Downloaded 33 times

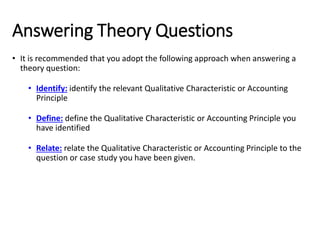

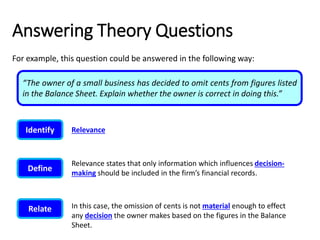

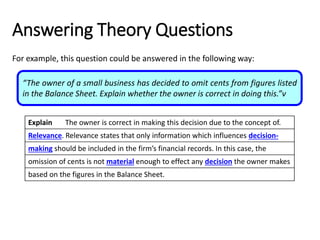

The document outlines a method for answering theory questions in accounting by identifying relevant qualitative characteristics or principles, defining them, and relating them to the specific question. An example illustrates how an owner omitting cents in a balance sheet can be justified through the concept of relevance, which states only information impacting decision-making should be included. It concludes that the omission is correct as it does not materially affect decisions based on the figures.