Governor Olli Rehn: Dialling back monetary restraint

10 February Daily market report

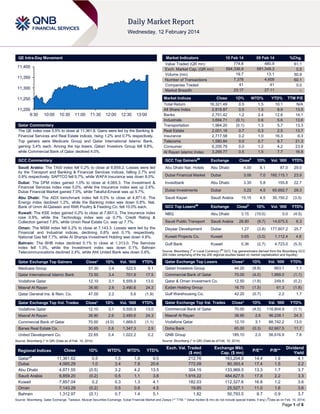

1. QE Intra-Day Movement

Market Indicators

11,400

11,350

11,300

Market Indices

11,250

11,200

9:30

10 Feb 14

774.8

594,336.9

19.7

7,378

41

23:17

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.5% to close at 11,361.6. Gains were led by the Banking &

Financial Services and Real Estate indices, rising 1.2% and 0.7% respectively.

Top gainers were Medicare Group and Qatar International Islamic Bank,

gaining 3.4% each. Among the top losers, Qatari Investors Group fell 9.8%,

while Commercial Bank of Qatar declined 4.0%.

09 Feb 14

480.9

591,349.3

13.1

4,609

41

27:11

%Chg.

61.1

0.5

50.9

60.1

0.0

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

16,321.49

2,818.87

2,751.42

3,694.71

1,964.20

2,001.18

2,717.58

1,580.84

6,200.79

3,269.77

0.5

0.5

1.2

(0.1)

(0.1)

0.7

0.2

0.0

0.0

0.5

1.5

1.5

2.4

0.6

1.3

0.3

1.0

0.7

1.2

1.5

10.1

8.9

12.6

5.6

5.7

2.5

16.3

8.7

4.2

7.7

N/A

13.5

14.1

13.6

13.3

13.7

6.3

21.3

23.9

16.8

Vol. ‘000

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Saudi Arabia: The TASI index fell 0.2% to close at 8,859.2. Losses were led

by the Transport and Banking & Financial Services indices, falling 2.7% and

0.8% respectively. SAPTCO fell 9.7%, while WAFA Insurance was down 8.0%.

Abu Dhabi Nat. Hotels

Abu Dhabi

4.00

8.1

87.0

29.0

Dubai Financial Market

Dubai

3.06

7.0

160,115.1

23.9

Dubai: The DFM index gained 1.0% to close at 4,065.3. The Investment &

Financial Services index rose 5.0%, while the Insurance index was up 2.6%.

Dubai Financial Market gained 7.0%, while Takaful-Emarat was up 5.7%.

Investbank

Abu Dhabi

3.30

5.8

155.8

22.7

Dubai Investments

Dubai

3.22

4.5

65,692.7

29.3

Abu Dhabi: The ADX benchmark index fell 0.5% to close at 4,871.6. The

Energy index declined 1.2%, while the Banking index was down 0.8%. Nat.

Bank of Umm Al-Qaiwain and RAK Poultry & Feeding Co. fell 10.0% each.

Saudi Kayan

Saudi Arabia

15.15

4.5

30,150.2

(3.5)

GCC Top Losers

Exchange

Kuwait: The KSE index gained 0.2% to close at 7,857.0. The Insurance index

rose 0.9%, while the Technology index was up 0.7%. Credit Rating &

Collection gained 7.8%, while Union Real Estate Co. was up 7.7%.

NBQ

Abu Dhabi

Saudi Public Transport

Saudi Arabia

Oman: The MSM index fell 0.2% to close at 7,143.3. Losses were led by the

Financial and Industrial indices, declining 0.6% and 0.1% respectively.

National Gas fell 7.7%, while Al Sharqia Investment Holding was down 4.8%.

Deyaar Development

Kuwait Projects Co.

Gulf Bank

Bahrain: The BHB index declined 0.1% to close at 1,313.0. The Services

index fell 1.3%, while the Investment index was down 0.1%. Bahrain

Telecommunications declined 2.4%, while Ahli United Bank was down 0.6%.

Medicare Group

Close*

1D%

Vol. ‘000

YTD%

57.30

Qatar Exchange Top Gainers

3.4

522.5

9.1

##

YTD%

#

1D%

3.15

(10.0)

5.0

(4.5)

28.80

(9.7)

14,675.5

6.3

Dubai

1.27

(3.8)

177,607.2

25.7

Kuwait

0.65

(3.0)

1,112.4

4.8

Kuwait

0.36

(2.7)

4,723.0

(5.3)

Close

Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

Qatari Investors Group

44.20

(9.8)

663.1

1.1

70.00

(4.0)

1,669.0

(1.1)

Qatar Exchange Top Losers

YTD%

Qatar International Islamic Bank

72.50

3.4

701.9

17.5

Commercial Bank of Qatar

Vodafone Qatar

12.10

3.1

5,555.9

13.0

Qatar & Oman Investment Co.

12.50

(1.8)

249.5

(0.2)

Masraf Al Rayan

38.90

2.6

2,490.6

24.3

Ezdan Holding Group

16.70

(1.5)

61.3

(1.8)

Qatar General Ins. & Rein. Co.

47.00

2.2

5.6

(1.9)

Gulf Warehousing Co.

42.20

(0.7)

2.2

1.7

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

YTD%

Vodafone Qatar

12.10

3.1

5,555.9

13.0

Commercial Bank of Qatar

70.00

(4.0)

116,804.9

(1.1)

Masraf Al Rayan

38.90

2.6

2,490.6

24.3

Masraf Al Rayan

38.90

2.6

96,238.1

24.3

Commercial Bank of Qatar

70.00

(4.0)

1,669.0

(1.1)

Vodafone Qatar

12.10

3.1

66,742.2

13.0

Barwa Real Estate Co.

30.65

0.8

1,347.3

2.9

Doha Bank

65.00

(0.3)

62,667.5

11.7

United Development Co.

22.65

0.4

1,022.2

0.2

QNB Group

185.10

2.0

56,616.9

7.6

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR) (Data as of Feb. 10, 2014)

Source: Bloomberg (* in QR) (Data as of Feb. 10, 2014)

Regional Indices

Qatar*#

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

11,361.62

4,065.29

4,871.55

8,859.20

7,857.04

7,143.28

1,312.97

0.5

1.0

(0.5)

(0.2)

0.2

(0.2)

(0.1)

1.5

3.4

3.2

0.5

0.3

0.5

0.7

1.8

7.8

4.2

1.1

1.3

0.8

1.4

9.5

20.6

13.5

3.8

4.1

4.5

5.1

Exch. Val. Traded

($ mn)

212.76

772.09

304.15

1,916.22

182.03

19.85

1.82

Exchange Mkt.

Cap. ($ mn)

163,204.9

80,393.4

133,969.5

484,627.5

112,327.6

25,527.1

50,793.5

P/E**

P/B**

14.4

17.4

13.3

17.8

16.8

11.0

8.7

1.9

1.5

1.7

2.2

1.2

1.6

0.9

Dividend

Yield

4.1

2.2

3.7

3.3

3.6

3.6

3.7

#

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as on Feb. 10, 2014)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.5% to close at 11,361.6. The Banking &

Financial Services and Real Estate indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

64.70%

70.76%

(46,921,494.42)

Non-Qatari

Medicare Group and Qatar International Islamic Bank were the

top gainers, rising 3.4% each. Among the top losers, Qatari

Investors Group fell 9.8%, while Commercial Bank of Qatar

declined 4.0%.

Buy %*

35.30%

29.24%

46,921,494.42

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Monday rose by 50.9% to 19.7mn

from 13.1mn on Sunday. Further, as compared to the 30-day

moving average of 11.0mn, volume for the day was 79.9%

higher. Vodafone Qatar and Masraf Al Rayan were the most

active stocks, contributing 28.2% and 12.6% to the total volume

respectively.

Ratings, Earnings and Global Economic Data

Ratings Updates

Company

BMI Bank (BMI)

Agency

Market

Bahrain

Moody's

Type*

Deposit Ratings# /

BFSR

Old Rating

New Rating

E+

Rating Change

Outlook Change

–

Ba1/ E+

Outlook

Negative

/ Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, BFSR- Bank Financial Strength Rating) (#Rating confirmed)

Earnings Releases

Company

Market

Currency

Gulf Navigation (GULFNAV)

Dubai

Dubai

AED

RAK Properties

Abu Dhabi

AED

Foodco Holding

Abu Dhabi

% Change

YoY

Operating Profit

(mn) FY2013

% Change

YoY

Net Profit (mn)

FY2013

% Change

YoY

–

–

–

–

-697.9

372.1%

307.6

6.9%

–

–

44.3

8.8%

322.3

-49.8%

182.4

-1.8%

150.6

2.4%

98.4

-12.2%

–

–

33.8

140.5%

739.1%

AED

Alliance Insurance

Revenue

(mn) FY2013

AED

United Industries Co. (UIC)

Kuwait

KD

–

–

–

–

28.1

Gulf Hotels (Oman) Co.

Computer Stationery

Industry Co. (CSII)

Global Financial Investments

Holding (GFI)

Bahrain Kuwait Insurance

Co. (BKIC)

Bahrain Car Parks Co.

(CPARK)

United Paper Industries

(UPI)*

Oman

OMR

8.8

5.4%

–

–

2.4

0.4%

Oman

OMR

3.0

-17.8%

–

–

0.2

200.2%

Oman

OMR

4.5

139.6%

–

–

1.9

1.0%

Bahrain

BHD

12.0

2.4%

–

–

3.7

-12.2%

Bahrain

BHD

–

–

0.9

19.6%

0.8

6.9%

Bahrain

BHD

8.2

-3.2%

–

–

0.3

-49.4%

Source: Company data, DFM, ADX, MSM (*Results for the nine months ended December 31, 2013)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

02/11

US

BLS

JOLTs Job Openings

December

3.99mn

3.98mn

4.03mn

02/11

US

US Census Bureau

Wholesale Inventories MoM

December

0.30%

0.50%

0.50%

02/11

US

US Census Bureau

Wholesale Trade Sales MoM

December

0.50%

0.70%

1.00%

02/10

EU

Sentix Behavioral Ind.

Sentix Investor Confidence

February

13.3

10.1

11.9

02/10

France

INSEE

Industrial Production MoM

December

-0.30%

-0.20%

1.20%

02/10

France

INSEE

Industrial Production YoY

December

0.50%

1.00%

1.70%

02/10

France

INSEE

Manufacturing Production MoM

December

0.00%

0.30%

0.20%

02/10

France

INSEE

Manufacturing Production YoY

December

0.50%

0.70%

1.60%

02/10

UK

Lloyds Bank

Lloyds Employment Confidence

January

-2

–

-12

02/11

UK

BRC

BRC Sales Like-For-Like YoY

January

3.90%

0.80%

0.40%

02/10

Italy

ISTAT

Industrial Production MoM

December

-0.90%

0.00%

0.30%

02/10

Italy

ISTAT

Industrial Production WDA YoY

December

-0.70%

0.90%

1.50%

02/10

Italy

ISTAT

Industrial Production NSA YoY

December

2.40%

4.70%

-1.70%

02/10

Japan

Bank of Japan

Housing Loans YoY

4Q2013

2.90%

–

3.00%

02/10

Japan

ESRI

Consumer Confidence Index

January

40.5

42.0

41.3

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 6

3. News

Qatar

QIMD reports net profit of QR202.1mn in 2013 – QIMD’s

financials revealed a net profit of QR202.1mn in 2013 versus

QR208.2mn in 2012. Earnings per Share (EPS) amounted to

QR5.11 in 2013 compared to QR5.26 in 2012. The company’s

Board of Directors recommended 20% bonus shares along with

the results. (QE)

QGRI reports net profit of QR1.37bn in 4Q2013 – Qatar

General Insurance & Reinsurance Company (QGRI) has

reported a net profit of QR1.37bn in 4Q2013 as compared to

QR19.3mn in 3Q2013. The net earned premiums was

QR52.8mn in 4Q2013 indicating a fall of 0.1% QoQ. For the full

year 2013, EPS amounted to QR36.96 vs. QR3.04 in 2012. The

significant increase in 4Q2013 net income is due to fair value

gain on investment properties of QR2.0bn in 2013 vs.

QR39.9mn in 2012. Meanwhile, QGRI’s board of directors has

recommended a cash dividend of QR1.50 and a 20% stock

dividend per share, which will have to be approved by

shareholders at the annual general assembly, scheduled on

March 16, 2014. (QE)

QFLS report net profit QR1.2bn profit in 2013 – Qatar Fuel

Company (Woqod) posted a net profit of QR1.2bn in 2013 vs.

QR1.1bn in 2012. Earnings per Share (EPS) amounted to

QR18.72 in 2013 compared to QR17.70 in 2012. QFLS’ Board

of Directors recommended cash dividends of QR10.0 per share,

in addition to 30% bonus shares i.e. 3 shares per 10 outstanding

shares. (QE)

CBQK curbs expansion plans – The Commercial Bank of

Qatar (CBQK) said it would freeze expenses and curb

expansion plans. CBQK has abandoned its plans to open a new

branch in every Turkish city, focusing on cost cutting in order to

protect profitability. CBQK's acquisition of Turkish lender ABank

and investment in staff and infrastructure saw costs balloon 40%

YoY in 2013. (Bloomberg)

Trading suspension in QIIK’s shares on February 12 due to

its AGM & EGM – The Qatar Exchange has announced trading

suspension in Qatar International Islamic Bank’s (QIIK) shares

on February 12, 2014 due to its AGM & EGM being held on that

day. (QE)

Asteco: Qatar's land sales rise 10% in 4Q2013 – According to

a report released by Asteco, the real estate market in Qatar

witnessed strong growth in 4Q2013 with land sales accounting

for about 75% of all property transactions in the last quarter. The

total value of land transactions in 4Q2013 reached QR6.3bn, up

by 10% from QR5.7bn in 3Q2013. The volume of transactions

also increased with over 1,500 properties changing hands.

(Peninsula Qatar)

International

Janet Yellen: Expect continuity at Fed – The Federal Reserve

Chairman Janet Yellen sought to reassure investors that she will

embrace the approach to interest-rate policy that her

predecessor, Ben Bernanke, pursued before he stepped down

as Chairman last month. Yellen told Congress that if the

economy keeps improving, the Fed will take "further measured

steps" to reduce the support it is providing through bond

purchases. Yellen said she expect a "great deal of continuity"

with Bernanke. She signaled that she supports his view that the

economy is strengthening enough to withstand a pullback in

stimulus but that rates should stay low to further improve a stilllackluster economy. (ET)

China's January trade beats forecasts, import growth at 6month high – China's trade performance zoomed past

forecasts in January as import growth hit a six-month high,

confounding market expectations that the country's economy is

mired in a deepening slowdown. China's Customs

Administration said the value of country's total exports climbed

10.6% in January from a year earlier, more than five times

market forecasts for a 2% rise. The value of imports jumped

10% from a year ago, a pace not seen since July and handily

beating market predictions for a 3% gain. Imports of crude oil,

iron ore and copper all hit record highs, according to customs

data. The country's trade surplus rose to $31.9bn, well above

forecasts of $23.7bn and December's $25.6bn. (ET)

Regional

RCJY awards SR226mn contracts for infrastructure projects

– The Royal Commission for Jubail & Yanbu’s (RCJY)

President, Prince Saud bin Abdullah Al-Thunayyan, has signed

three contracts for the construction and maintenance of a series

of infrastructure projects in the two industrial cities. The projects,

worth SR226mn, were awarded to a number of national firms.

The contracts included construction of educational facilities and

provision of operational & maintenance services for healthcare

facilities in Yanbu Industrial City in addition to rehabilitation and

beautification works of roads in Jubail Industrial City.

(GulfBase.com)

Kingdom issued 1.7mn work visas in 2013 despite Nitaqat –

Saudi Arabia's foreign missions issued over 1.7mn recruitment

visas in 2013 despite the Labor Ministry's Nitaqat nationalization

campaign to replace expat workers with Saudi nationals. The

Foreign Ministry said its 112 foreign missions and 12 temporary

Haj missions issued a total of 10.36mn visas in 2013, indicating

a 3.8% decline over the previous year’s 10.7mn visas.

(GulfBase.com)

MPC to shut ammonia plant for maintenance – Saudi Arabian

Mining Company (MA’ADEN) announced that its subsidiary,

Maaden Phosphate Company (MPC) will conduct a scheduled

maintenance activity in its Ammonia plant located in the

company’s complex at Ras Al Khair city. The maintenance

shutdown will start from February 12, 2014 and will take

approximately four weeks. The plant produces ammonia that is

used for manufacturing of Diammonium Phosphate (DAP).

During the shutdown, the DAP plant will maintain production

using its existing inventory. Thus, the maintenance will have no

impact on the company’s ability to meet its obligations and will

have no significant financial impact as well. (Tadawul)

Saudi Cargo enters into agreement with Samba Capital for

its IPO – Saudi Airlines Cargo Company (Saudi Cargo) has

entered into an agreement with Samba Capital & Investment

Management Company, the investment arm of Samba Financial

Group, to act as the financial advisor and lead manager for the

IPO of Saudi Cargo which intends to list its shares on Tadawul.

(GulfBase.com)

Saudi CMA approves JADCO’s capital increase – The Saudi

CMA’s board has approved Al-Jouf Agriculture Development

Company’s (JADCO) request for capital increase from

SR250mn to SR300mn by issuing one bonus share for every

five existing shares. This increase will be paid by transferring

SR50mn from the retained earnings account to the company's

capital. Consequently, the company's outstanding shares will

increase from 25mn to 30mn, indicating an increase of 5mn

shares. The eligibility for the bonus shares is limited to the

shareholders who are registered at the close of trading on the

Page 3 of 6

4. day of the extraordinary general assembly, which will be

determined at a later date. (Tadawul)

JLL: Dubai house prices to reach pre-crisis levels by 2015 –

According to Jones Lang LaSalle (JLL), Dubai house prices are

only 15% short of their 2008 peak and will return to their precrisis highs within 18 months. The Emirate outpaced all other

major property markets last year, with prices climbing more than

22% as billions of dollars of government real estate projects

triggered a buying spree among investors. The fast growth,

however, has raised concerns about a potential repeat of the

property market bubble that sent prices plunging by 50% after

the 2008 financial crisis. JLL’s Head of Research for MENA

Craig Plumb stated that JLL expects prices to get close to precrisis levels by the end of this year, since they have already

reached that level in some locations. (Gulf-Times.com)

DSI unit wins AED166mn water treatment projects in

Europe – Passavant-Roediger, a German subsidiary of Drake &

Scull International (DSI), has won three major projects worth

AED166mn for water and wastewater treatment plants in

Romania, Bosnia-Herzegovina and Turkey. Under the

agreement terms, Passavant-Roediger will undertake the

execution of the civil, mechanical, electrical along with SCADA

works for wastewater treatment plants in the cities of Sinaia and

Breaza and drinking water treatment plants in Comarnic and

Sinaia in Romania, to be completed by 2015. The company’s

scope of work in Bosnia-Herzegovina will involve the

rehabilitation of the Sarajevo Wastewater Treatment Plant to

increase its capacity to 170, 000 cubic meters of wastewater per

day. Work on the project is expected to be completed by 2016.

(DFM)

Emirates to idle 10% jets as Dubai runway revamp weighs

on flights – Emirates Airline will idle 10% of its fleet for almost

three months, crimping sales, as runway repairs curtail capacity

at its Dubai International hub. Emirates Airline’s President Tim

Clark said the company will ground 18 to 20 planes, in Dubai.

Fleet expansion will not be affected, with Emirates still looking to

add 22 jets this year. (GulfBase.com)

EFECO wins AED878mn MEP contract at Abu Dhabi airport

– Arabtec Holding announced that its subsidiary, Emirates

Falcon Electromechanical Company (EFECO), has been

awarded a JV contract to carry out mechanical, electrical &

plumbing works (MEP) at the new Abu Dhabi International

Airport Midfield Terminal Building. The 700,000-square meter

large terminal building is a key strategic infrastructure project in

Abu Dhabi, which will accommodate up to 65 aircraft, including

the Airbus A‐380, with an expected capacity of 30mn

passengers per year. This project is currently under construction

by a JV of Arabtec Construction, TAV Construction, and

Consolidated Contractors International, which awarded the

AED878mn contract for MEP work to a JV of EFECO, BK Gulf,

and China State. EFECO will play a major role in delivering the

complex mechanical scope of the project. (DFM)

SHUAA elevates its capital markets platform to SunGard –

Shuaa Capital has elevated its capital markets platform to the

global institutional standard with the deployment of keys

solutions from SunGard. SHUAA is set to go live with SunGard’s

Front Arena, an advanced sales & trading system that provides

a reliable platform with fully-integrated access to regional and

global markets. The implementation of SunGard’s Front Arena

will help Shuaa Capital to gain a competitive advantage as its

sales and trading capabilities evolve to higher global standards.

(DFM)

Etihad to meet Alitalia creditors this week – Etihad Airways’

Chief Executive James Hogan said the airline is still talking to

Alitalia’s creditors as part of a due diligence before a possible

investment by the Abu Dhabi airline in the troubled Italian

carrier. Alitalia and Etihad are in the final stages of due diligence

and sources said a deal could involve Etihad buying a 40%

stake for around €300mn ($409mn). Meanwhile, the Chief

Executive of Italy’s largest bank UniCredit said Etihad and

Alitalia’s creditors held talks ahead of a potential investment by

Etihad. However, Hogan said there is still no certainty of a deal,

which depends on how the talks progress between the parties.

(Gulf-Times.com)

IHG signs first Staybridge Suites property in Al Khobar –

InterContinental Hotels Group (IHG) has signed a 20-year

management agreement with Al Khorayef & Sons Company to

operate Staybridge Suites as part of the Alkhorayef Tower

development in Al Khobar, Saudi Arabia. Located on King Fahd

Road, this 189-room property will be the first Staybridge Suites

branded property in Al Khobar, and the third one in Saudi

Arabia. Once ready, Staybridge Suites Al Khobar will be part of

a mixed use development, which will include retail, food and

beverage outlets. Staybridge Suites Al Khobar joins five other

IHG properties operating under three brands in the city,

including InterContinental Hotels & Resorts, Crowne Plaza and

Holiday Inn. (GulfBase.com)

Competition eats into AKS’ profit from sugar production –

Al Khaleej Sugar Company’s (AKS) Managing Director Jamal Al

Ghurair said the company will earn less from sugar production

due to increasing competition from Yemen and Bahrain.

According to a study by the International Sugar Organization,

global capacity to process raw sugar into refined products grew

17mn metric tons since 2000, with about 6.5mn tons coming

from the MENA region. Al Ghurair said that AKS processes

about 1.5mn tons a year although it has capacity for 2.5mn tons.

He further added that the prices are bound to go down due to

intensified competition from two new players, one in Yemen and

one in Bahrain, which will bring down the company’s margins.

(GulfBase.com)

Warba Bank report loss of KD3.7mn in 2013 – Warba Bank

has reported loss of KD3.7mn as compared with KD1.9mn in

2012. Warba Bank’s total assets grew by 81% YoY reaching

KD405.5mn as at the end of 2013. The financing portfolio

increased by 163% YoY to KD218mn, while customers’ deposits

were up by 216% YoY to KD246.8mn as at end of December

2013. (GulfBase.com)

KNPC awards $12bn clean fuel project to consortia – Kuwait

National Petroleum Company (KNPC) has awarded $12bn

project to a consortia led by companies from Britain, the US and

Japan to boost capacity at its oil refineries and make production

more eco-friendly. The $3.8bn Mina Abdullah I Project was

awarded to a consortium led by Britain's Petrofac, the $3.4bn

Mina Abdullah II project to US Fluor-led consortium, while the

$4.8bn Mina Al Ahmadi project went to Japan's JGC Corp-led

consortium. The current production capacity of the refineries of

Mina Al Ahmadi and Mina Abdullah is at around 730,000 bpd,

while the capacity of the third refinery at Shuaiba is 200,000

bpd. The work on this three-part project is expected to

commence in April 2014, which are to be completed in five

years. Once the projects are ready, the capacity of the two

refineries will be raised to 800,000 bpd, while Kuwait plans to

shut down the third refinery. (GulfBase.com)

NCSI: Oman’s industry puts up good performance –

According to data from the National Centre for Statistics and

Information (NCSI), the contribution of manufacturing to Oman’s

GDP has continued to grow during the Eighth Five-Year

Development Plan (2011-2015), and stood at OMR3.3bn (at

Page 4 of 6

5. current prices). Meanwhile, the contribution of industrial

activities including petroleum products and basic materials and

mining stood at OMR5.2bn. On the other hand, there has been

an increase in non-oil industrial exports from OMR2.45bn in

2010 to OMR3.6bn in 2012 respectively, i.e. an increase by

18%. The year 2013 saw around new 20 industrial projects with

investments estimated at more than OMR470mn. Exports of

industrial products from Oman recorded good growth in India,

China and the US. Non-oil exports to India grew from

OMR323mn in 2010 to OMR611.6mn in 2012, to China from

OMR182.6mn to OMR267.4mn and to the US from OMR109mn

to OMR233.2mn. (GulfBase.com)

Topaz unit bags $50mn contract to supply PSVs in Africa –

Renaissance Services, a subsidiary of Topaz Energy & Marine,

has own two platform supply vessel (PSV) contracts worth

$50mn. With this, the company has expanded its West African

operations and brings Topaz’s total contract backlog to

approximately $1.2bn. The contracts are to supply two 3,300

DWT PSVs to international oil companies to support their

offshore production operations. The vessels were commissioned

by Topaz in 2013 as a part of company’s strategy to offer a

technologically advanced fleet of vessels. The vessels are

equipped with the latest technology including dynamic

positioning DP2. Topaz Energy & Marine’s CEO Rene KofodOlsen said that the average age of the company’s total fleet of

93 vessels is now 7.1 years as against an industry average of

around 15 years. (MSM)

ONEIC gets OMR2.1mn hospital contract – The Ministry of

Health has awarded a contract worth OMR2.1mn to Oman

National Engineering & Investment Company (ONEIC) for the

operation & maintenance of equipment and services at Sur

Hospital. This contract also covers other affiliated health units

and administrative offices in the Governorate of South Sharqiya

for the period of three years. (MSM)

AOFS’ BoD recommends 25% dividend for 2013 – Al

Omaniya Financial Services’ (AOFS) board recommended a

25% dividend for 2013. The dividend comprises 17.5% cash and

7.5% compulsory convertible unsecured bonus stock bonds

payable from share premium account. (GulfBase.com)

BKIC’s BoD proposes 30% cash dividend – Bahrain Kuwait

Insurance Company’s (BKIC) board of directors proposed a

cash dividend of 30% (30 fils per share) to its shareholders,

which is subject to approval by the company’s AGM. (Bahrain

Bourse)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.2%

1.0%

0.8%

0.5%

141.9

0.4%

0.2%

129.1

0.0%

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price*

Euro

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

(0.2%)

(0.5%)

Kuwait

(0.8%)

Jan-11

(0.1%)

(0.2%)

Qatar *

(0.4%)

Saudi Arabia

Jun-10

163.3

Source: Bloomberg (*Data as of February 10, 2014)

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,291.46

1.3

1.9

7.1

DJ Industrial

15,994.77

1.2

1.3

(3.5)

20.24

0.8

1.1

4.0

S&P 500

1,819.75

1.1

1.3

(1.5)

108.68

0.0

(0.8)

(1.9)

NASDAQ 100

4,191.05

1.0

1.6

0.3

7.73

1.4

31.6

78.0

STOXX 600

329.52

1.3

1.4

0.4

154.00

(8.9)

(7.4)

21.7

DAX

9,478.77

2.0

1.9

(0.8)

150.25

0.0

0.7

10.1

FTSE 100

6,672.66

1.2

1.5

(1.1)

1.36

(0.1)

0.0

(0.8)

CAC 40

4,283.32

1.1

1.3

(0.3)

102.63

0.4

0.3

(2.5)

Nikkei*

14,718.34

0.0

1.8

(9.7)

GBP

1.65

0.3

0.2

(0.6)

MSCI EM

CHF

1.11

(0.2)

(0.0)

(0.6)

SHANGHAI SE Composite

944.75

1.0

0.8

(5.8)

2,103.67

0.8

2.9

(0.6)

AUD

0.90

1.0

0.9

1.4

HANG SENG

21,962.98

1.8

1.5

(5.8)

USD Index

80.64

(0.0)

(0.1)

RUB

34.74

(0.1)

(0.1)

0.8

BSE SENSEX

20,363.37

0.1

(0.1)

(3.8)

5.7

Bovespa

48,462.79

1.6

0.8

(5.9)

BRL

0.42

0.4

(0.8)

(1.6)

1,341.85

0.4

0.0

(7.0)

Source: Bloomberg (*Market closed on February 11, 2014)

RTS

Source: Bloomberg (*Market closed on February 11, 2014)

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6