Downloaded 77 times

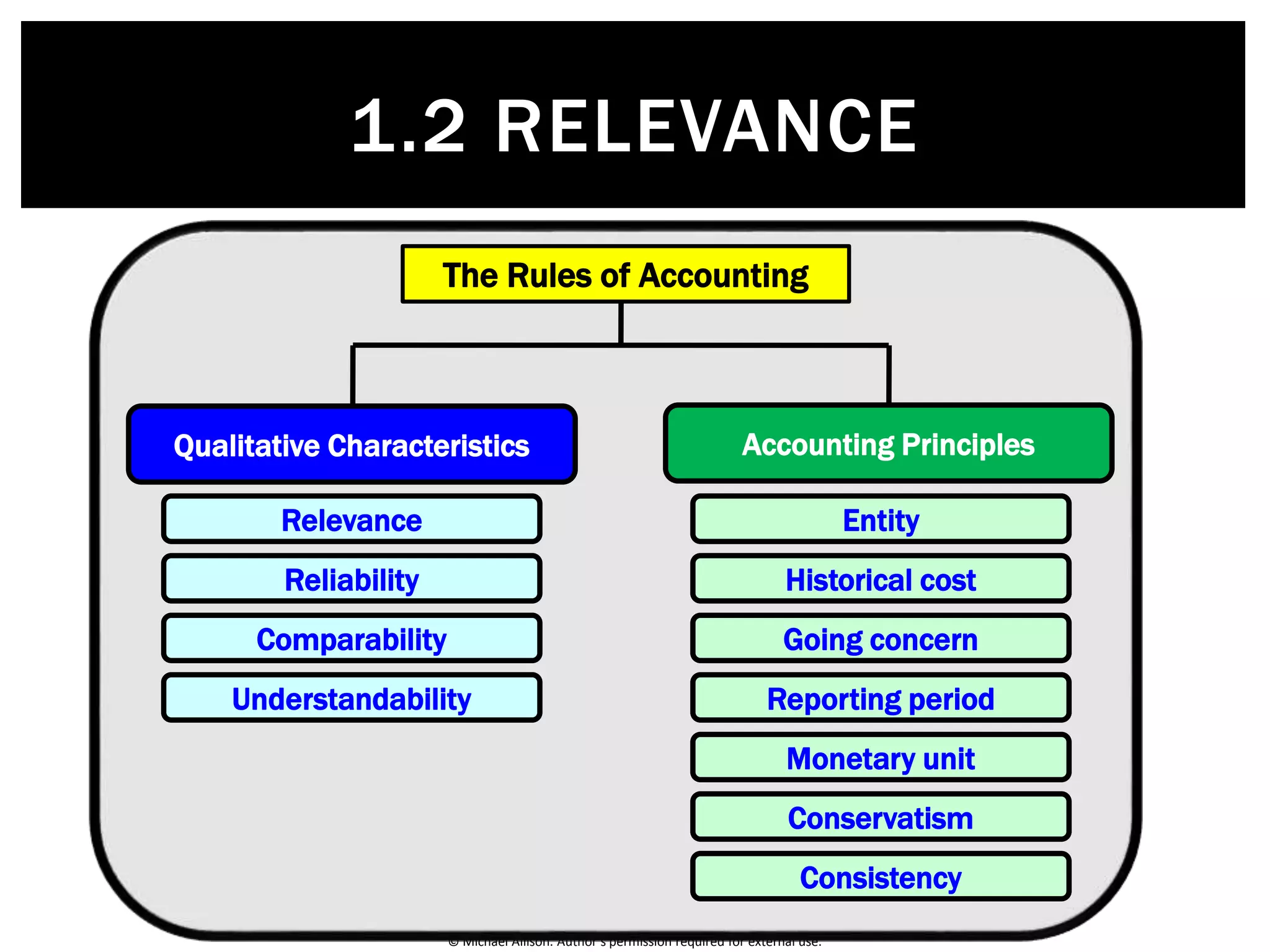

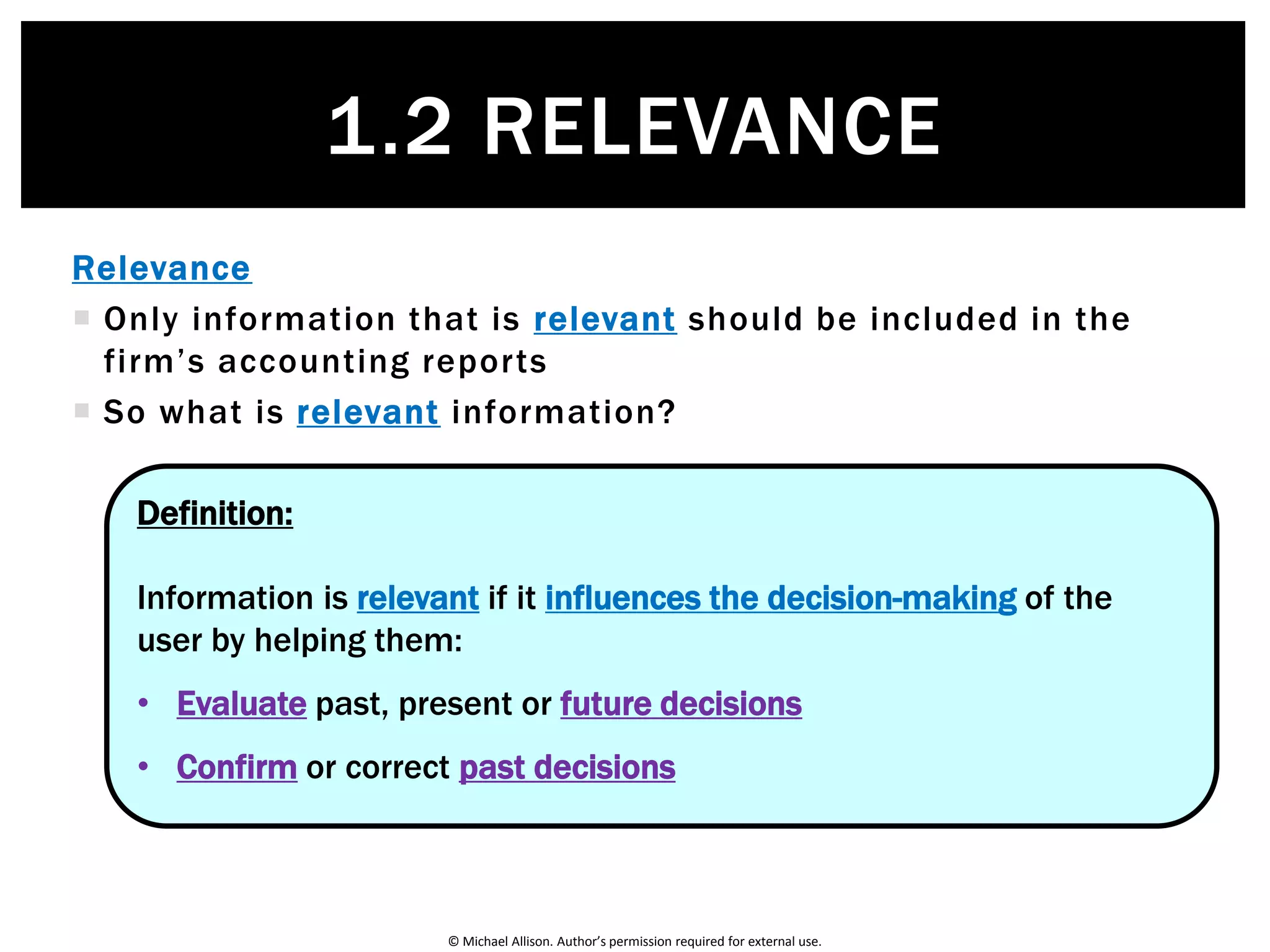

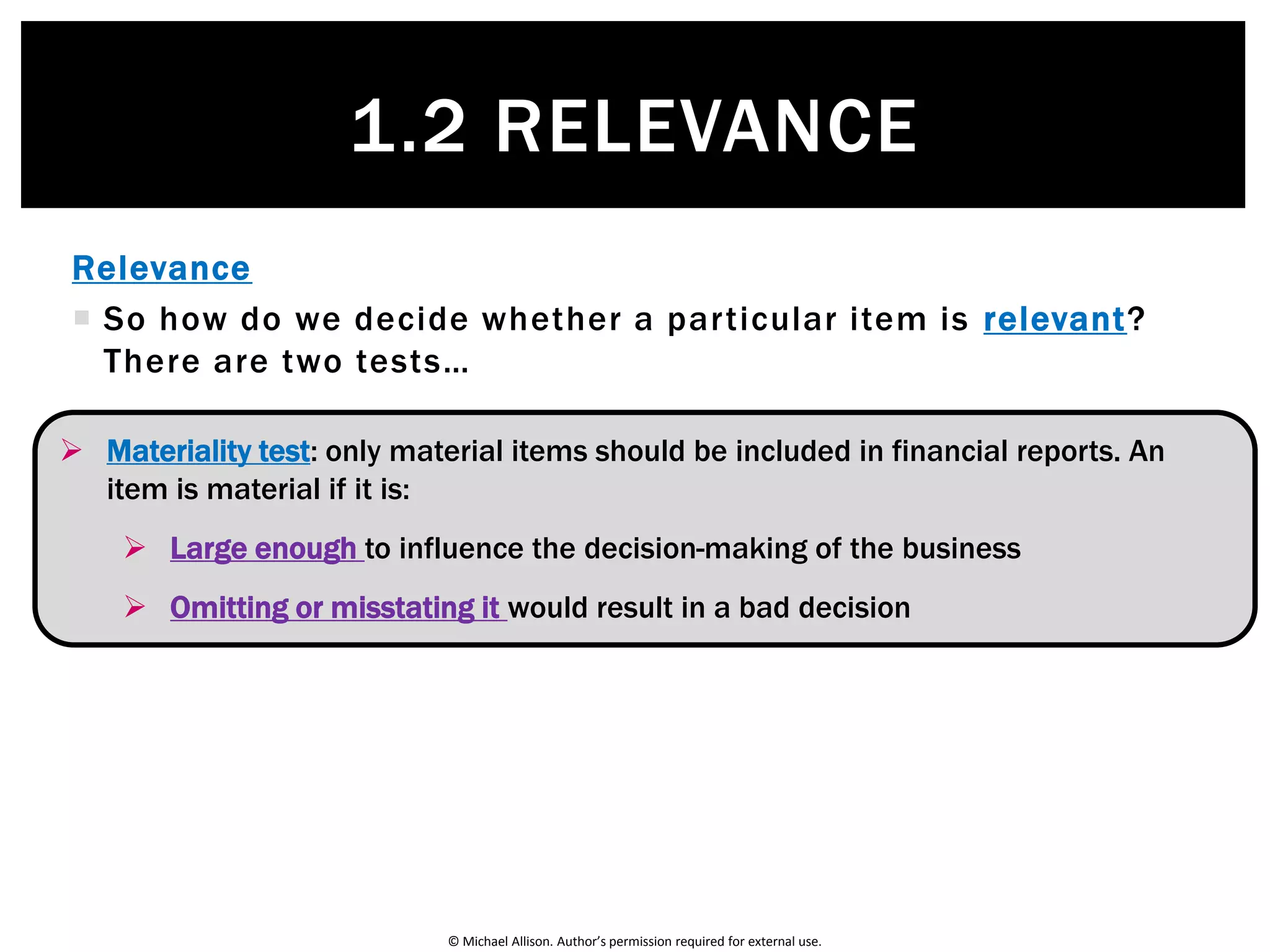

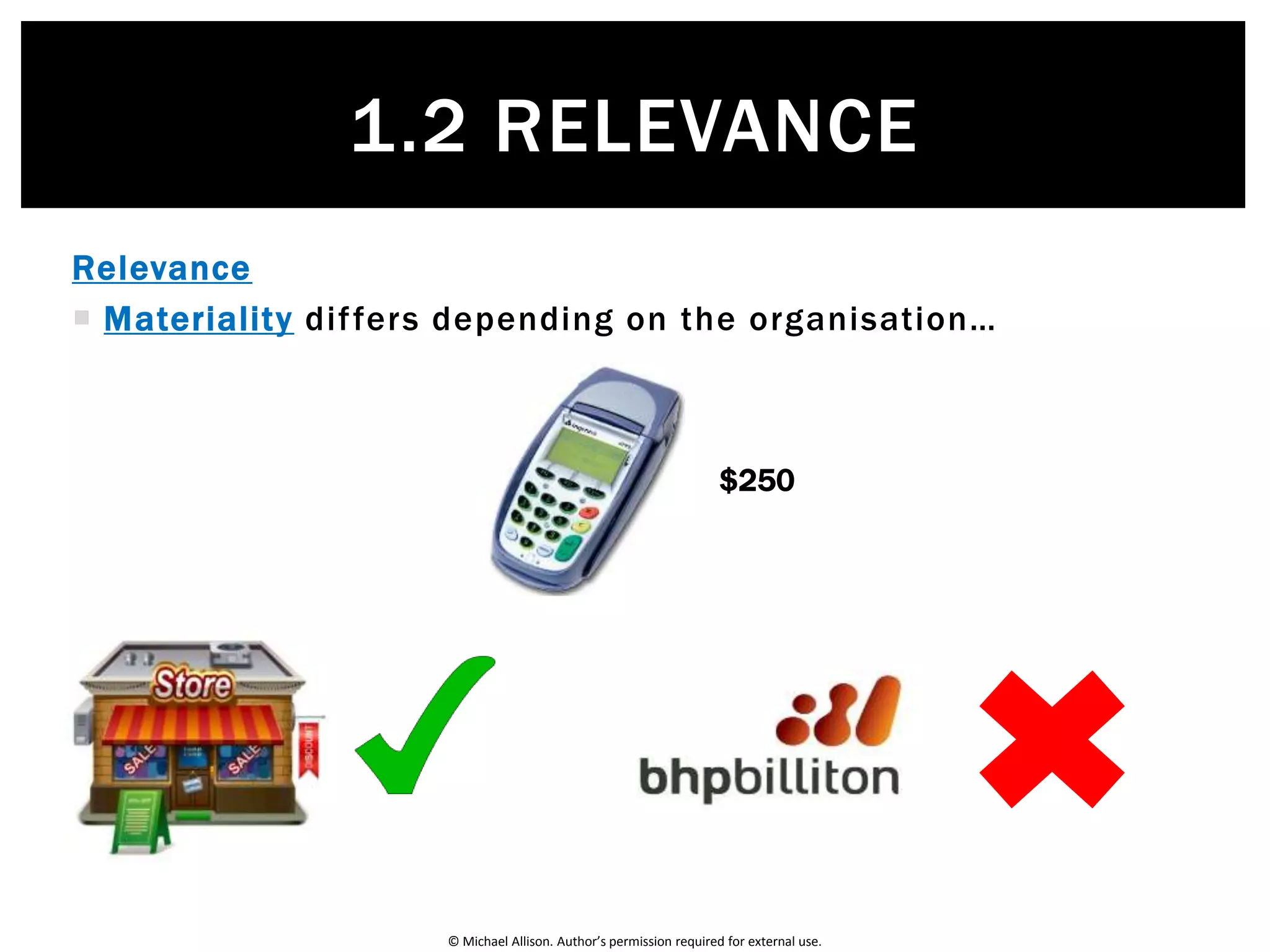

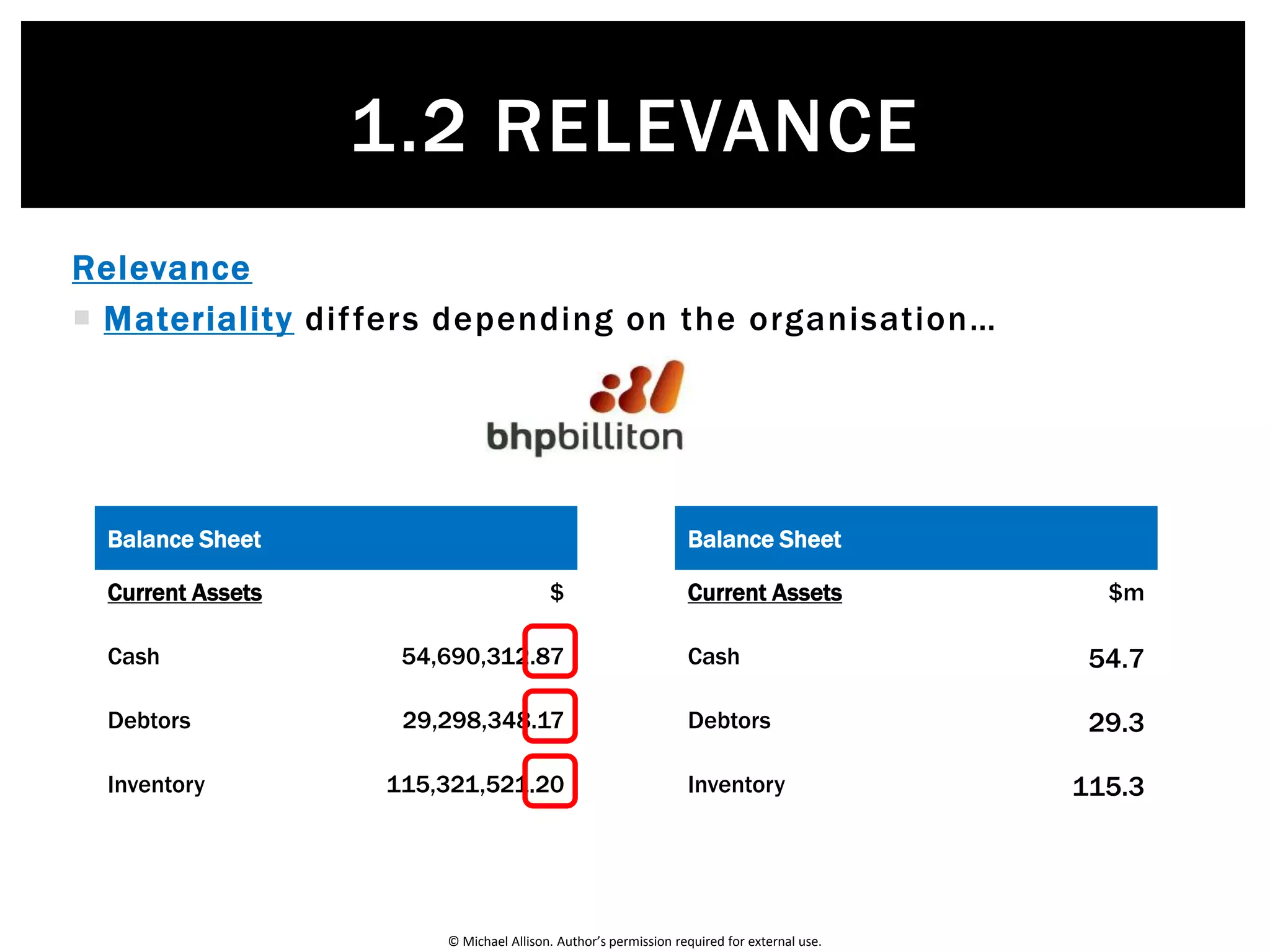

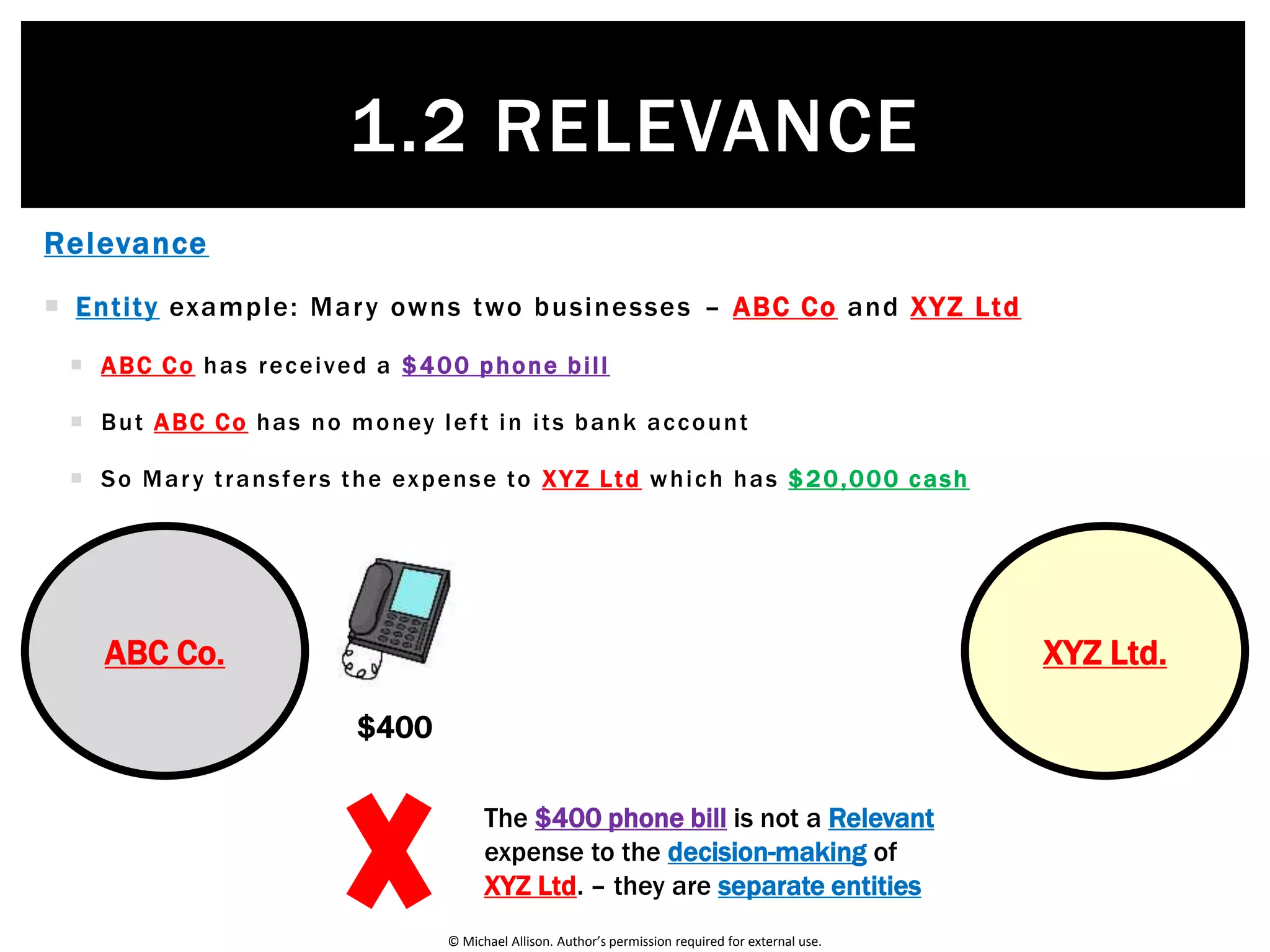

The document discusses the concept of relevance in accounting, emphasizing that only information that influences decision-making should be included in financial reports. It outlines two key tests for determining relevance: the materiality test and the entity test, providing examples to illustrate the separation of personal and business entities. The document also touches on the varied thresholds for materiality based on organizational context.