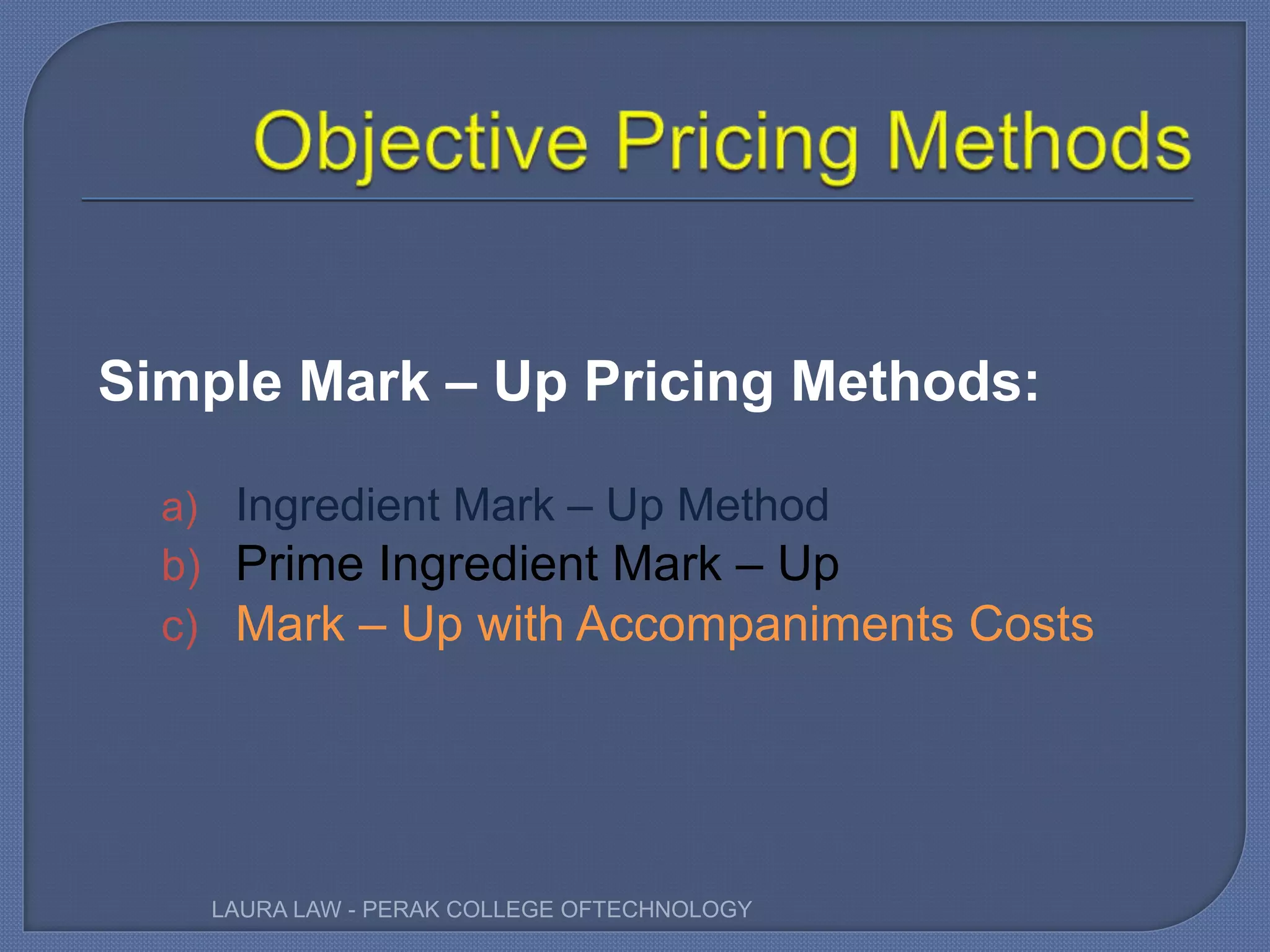

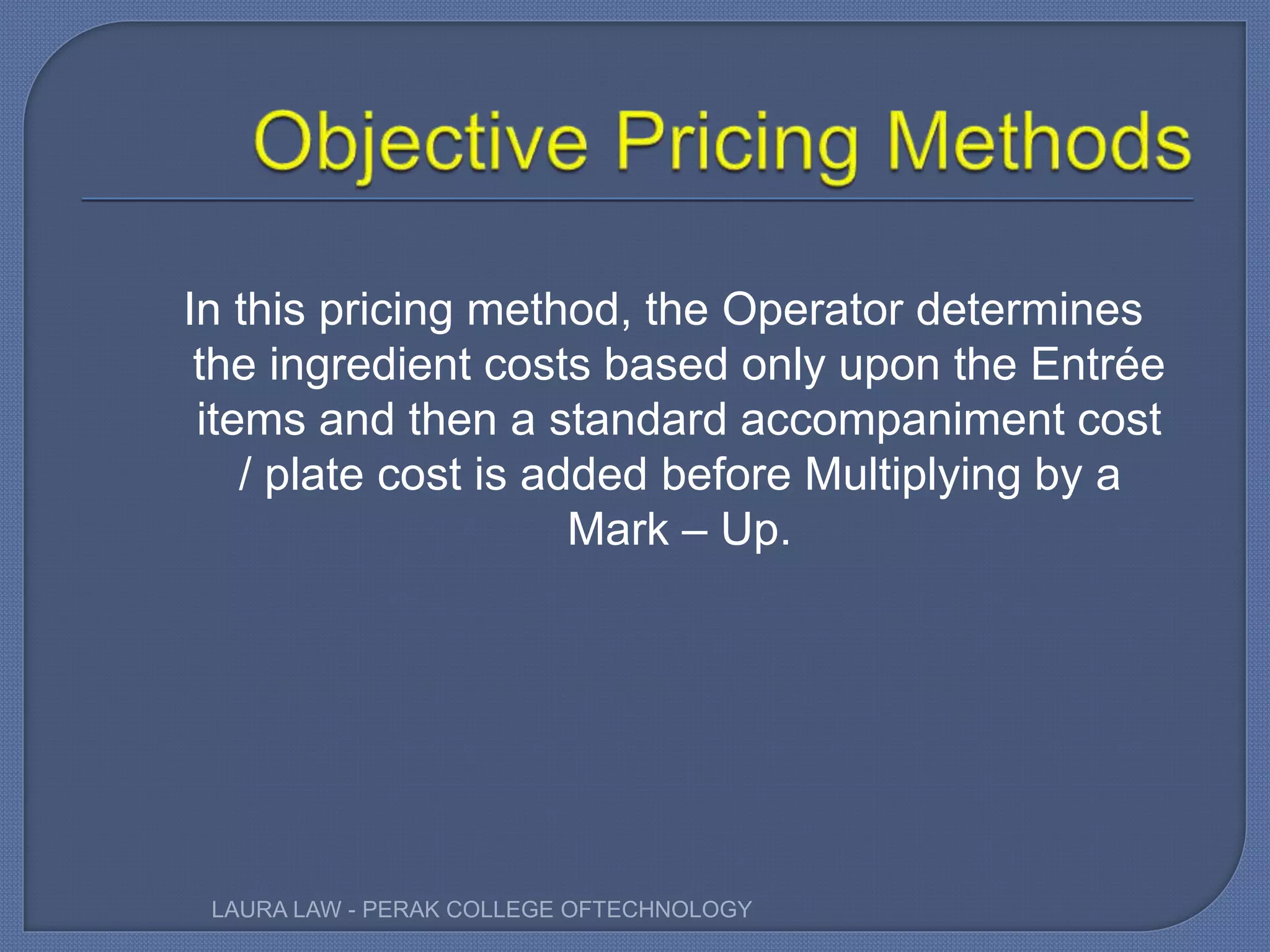

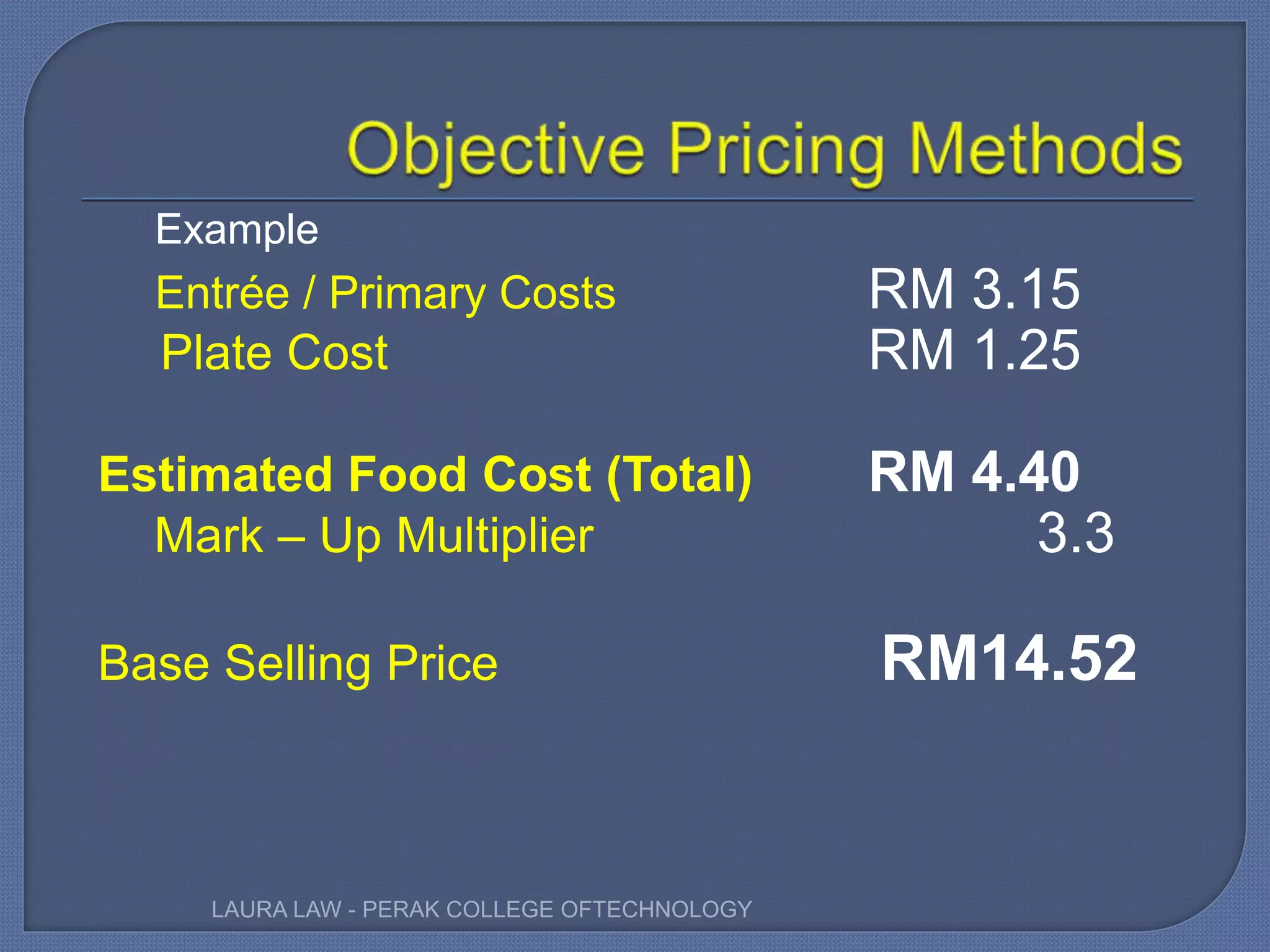

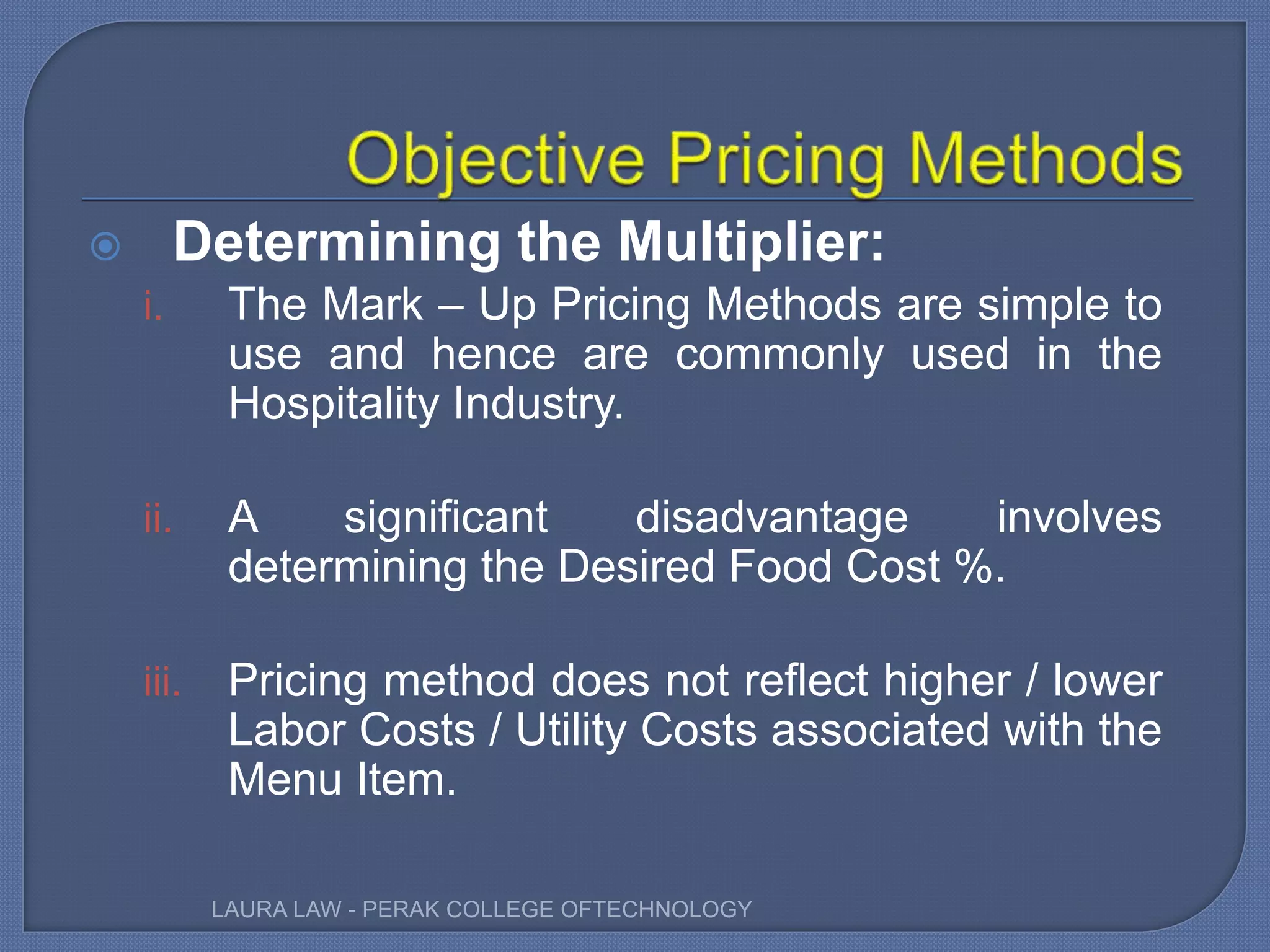

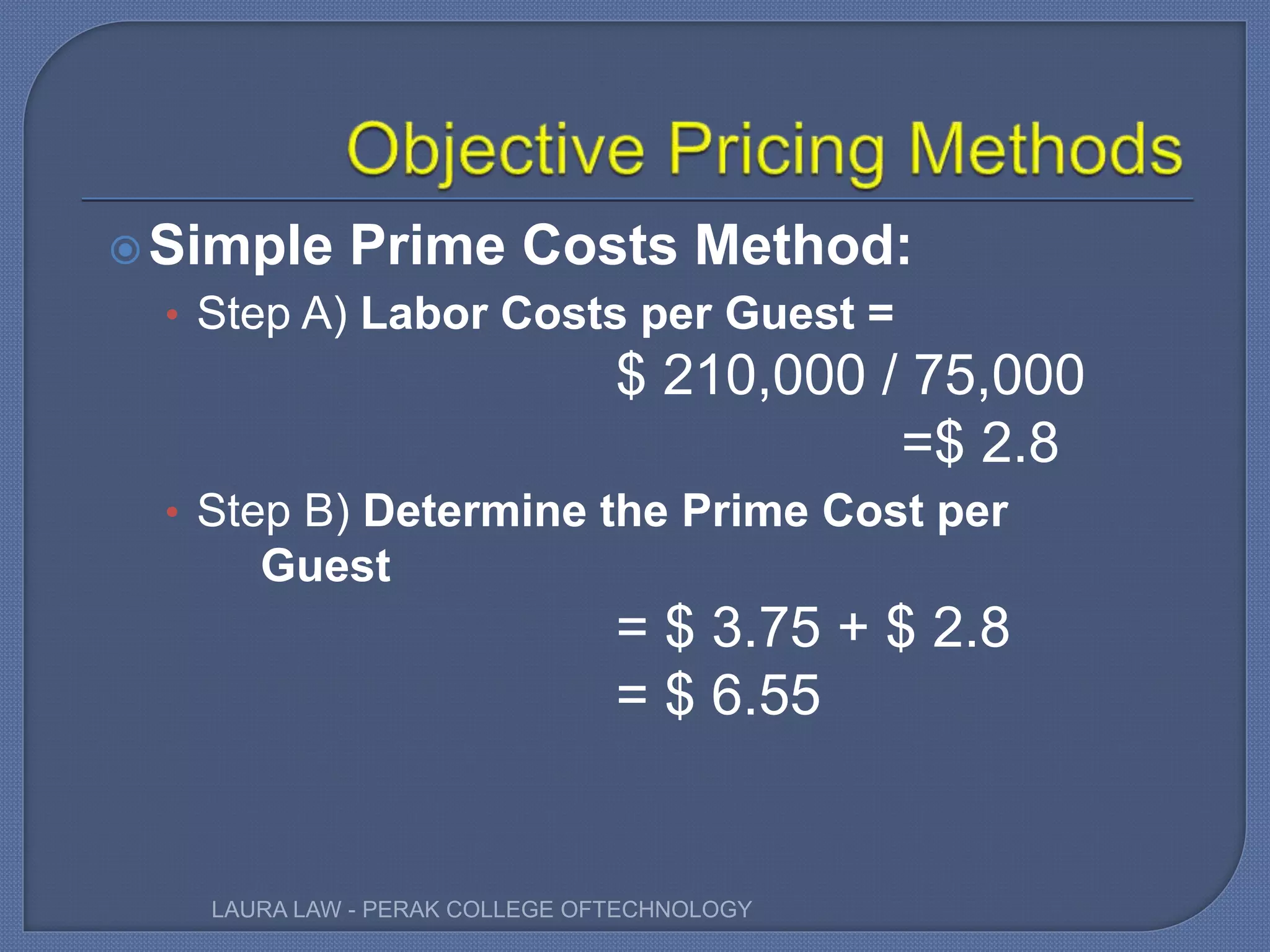

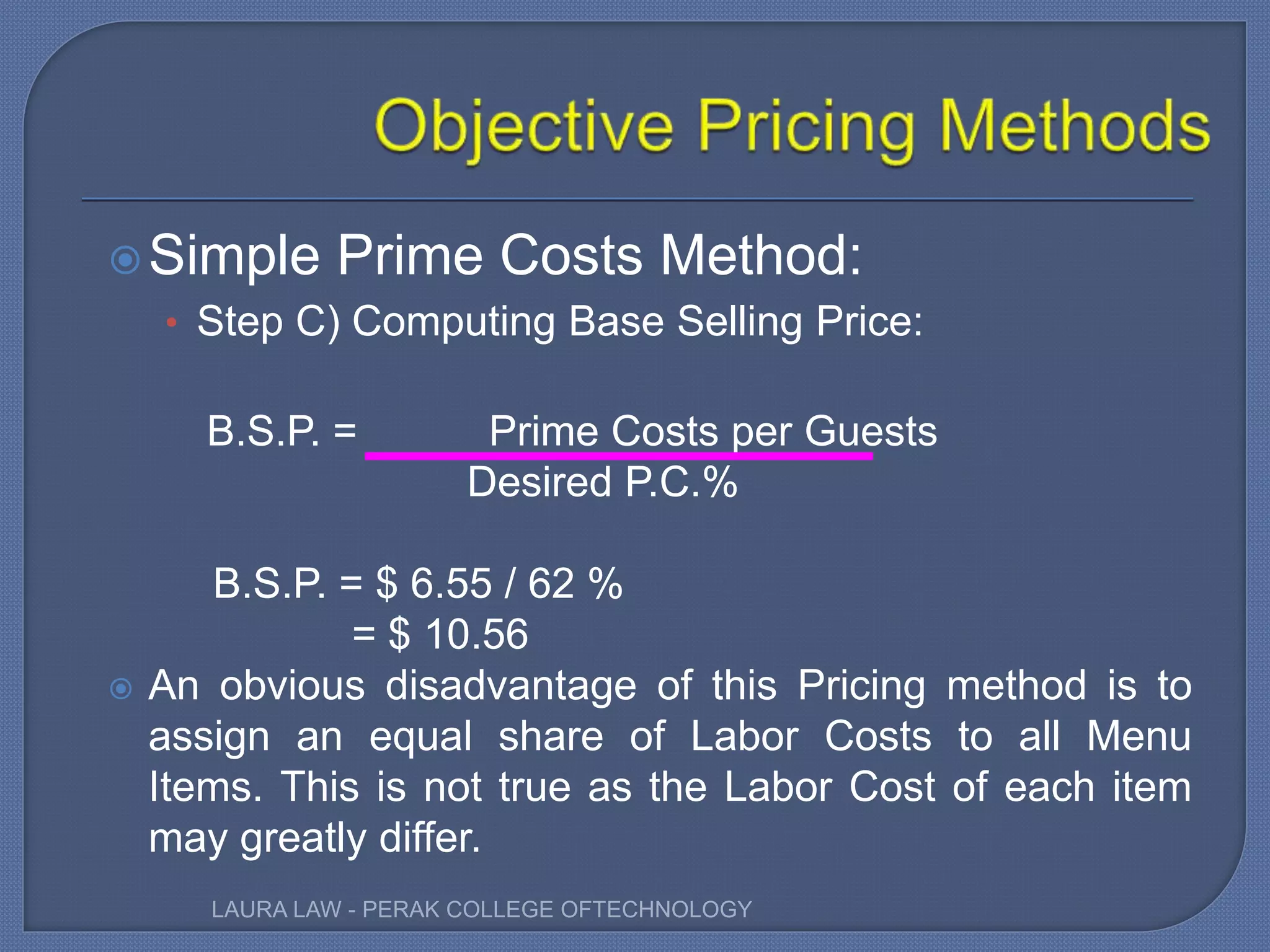

Explains pricing strategies in menu planning, including subjective and objective pricing methods.

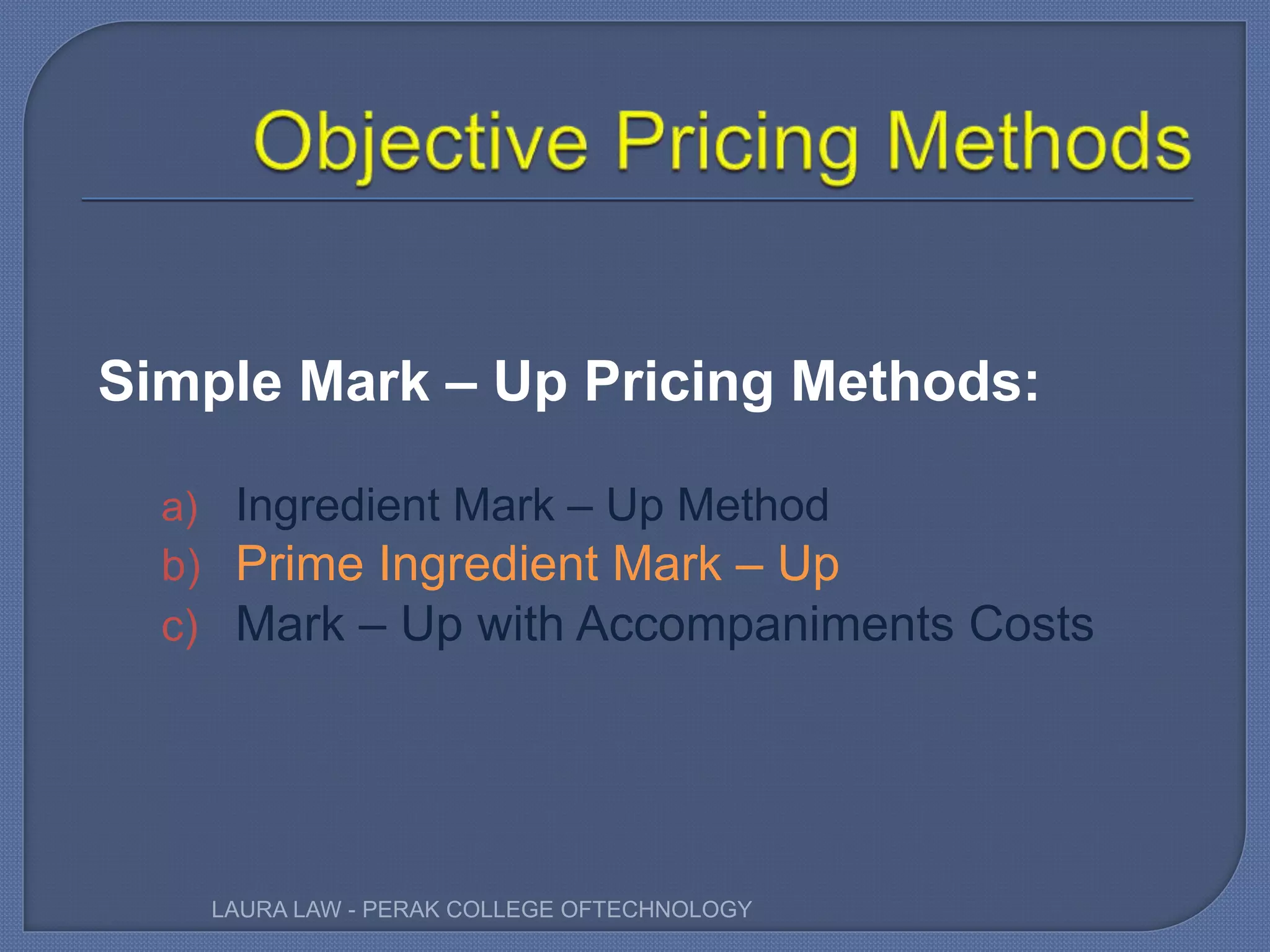

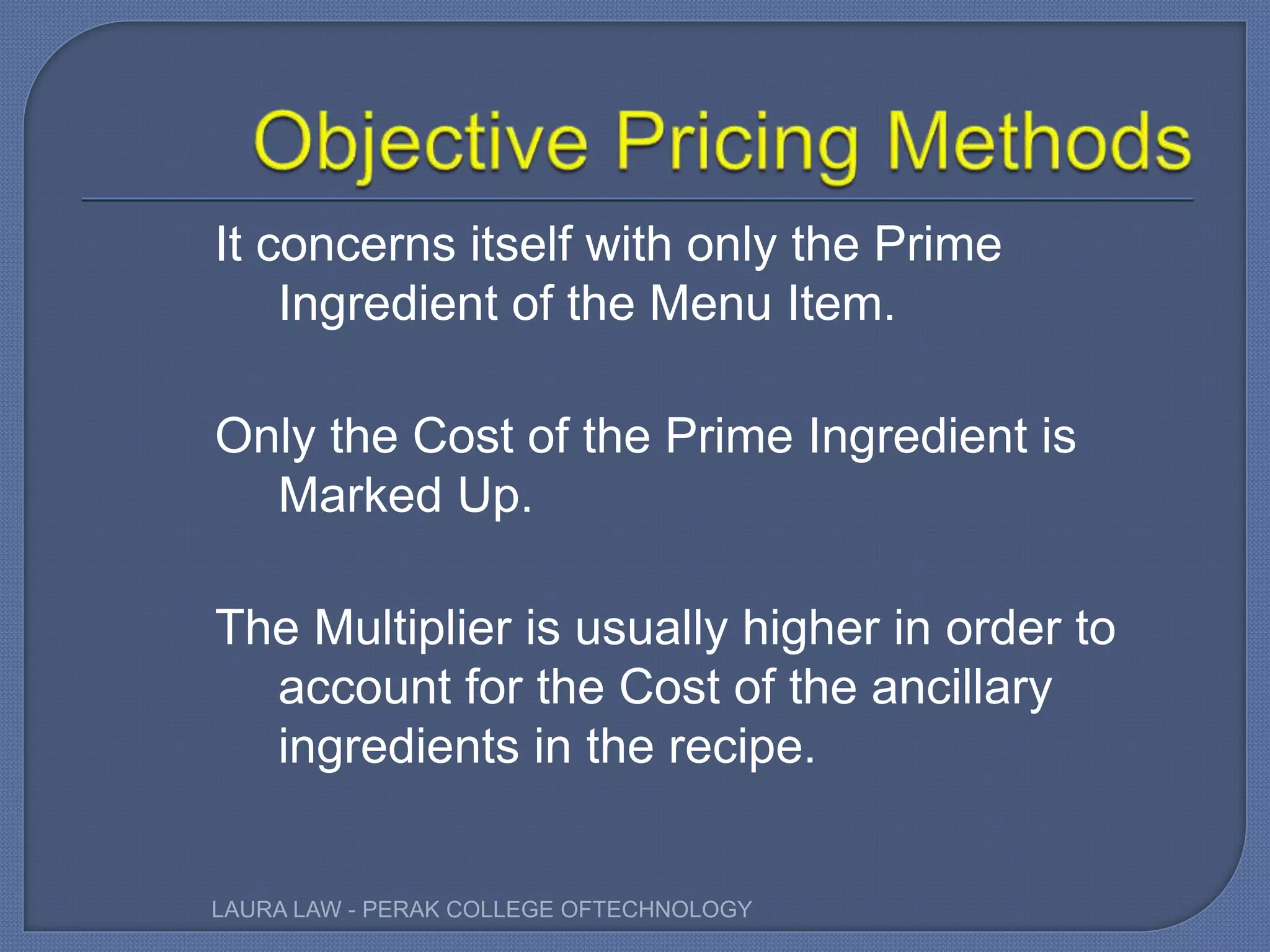

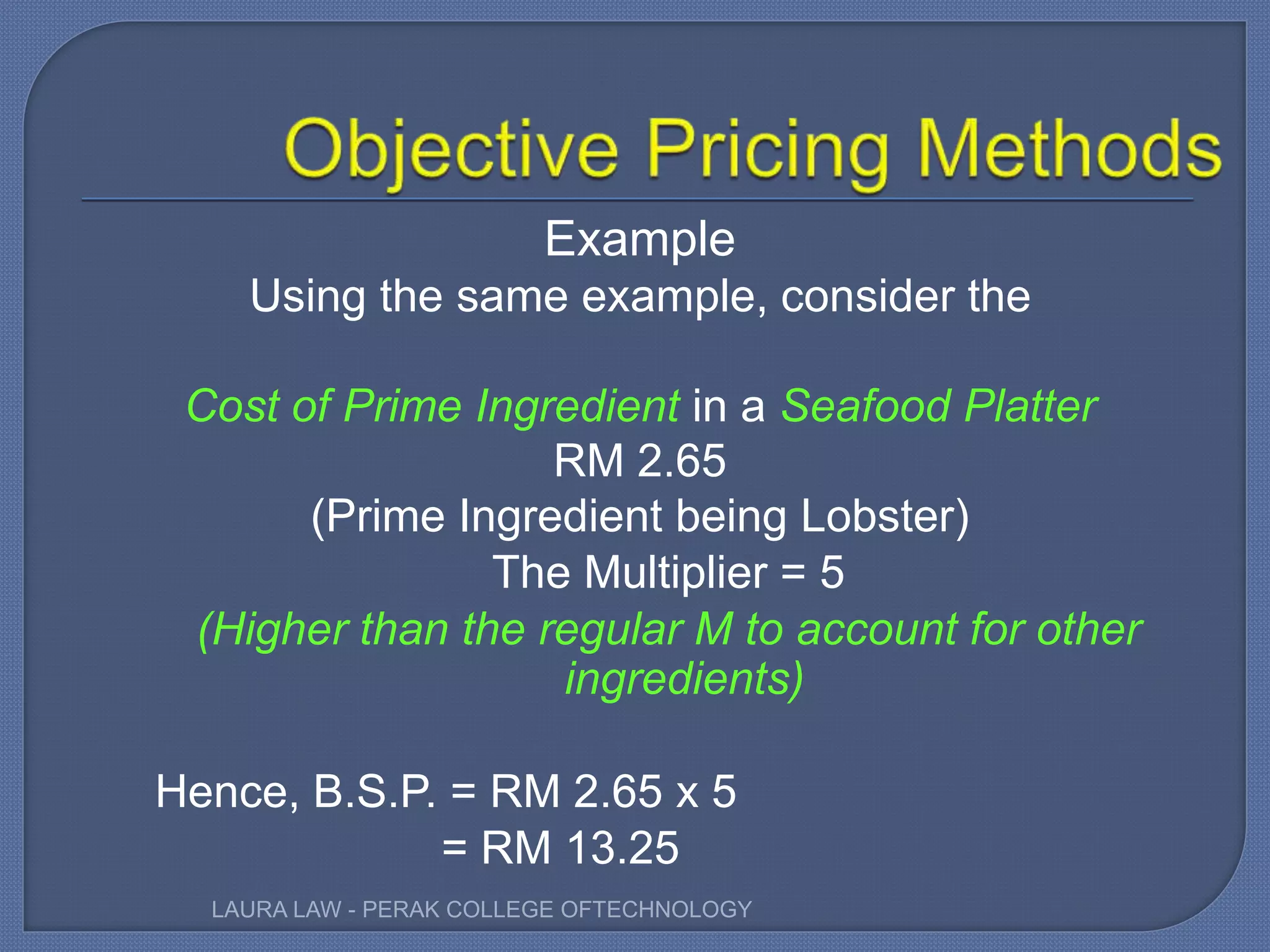

Details various simple mark-up pricing methods used to determine base selling prices for menu items.

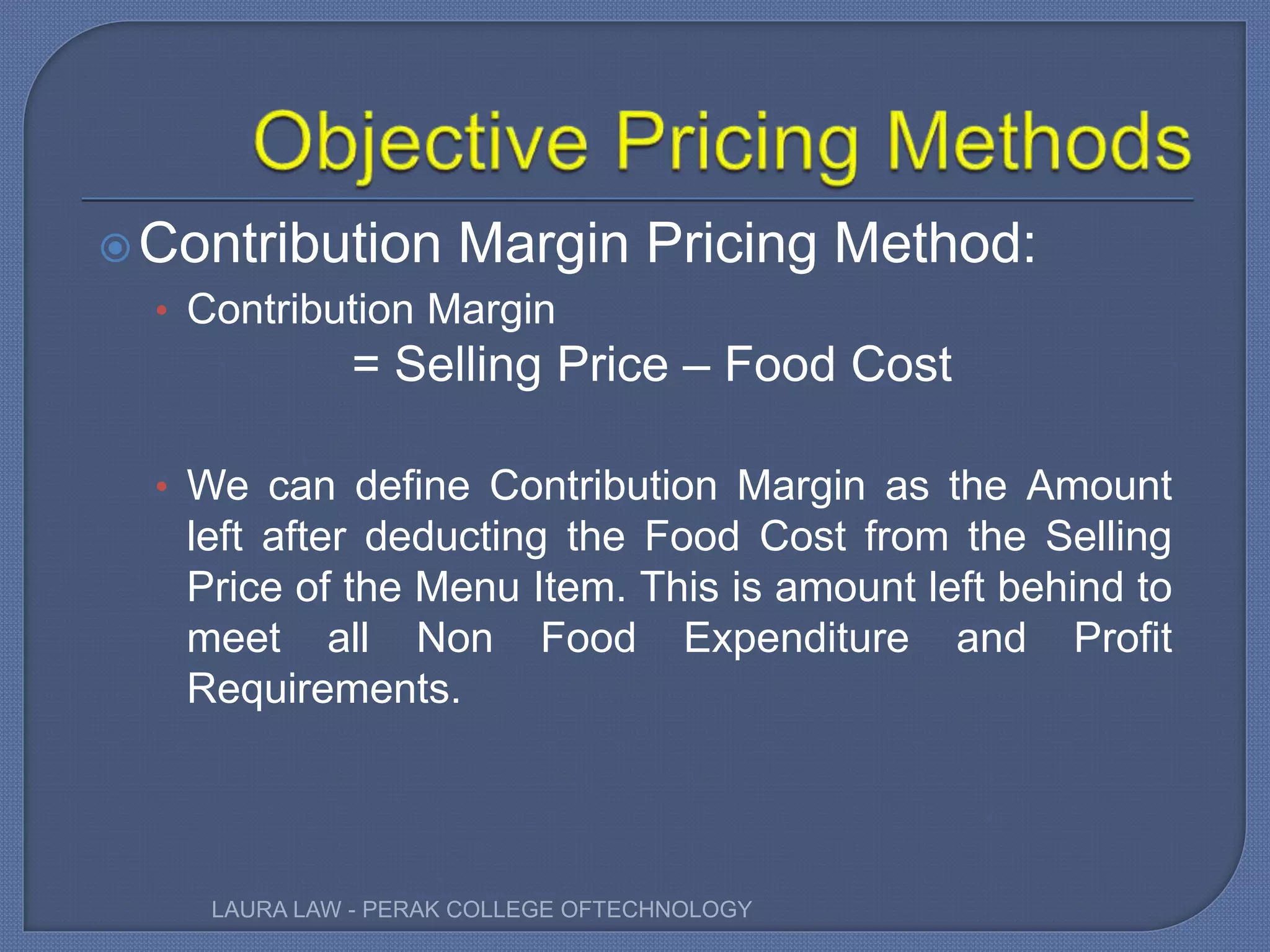

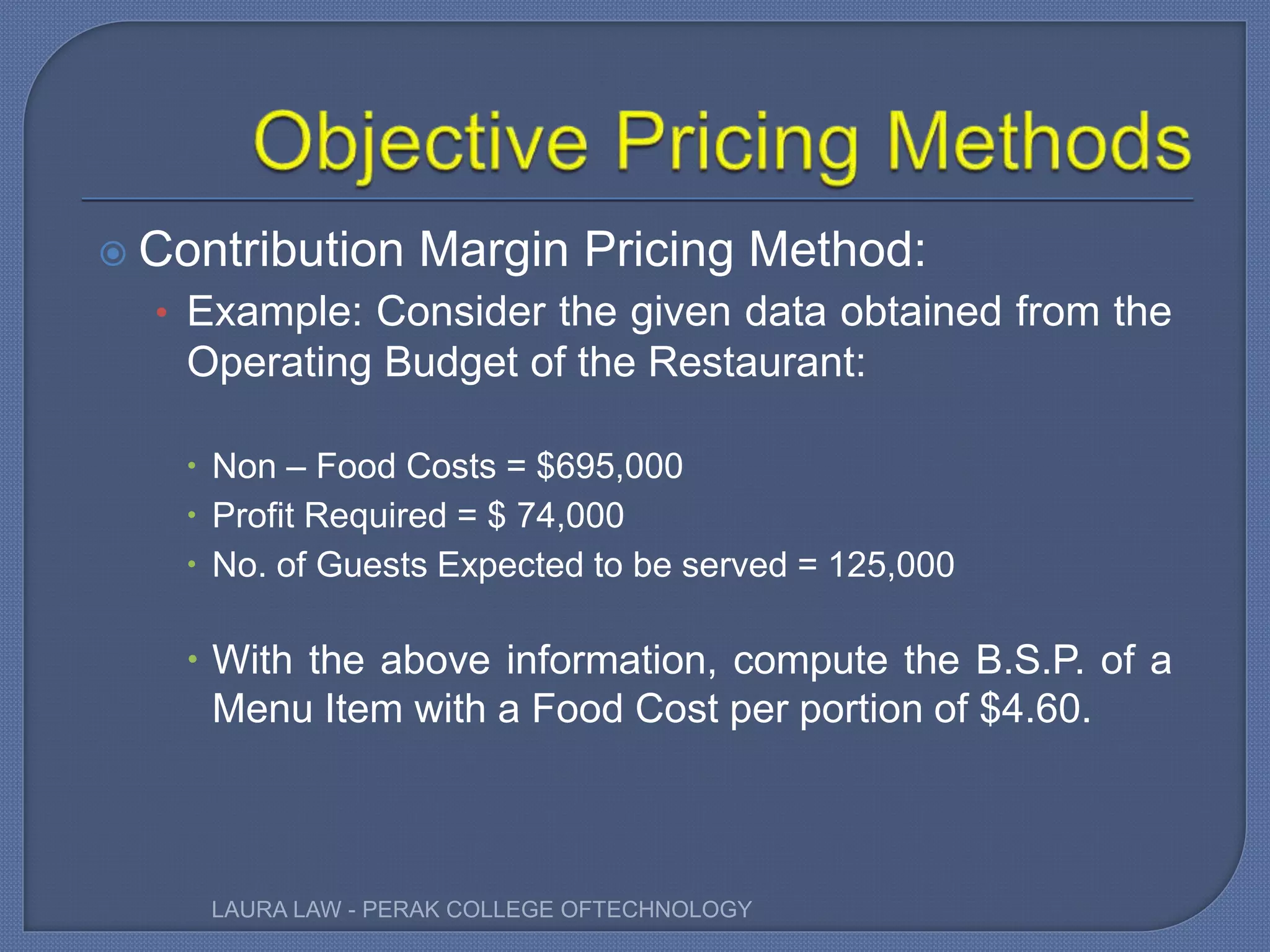

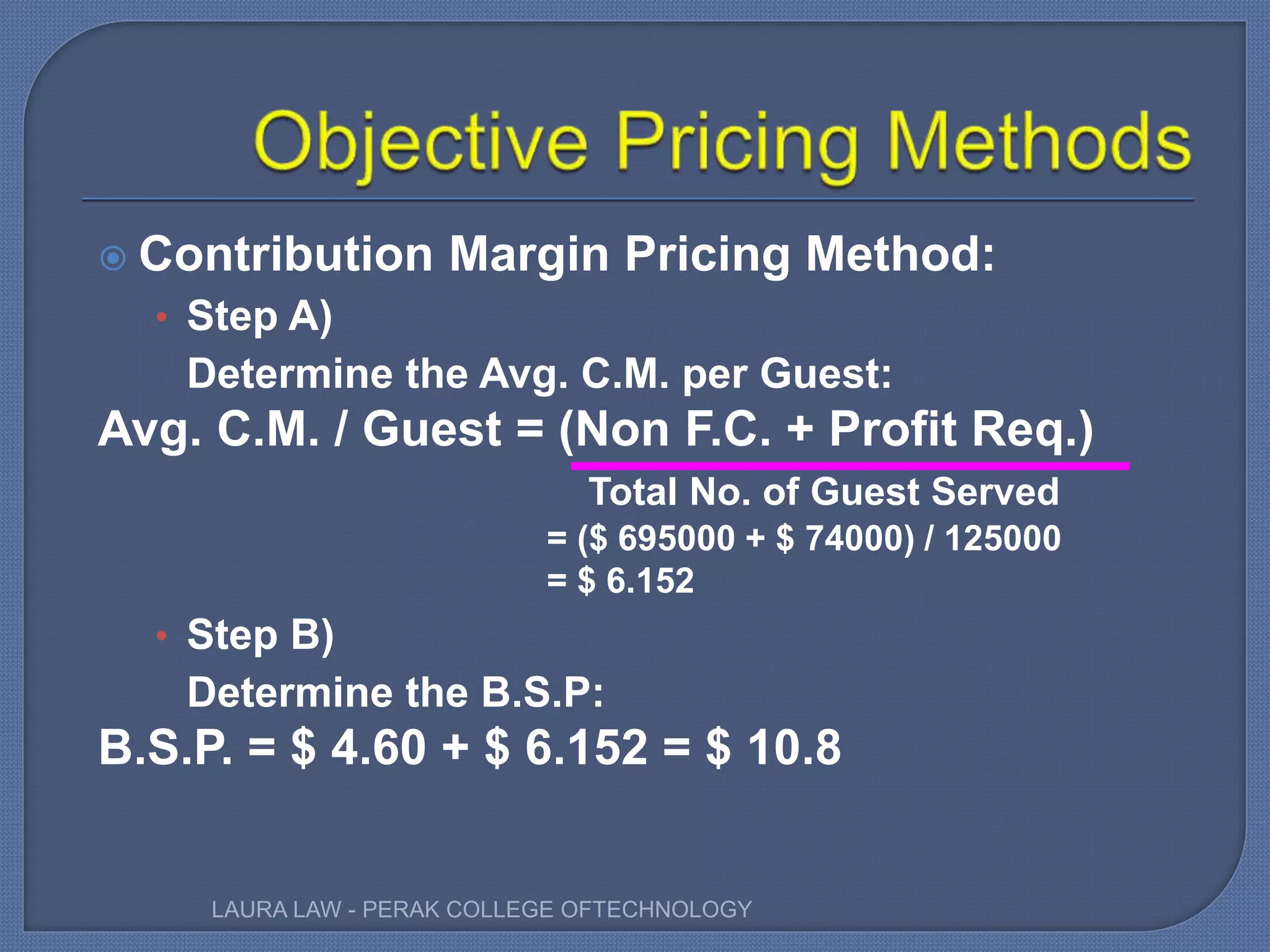

Describes the contribution margin pricing method for calculating base selling prices based on costs.

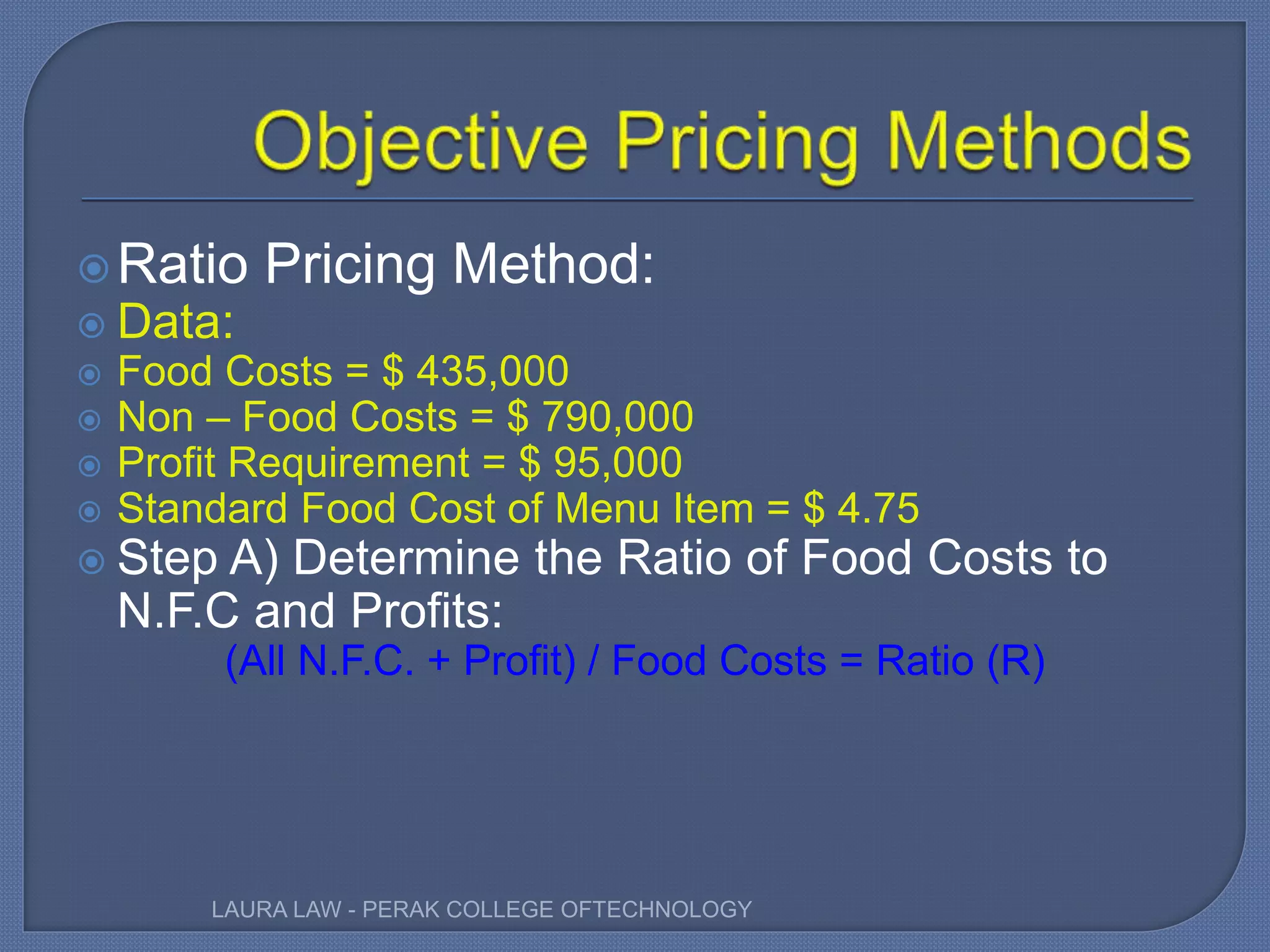

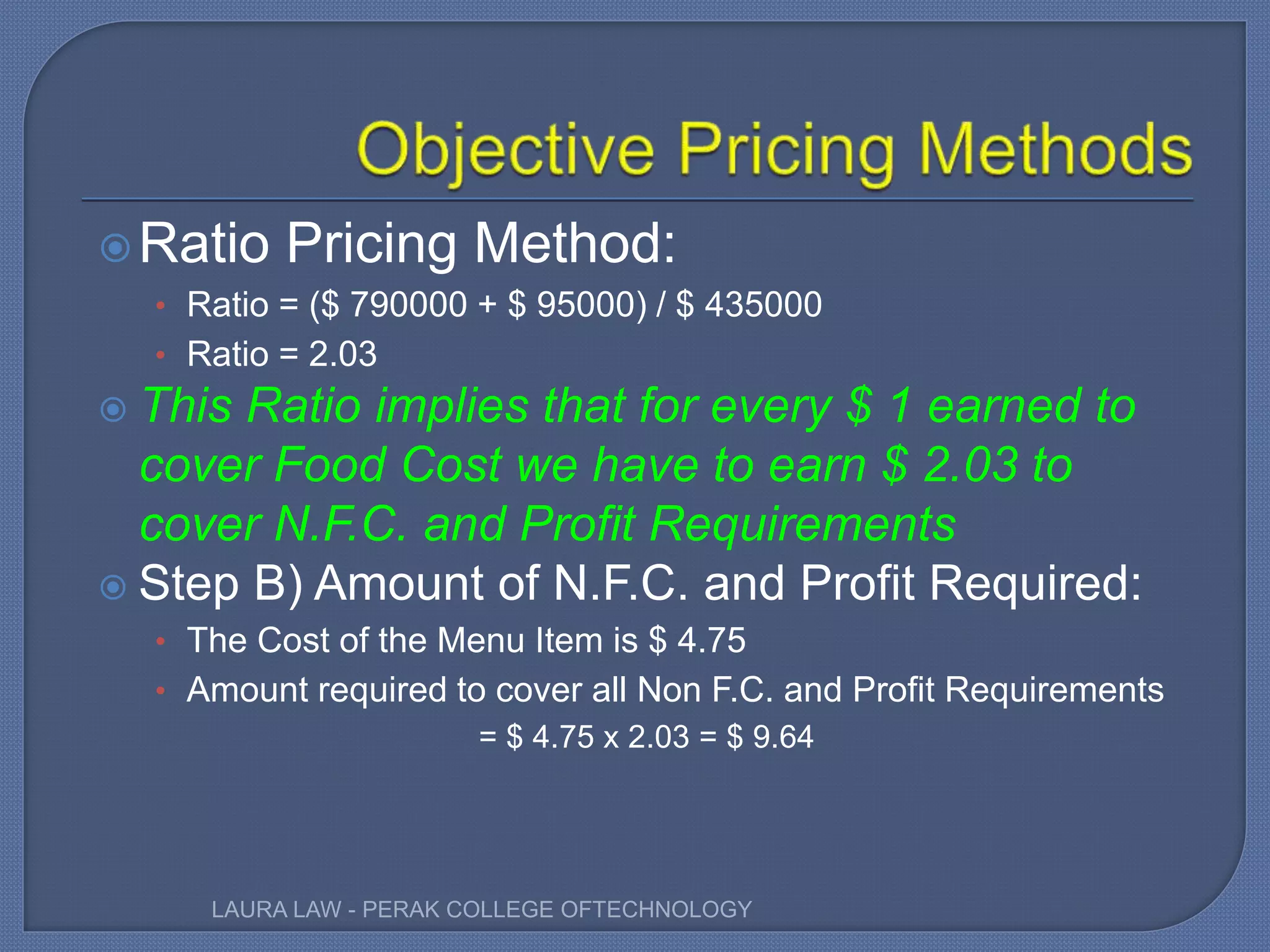

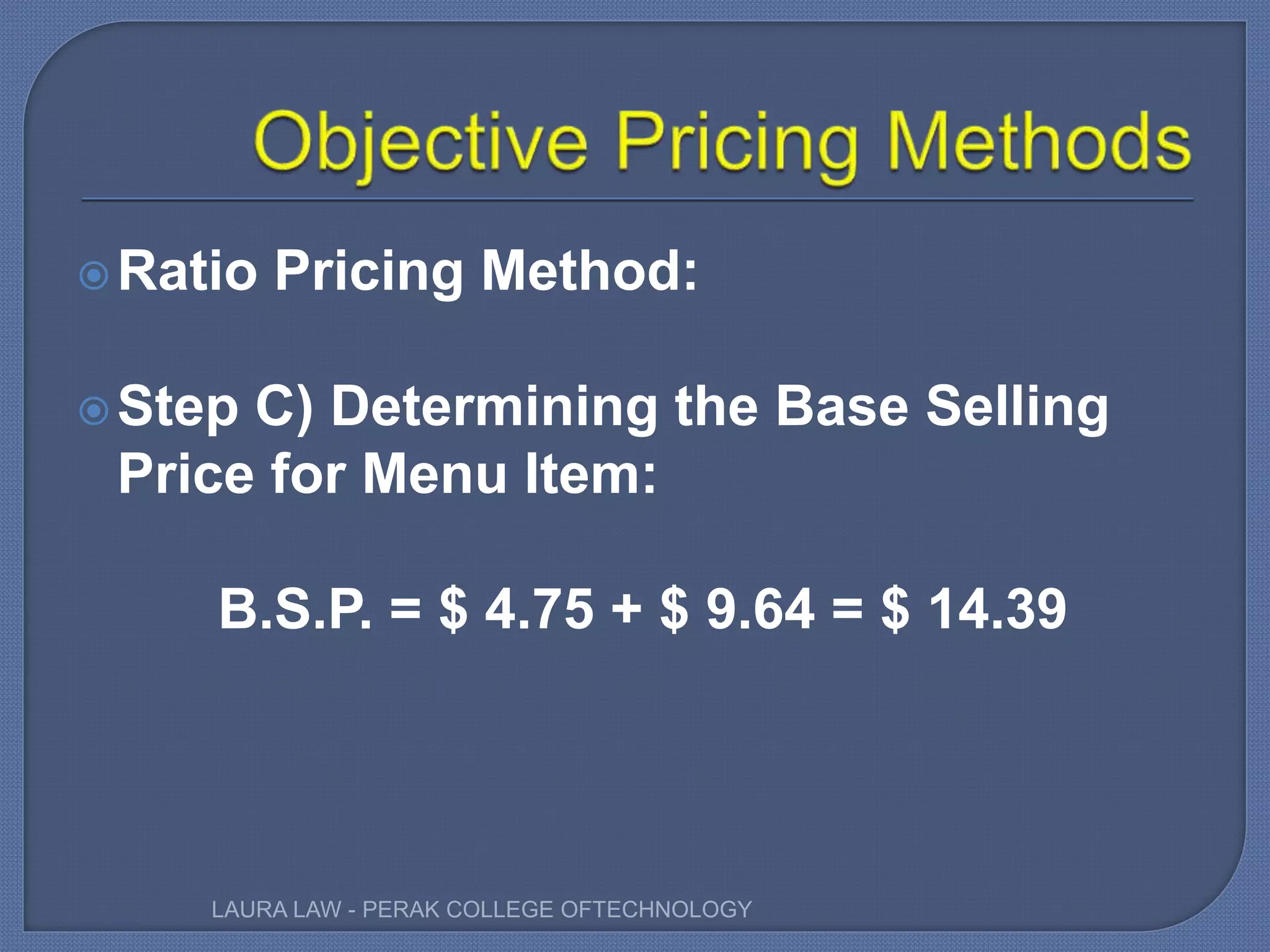

Explains the ratio pricing method for establishing menu item pricing based on food costs and non-food costs.

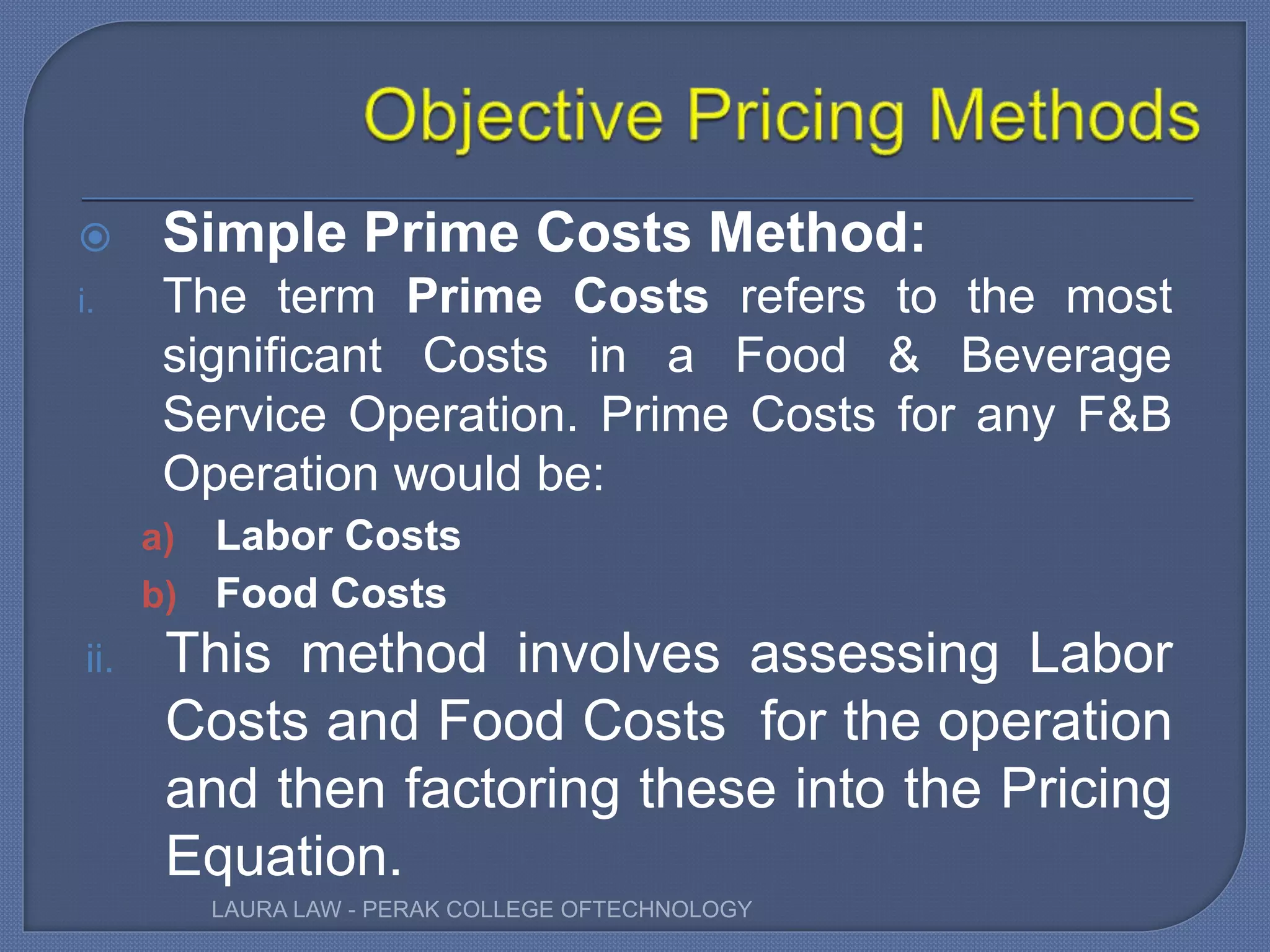

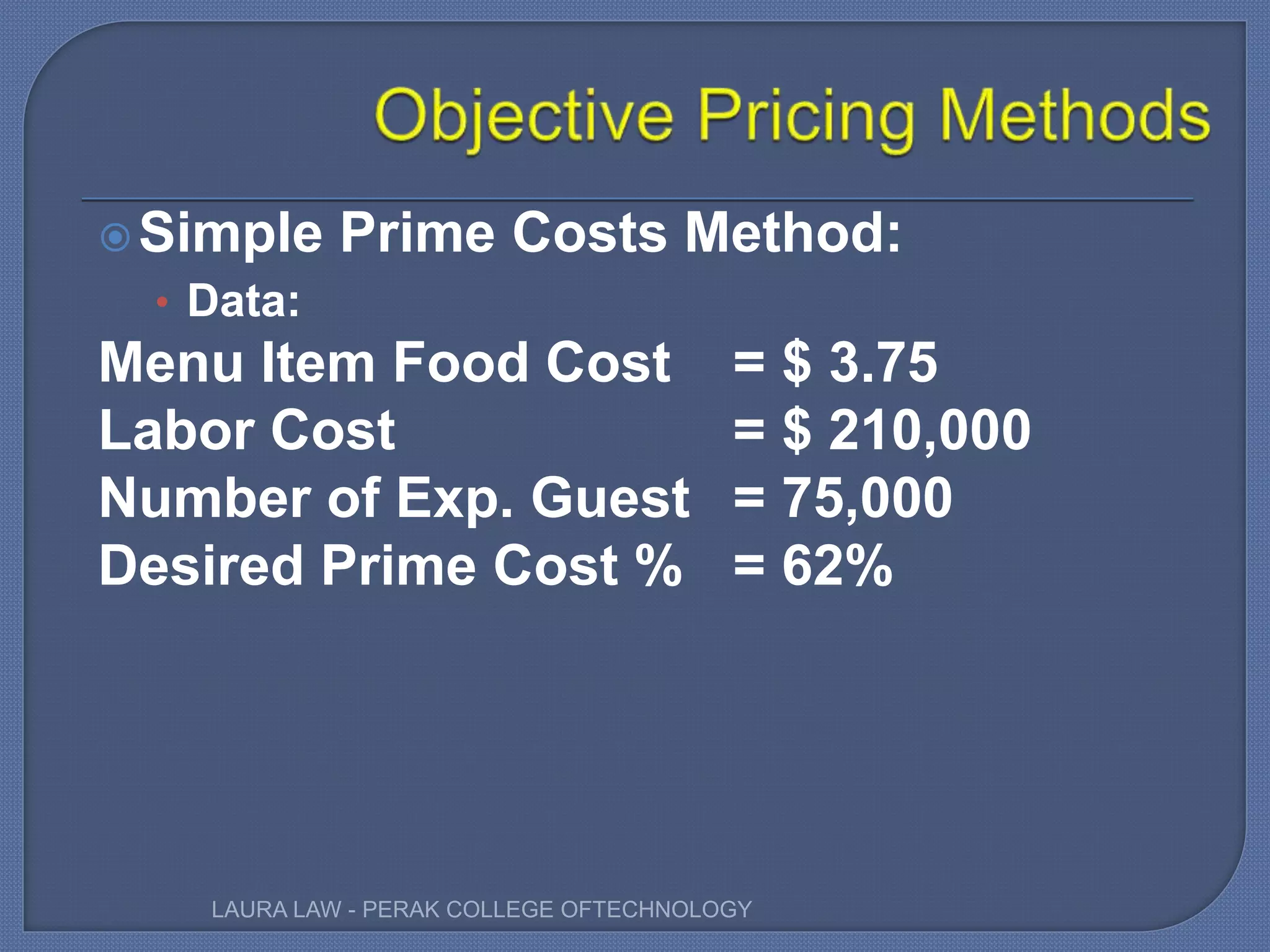

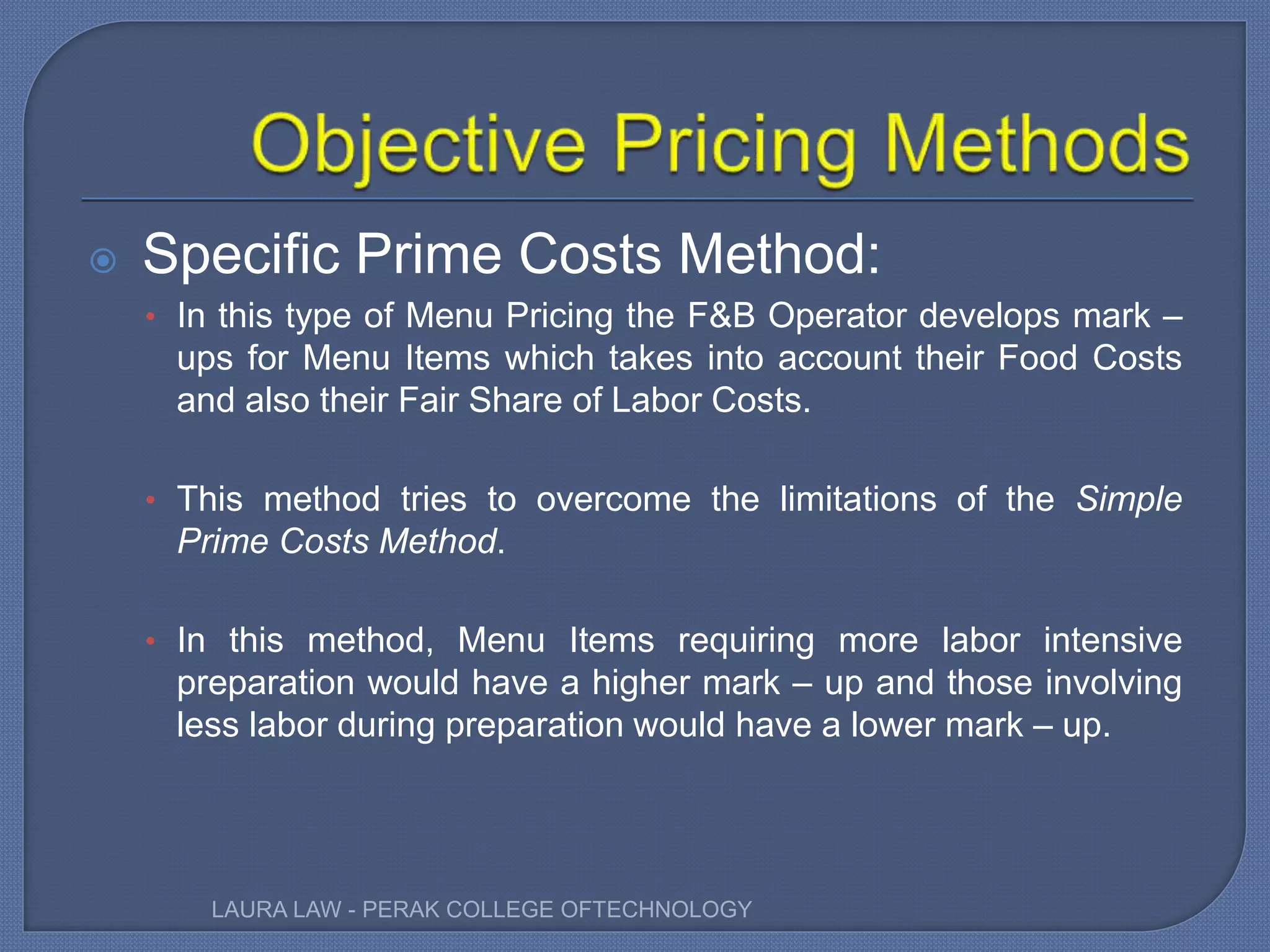

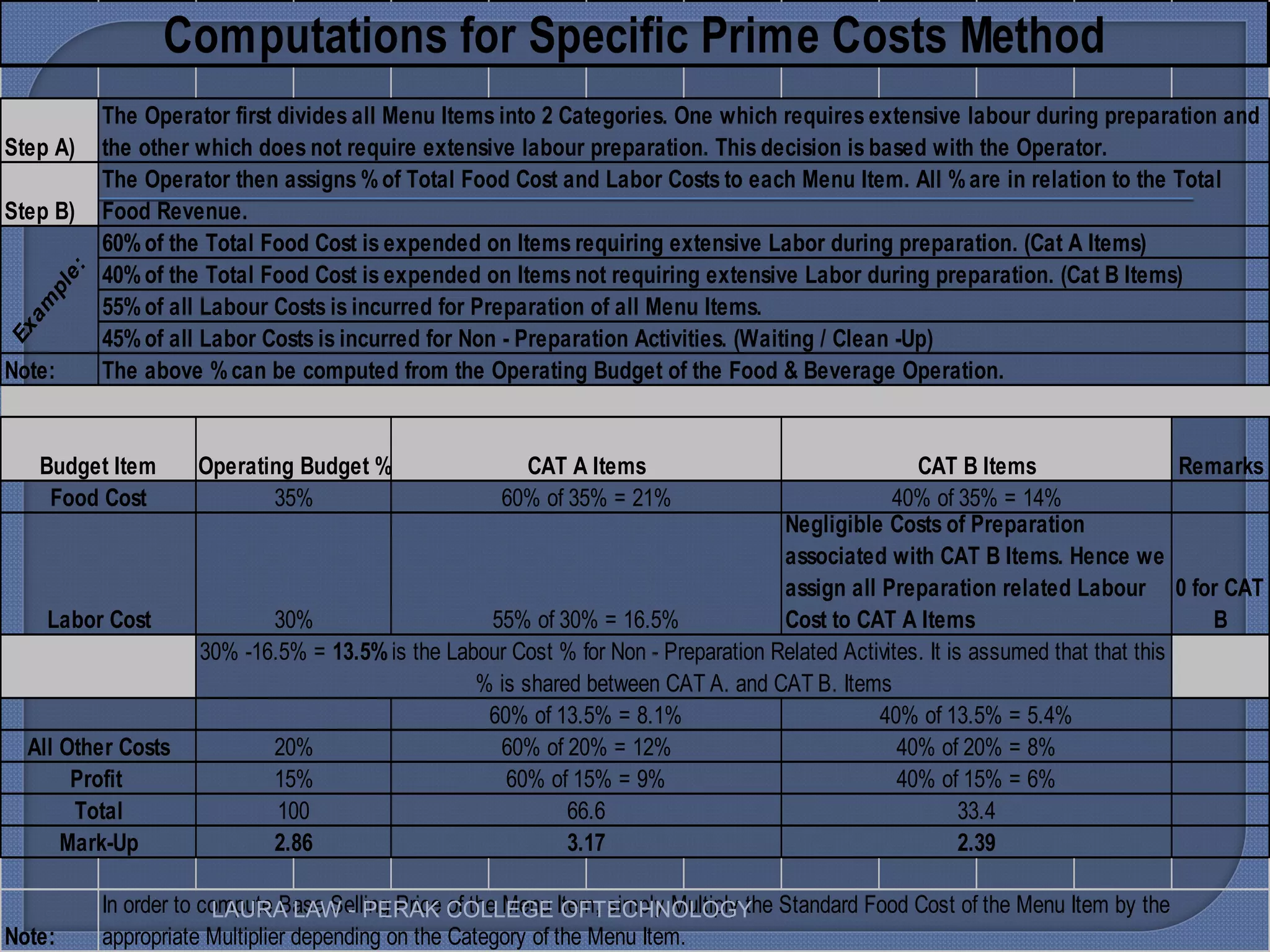

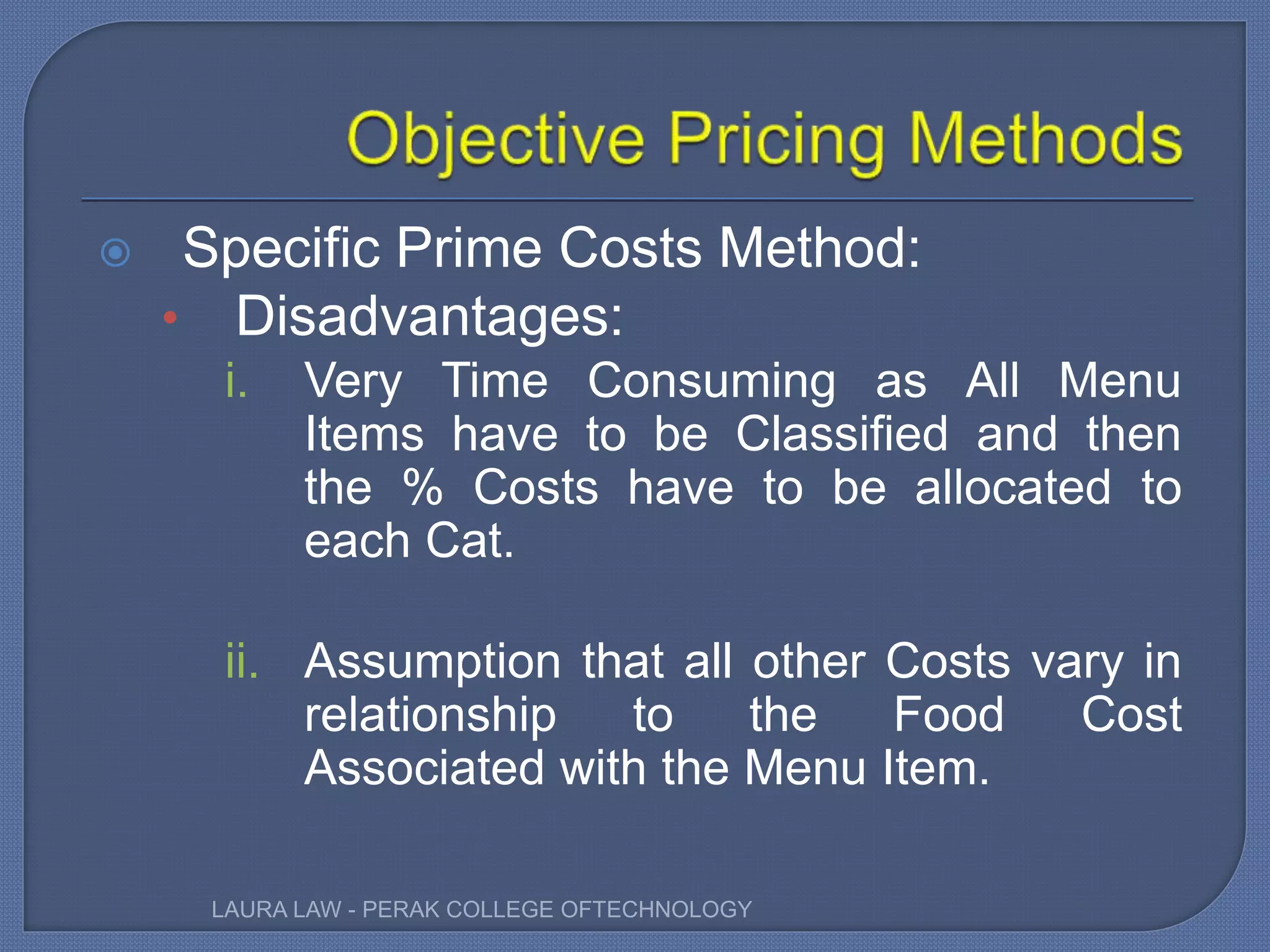

Discusses the specific prime costs method, affecting labor and food costs in menu pricing.