Downloaded 12 times

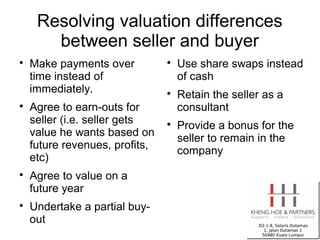

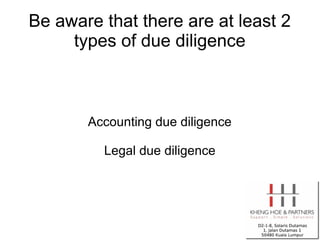

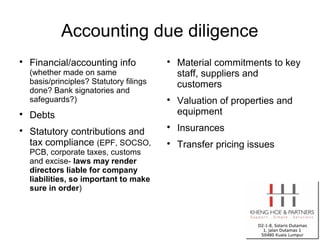

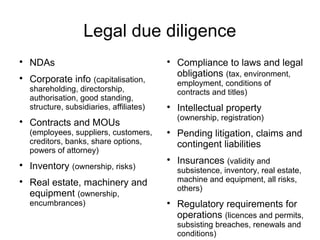

The document provides an overview of mergers and acquisitions for private companies. It discusses common reasons why companies sell, factors to consider when deciding whether to buy another company, important questions to ask before an acquisition, the typical M&A process, negotiation strategies, resolving valuation differences, types of due diligence, common deal structures, important shareholder agreement clauses, post-merger integration, and reminders for M&A transactions.

![Insights Newsletter Autumn 2011.Final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/insightsnewsletterautumn2011final1-13269027987541-phpapp02-120118100706-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)