(DIYA) Bhumkar Chowk Call Girls Just Call 7001035870 [ Cash on Delivery ] Pun...

22 October Daily Market Report

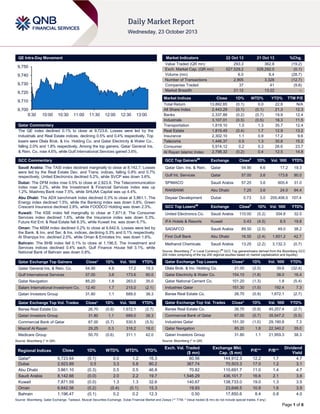

1. QE Intra-Day Movement

Market Indicators

9,750

9,740

9,730

9,720

21 Oct 13

%Chg.

293.3

527,529.2

6.0

2,905

37

21:12

362.8

528,292.0

8.4

3,328

41

13:22

(19.2)

(0.1)

(28.7)

(12.7)

(9.8)

–

Market Indices

9,710

9,700

9:30

22 Oct 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.1% to close at 9,723.6. Losses were led by the

Industrials and Real Estate indices, declining 0.5% and 0.4% respectively. Top

losers were Dlala Brok. & Inv. Holding Co. and Qatar Electricity & Water Co.,

falling 2.0% and 1.8% respectively. Among the top gainers, Qatar General Ins.

& Rein. Co. rose 4.6%, while Gulf International Services gained 3.6%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

13,892.85

2,443.29

2,337.89

3,107.01

1,819.10

1,819.49

2,302.10

1,446.37

5,914.12

2,798.32

(0.1)

(0.1)

(0.2)

(0.5)

1.0

(0.4)

1.1

0.5

0.2

(0.2)

0.0

(0.1)

(0.7)

(0.5)

1.3

1.7

0.9

1.3

0.3

0.4

22.8

21.3

19.9

18.3

35.7

12.9

17.2

35.8

26.6

12.5

N/A

12.3

12.4

11.5

12.4

13.2

9.6

15.2

23.7

14.8

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index declined marginally to close at 8,142.7. Losses

were led by the Real Estate Dev. and Trans. indices, falling 0.8% and 0.7%

respectively. United Electronics declined 5.2%, while SVCP was down 3.6%.

Qatar Gen. Ins. & Rein.

1D%

Qatar

54.90

4.6

17.2

19.3

Gulf Int. Services

Qatar

57.00

3.6

173.6

90.0

Dubai: The DFM index rose 0.5% to close at 2,923.9. The Telecommunication

index rose 2.2%, while the Investment & Financial Services index was up

1.2%. Mashreq Bank rose 7.5%, while SHUAA Capital was up 4.4%.

SPIMACO

Saudi Arabia

57.25

3.6

605.4

31.0

RAKBANK

Abu Dhabi

7.25

3.6

24.0

94.4

Abu Dhabi: The ADX benchmark index declined 0.3% to close at 3,861.1. The

Energy index declined 1.5%, while the Banking index was down 0.8%. Green

Crescent Insurance declined 2.8%, while FOODCO Holding was down 2.3%.

Deyaar Development

Dubai

0.73

3.0

GCC Top Losers

Exchange

Close

1D% Vol. ‘000

Kuwait: The KSE index fell marginally to close at 7,871.6. The Consumer

Services index declined 1.6%, while the Insurance index was down 0.3%.

Future Kid Ent. & Real Estate fell 8.3%, while Kuwait Ins. was down 6.7%.

United Electronics Co.

Saudi Arabia

110.00

(5.2)

354.8

32.5

IFA Hotels & Resorts

Kuwait

0.43

(4.5)

8.5

19.8

Oman: The MSM index declined 0.2% to close at 6,642.6. Losses were led by

the Bank. & Inv. and Ser. & Ins. indices, declining 0.3% and 0.1% respectively.

Al Sharqiya Inv. declined 2.0%, while Oman & Emirates Inv. was down 1.6%.

SADAFCO

Saudi Arabia

89.50

(2.5)

49.0

38.2

First Gulf Bank

Abu Dhabi

16.55

(2.4)

1,651.2

42.7

Methanol Chemicals

Saudi Arabia

13.25

(2.2)

3,132.3

(0.7)

Bahrain: The BHB index fell 0.1% to close at 1,196.5. The Investment and

Services indices declined 0.4% each. Gulf Finance House fell 3.1%, while

National Bank of Bahrain was down 0.8%.

Qatar Exchange Top Gainers

Close*

Qatar General Ins. & Rein. Co.

54.90

##

#

Vol. ‘000

YTD%

205,406.5 107.4

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

4.6

17.2

19.3

Dlala Brok. & Inv. Holding Co.

21.00

(2.0)

39.6

(32.4)

90.0

Qatar Electricity & Water Co.

154.10

(1.8)

38.0

16.4

(5.4)

Gulf International Services

57.00

3.6

173.6

Qatar Navigation

85.20

1.8

263.0

35.0

Qatar National Cement Co.

101.20

(1.3)

1.8

Salam International Investment Co.

12.40

1.7

215.0

(2.1)

Industries Qatar

151.30

(1.0)

192.4

7.3

Qatari Investors Group

31.80

1.1

689.0

38.3

Barwa Real Estate Co.

26.70

(0.9)

1,672.1

(2.7)

Qatar Exchange Top Vol. Trades

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

YTD%

Barwa Real Estate Co.

26.70

(0.9)

1,672.1

(2.7)

Barwa Real Estate Co.

26.70

(0.9)

45,257.4

(2.7)

Qatari Investors Group

31.80

1.1

689.0

38.3

Commercial Bank of Qatar

67.00

(0.7)

35,547.2

(5.5)

Commercial Bank of Qatar

67.00

(0.7)

530.5

(5.5)

Industries Qatar

151.30

(1.0)

29,190.8

7.3

Masraf Al Rayan

29.25

0.3

318.2

18.0

Qatar Navigation

85.20

1.8

22,340.2

35.0

Medicare Group

50.70

(0.6)

311.1

42.0

Qatari Investors Group

31.80

1.1

21,959.3

38.3

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

9,723.64

2,923.89

3,861.10

8,142.66

7,871.59

6,642.56

1,196.47

(0.1)

0.5

(0.3)

(0.0)

(0.0)

(0.2)

(0.1)

0.0

3.3

0.5

2.0

1.3

(0.4)

0.2

1.2

5.8

0.5

2.2

1.3

(0.1)

0.2

16.3

80.2

46.8

19.7

32.6

15.3

12.3

Exch. Val. Traded

($ mn)

80.56

367.74

70.82

1,546.29

140.67

19.93

0.50

Exchange Mkt.

Cap. ($ mn)

144,912.3

70,503.3

110,691.7

436,101.7

138,733.0

23,648.5

17,850.6

P/E**

P/B**

12.2

17.0

11.0

16.6

19.0

10.9

8.4

1.7

1.2

1.4

2.1

1.3

1.6

0.8

Dividend

Yield

4.7

3.1

4.7

3.6

3.5

3.9

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index declined 0.1% to close at 9,723.6. The Industrials

and Real Estate indices led the losses. The index declined on

the back of selling pressure from Qatari shareholders despite

buying support from non-Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

58.90%

63.07%

(12,217,439.56)

Non-Qatari

Dlala Brok. & Inv. Holding Co. and Qatar Electricity & Water Co.

were the top losers, falling 2.0% and 1.8% respectively. Among

the top gainers, Qatar General Ins. & Rein. Co. rose 4.6%, while

Gulf International Services gained 3.6%.

Buy %*

41.09%

36.92%

12,217,439.56

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Tuesday declined by 28.7% to

6.0mn from 8.4mn on Monday. Further, as compared to the 30day moving average of 6.9mn, volume for the day was 13.3%

lower. Barwa Real Estate Co. and Qatari Investors Group were

the most active stocks, contributing 27.8% and 11.5% to the total

volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Revenue

(mn) 3Q2013

% Change

YoY

Operating Profit

(mn) 3Q2013

% Change

YoY

Net Profit (mn)

3Q2013

% Change

YoY

SR

–

–

21.9

13.4%

18.6

9.8%

Saudi Arabia

SR

–

–

-15.3

N/A

-13.1

N/A

Saudi Arabia

SR

–

–

35.2

-0.6%

37.0

27.1%

Saudi Arabia

SR

–

–

33.7

-5.1%

22.0

-12.5%

Saudi Arabia

SR

–

–

64.1

-15.4%

65.5

-7.7%

Saudi Arabia

SR

–

–

44.3

-11.5%

17.6

8.5%

Saudi Arabia

SR

–

–

18.0

-21.7%

17.5

-23.2%

Saudi Arabia

SR

–

–

238.0

8.7%

229.0

9.6%

Saudi Arabia

SR

–

–

957.2

78.2%

864.8

98.5%

Abu Dhabi

AED

51.5

107.0%

–

–

7.9

3.1%

Market

Al Khaleej Training &

Education

Saudi Public Transport Co.

(SAPTCO)

National Gas &

Industrialization Co.

(GASCO)

Methanol Chemicals Co.

(MCC)

Al Abdullatif Industrial

Investment Co. (AIIC)

Saudi Arabian Amiantit Co.

(SAAC)

Saudi Vitrified Clay Pipe Co.

(SVCP)

Saudi Cement Co. (SCC)

Yanbu National

Petrochemicals Co.

(YANSAB)

Insurance House (IH)*

Currency

Saudi Arabia

Source: Company data, DFM, ADX, MSM (* Results for nine months ended September 30, 2013)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

10/22

US

Bureau of Labor Stat.

Change in Private Payrolls

September

126K

180K

161K

10/22

US

Bureau of Labor Stat.

Unemployment Rate

September

7.20%

7.30%

7.30%

10/22

US

Bureau of Labor Stat.

Average Hourly Earnings MoM

September

0.10%

0.20%

0.30%

10/22

US

Bureau of Labor Stat.

Average Hourly Earnings YoY

September

2.10%

2.10%

2.30%

10/22

US

Bureau of Labor Stat.

Underemployment Rate

September

13.60%

–

13.70%

10/22

US

Bureau of Labor Stat.

Change in Manufact. Payrolls

September

10/22

US

US Census Bureau

Construction Spending MoM

August

10/22

US

Richmond Fed

Richmond Fed Manufact. Index

October

2K

5K

13K

0.60%

0.40%

1.40%

1

0

0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 6

3. News

Qatar

Qatari banking sector monthly update for September 2013 –

Customer deposits grew by 3.2% MoM (+14.8% YTD), while

loans were flattish MoM basis (+9.0% YTD) in September 2013.

However, the banking sector’s loan-to-deposit ratio (LDR) fell to

106% in September 2013 versus 109% in August 2013. (QCB)

QIIK 3Q2013 net income up 12.5% QoQ – QIIK (Qatar

International Islamic Bank) posted a net profit of QR202.9mn in

3Q2013 vs. our estimate of QR187.9mn and Bloomberg

consensus estimate of QR185.0mn. QIIK posted QR180.3mn in

2Q2013, implying a growth of 12.5% QoQ. The QoQ growth in

earnings was mainly due to higher income from share of results

from associates, lower foreign exchange loss on translation of

investment in associates and lower provisions vs. our estimates.

The loan book and deposits expanded on a QoQ and YTD

basis. QIIK’s loan book grew by 9.3% QoQ (+44.5% YTD), while

total deposits (URIA & current accounts) grew by 12.9% QoQ

(+24.9% YTD). However, the improved loan book did not make

a significant impact on income from financing activities, which

expanded by only 1.9% (QIIK has been aggressively targeting

the public sector in the last few quarters). On the other hand,

share of unrestricted investment account holders (URIA)

increased by 13.0% QoQ. Hence, net financing income declined

by 2.3% QoQ. Furthermore, income from investing activities

declined by 18.8% QoQ. We maintain our estimates and

reiterate our price target of QR57.18. For 2013 and 2014, we

expect QIIK to post earnings of QR729mn and QR782mn,

respectively. We feel the bank will increase DPS to QR3.75 for

2013 (QR3.50 DPS for the last two years). Going forward, we

expect the dividend payout ratio to be in the vicinity of 75%.

Valuation appears fair. We believe the bank is fairly valued

relative to its Qatari peers. The bank trades on P/E and P/B

multiples of 11.8x and 1.6x on our 2013 estimates. (QNBFS

Research, QE)

GISS reports net profit of QR166.1mn in 3Q2013 – Gulf

International Services (GISS) reported a net profit of

QR166.1mn in 3Q2013 up 5.6% and 36.4% QoQ and YoY,

respectively. Revenue rose by 1.5% QoQ (+30.1% YoY) to

QR575.2mn in 3Q2013. EPS amounted to QR3.09 for the nine

months ended September 30, 2013 as compared to QR2.14 for

the corresponding period in 2012. (QE)

DOHI reports net profit of QR2.9mn in 3Q2013 – Doha

Insurance (DOHI) has reported a net profit (attributable to

shareholders) of QR2.9mn in 3Q2013, reflecting a decrease of

80.2% QoQ (+85.6% YoY). Net premiums fell by 43.1% QoQ (7.4% YoY) to QR19.1mn in 3Q2013. Earnings per Share (EPS)

amounted to QR1.52 for the nine months ended September 30,

2013 as compared to QR1.67 for the corresponding period in

2012. (QE)

SIIS reports net profit of QR92.6mn in 3Q2013 – Salam

International Company (SIIS) has reported a net profit

(attributable to equity holders) of QR92.6mn in 3Q2013 as

compared to QR2.8mn in 2Q2013. Operating income rose by

17.8% QoQ to QR500.4mn in 3Q2013. Earnings per Share

(EPS) amounted to QR0.94 for the nine months ended

September 30, 2013 as compared to QR0.54 for the

corresponding period in 2012. (QE)

DHBK clarifies regarding issuance of Tier 1 capital notes –

Doha Bank has clarified to its shareholders that the

recommendation that will be submitted to the extraordinary

general assembly by the board is not intended to increase the

number of the bank's current capital shares through the

issuance of new shares, but is intended to strengthen the bank's

Tier 1 capital through the issuance of notes in Qatar of a special

nature that qualifies those bonds to be subordinated Tier 1

capital notes in order to strengthen the bank's capital adequacy

ratio. Therefore, the issuance of these notes will not entail

offering any new shares for subscription, and Doha Bank's

capital will remain at its current level of 258,372,252 and any

dividend distributions will be for the shares of the current capital

of the bank. (QE)

Qatar to launch tourism strategy by December – The Qatar

Tourism Authority (QTA) is all set to launch a comprehensive

strategy before the end of this year, in a move to attract more

foreign visitors to the state. QTA’s Chairman Issa bin Mohamed

al- Mohannadi said details of “the Qatar Tourism Sector Strategy

2030” will be disclosed either in November or December. AlMohannadi noted that the strategy will include benchmarking

and involving all its local stakeholders who have been working to

develop destinations in Qatar for both domestic and international

tourists. During the Eid al-Adha holidays, QTA recorded a 1617% rise in tourist arrivals from the GCC countries as compared

to the previous year, while the number of tourists outside the

GCC region grew 7%. Hotels in Doha saw their occupancy rates

rising to about 90%. He also said that QTA wants to contribute

significantly to Qatar’s GDP, rising from 0.7-0.8% share in 2012,

to a 2.9-3.3% by 2030. QTA also expects tourism-related jobs to

grow from 19,000 in 2012 to 127,000 by 2030. (Gulf-Times.com)

Ashghal: 75% work on F-Ring Road completed – The Public

Works Authority (Ashghal) has said 75% of the work on F-Ring

Road has been completed and the contractors are now working

toward delivering the project by 2Q2014. The road is part of the

highways project, which will link south Doha to Hamad

International Airport, and connect Mesaimeer Road and the

main road leading to Al Wakrah. Executed at a cost of

QR837mn, the F-Ring Road project will feature an 8.7 kilometer

highway with 3-4 lanes in each direction. (Gulf-Times.com)

Hamad airport to open partially in November – The Hamad

International Airport will be partially opened by the end of next

month. The New Doha International Airport Steering Committee

said the plan for the initial opening includes beginning the air

cargo service to and from Doha. (Peninsula Qatar)

Qafac partners with SAP to boost key operational

processes – Qatar Fuel Additives Company (Qafac) announced

that it has partnered with business software company SAP to

enhance its key operational processes and its overall

sustainability performance. Qafac said a series of solutions

created by SAP will give Qafac an edge in contributing to the

Qatar National Vision 2030 and its goal of becoming the world’s

top five methanol producers by 2020. (Gulf-Times.com)

WDAM to disclose its 3Q2013 results on October 30 –

Widam Food Company (WDAM) will disclose its quarterly

financial results for the period ending September 30, 2013 on

October 30, 2013. (QE)

ERES to hold its AGM on November 10 – Ezdan Holding

Group (ERES) will hold its AGM on November 10, 2013, to

discuss the recommendation of its board of directors to enter

into a partnership with the Sak Holding Group for the

development of land owned by Ezdan Holding and delegate the

board to complete the procedures necessary to do so. (QE)

International

US shutdown cost 120,000 jobs – US President Barack

Obama’s Chief Economic Adviser Jason Furman said the partial

government shutdown this month trimmed 0.25% from the

economic growth for 4Q2013 and cost 120,000 jobs in October.

Page 3 of 6

4. He said an analysis of daily and weekly economic data through

October 12 showed weakness in areas such as retail sales,

economic confidence and mortgage applications, some of which

was directly related to the 16-day shutdown. (Bloomberg)

Osborne: Growth alone would not fix British deficit – British

Finance Minister George Osborne vowed to stick to the path of

austerity, saying the economic recovery on its own would not be

enough to fix the budget deficit, since the causes of overspending still need to be addressed. Osborne warned that

growth alone would not fix the fundamental problems in Britain's

public finances and the government would have to take very

difficult decisions. (Reuters)

PBoC may tighten cash supply as China’s house prices fuel

inflation fears – Chinese authorities indicated concerns that

ample credit could fuel inflation since a recent report showed

house prices jumped the most in nearly three years, with

double-digit gains in major cities. A policy adviser to the

People's Bank of China (PBoC) said the authority may tighten

cash conditions in the financial system to address inflation risks.

(Reuters)

Regional

APICORP to buy 10% equity stake in EMethanex – Arab

Petroleum Investments Corporation (APICORP) will buy 10%

equity stake in its JV, “Egyptian Methanex Methanol Company

(EMethanex)” from its partner, Methanex Corporation. This

stake worth $110mn will increase APICORP's ownership in the

JV to 17%. Methanex will remain the operator and majority

shareholder of EMethanex with around 50% ownership. The

remaining 33% interest is held by several Egyptian government

shareholders. The partner companies expect the stake sale to

be finalized by the end of 2013. (Bloomberg)

APC obtains contract from PDO to supply welded steel

pipes– The Arabian Pipes Company (APC) has obtained a

three-year contract worth SR400-SR500mn from Petroleum

Development of Oman (PDO) for supply of welded steel pipes.

This contract includes manufacture, coating and supply of steel

pipes designed for high pressure flow lines and critical

applications. APC expects to begin the production of these pipes

in 1Q2014 and supply continuously until the end of 2016. The

financial impact of this contract will be seen starting from

1Q2014 up to the end of the project. (Tadawul)

Bank AlBilad buys SR410mn building from Ajlan Real

Estate – Bank AlBilad has purchased a building in Riyadh for

SR410mn from Ajlan Real Estate Company. This new building

will be the new headquarters of the bank. (Tadawul)

Itqan Capital eyes $200mn for its private equity fund –

Saudi-based investment firm Itqan Capital’s CEO Adil Dahlawi

said the firm is eyeing up to $200mn for the fund that it plans to

launch along with Bahrain-based school consultancy firm, D3

Consultants in 2014. Dahlawi stated the firm has entered into a

MoU with D3 Consultants to launch a private equity fund that will

focus on investment in the fast-growing education sector in the

GCC region. (GulfBase.com)

Dubai switches on first solar plant, plans to build second

plant – Dubai has commissioned its first solar power plant

producing 13 megawatt (MW) and is planning to build a second,

bigger photovoltaic plant to diversify the energy supply in the

UAE. US-based First Solar has built this facility worth AED120AED130mn. The Dubai Electricity & Water Authority’s (DEWA)

CEO Saeed Al Tayer said that this is the first part of Dubai’s

plan to develop a solar park with 1,000 MW of power by 2030.

He added that DEWA is also planning to invite bids over the

next six months to have a private partner for its second 100 MW

solar project expected to cost AED700-800mn. DEWA expects

to complete the second plant in three years. (Bloomberg)

Dubai Customs to increase its customs declaration

clearance capacity by 200% – Dubai Customs is expecting to

increase its clearance capacity of customs declarations by

around 200% soon. Dubai Customs has recorded 6.3mn

transactions in 2012 and expects to reach 6.8mn by the end of

2013. The department is currently working on implementing a

smart technology, which will boost its capacity to around 18mn

transactions. These smart services are becoming widely

accepted by the customers. (GulfBase.com)

du telecom appoints new CFO – Emirates Integrated

Telecommunications Company (du telecom) has appointed

Amer Kazim as the new CFO for the company. Kazim is

expected to join the company from December 2013. He brings

with him an experience of 18 years in the financial sector. Kazim

has joined from the Dubai Airports Company, where he was

working as Senior Vice President Group Services for the last

four years. The current CFO Mark Shuttleworth will remain in his

position till the end of 1Q2014. (DFM)

EIT plans to sell stake in Tunisie Telecom, Axiom Telecom –

Emirates International Telecommunications (EIT) is planning to

sell its 35% stake in Tunisia-based Tunisie Telecom and 26%

stake in Dubai-based Axiom Telecom. This is as part of a

strategy by all state-linked companies to sell their assets to

repay the Emirate's debt pile. JP Morgan Chase has estimated

that these sales could generate $1bn in total. (Reuters)

NBQ reports AED90.7mn net profit in 3Q2013 – The National

Bank of Umm Al Qaiwain (NBQ) has reported a net profit of

AED90.7mn in 3Q2013, indicating an increase of 5.3% YoY. Net

interest income decreased 9.4% YoY to AED102.9mn in

3Q2013. EPS amounted to AED0.17 for the nine months ended

September 30, 2013 as compared to AED0.15 for the

corresponding period in 2012. Total assets stood at AED12.2bn

as on September 30, 2013, declining 0.1% YTD. Loans &

advances rose by 0.2% YTD to AED6.8bn, while customer

deposits declined 0.9% YTD to AED7.2bn. (ADX)

Abu Dhabi’s GBC Index stood at 57 points in 2Q2013 –

According to a report by the Abu Dhabi Department of Economic

Development, Abu Dhabi’s General Business Climate Index

(GBC Index) has gained two points to reach 57 points in

2Q2013 as compared to 55 points in 1Q2013. This reflects the

continued optimistic outlook of various economic establishments

on the performance of Abu Dhabi’s economy during 1H2013.

(Bloomberg)

Dana Gas begins arbitration proceedings on Kurdish

Contract – Dana Gas has began arbitration proceedings in

London on rights and money owed from an oil development

contract it signed with the Kurdistan regional government of Iraq

in 2007. Dana Gas said the proceedings at the London Court of

International Arbitration relate to outstanding receivables owed

by the Kurdish government. The company, along with majority

shareholder Crescent Petroleum Company and subsidiary Pearl

Petroleum Company, also filed the case to clarify the group’s

development and marketing rights of the Khor Mor and

Chemchemal fields in Kurdistan. (Bloomberg)

Fitch assigns ratings to Al Hilal Bank's certificates – Fitch

Ratings has assigned Al Hilal Bank's $2.5bn trust certificate

issuance program a final long-term rating of “A+” and a final

short-term rating of “F1”. Fitch has also assigned Al Hilal's

$500mn senior unsecured fixed rate certificates (sukuk) issued

under the program a long-term rating of “A+”. (Bloomberg)

Page 4 of 6

5. Mubadala provides $900mn to Verno Capital for Russian

private equity – Mubadala Development Company has

provided Verno Capital with $900mn to help the company invest

in Russian private equity. (Bloomberg)

Ahli Bank Oman reports OMR18mn net profit for 9M2013 –

Ahli Bank Oman has a net profit of OMR18mn for the nine

months ended on September 30, 2013, reflecting an increase of

6% YoY. The bank’s total assets at the end of September 30,

2013 rose by 23% YoY to OMR1.3bn. Loans & advances

increased by 19% YoY to OMR1.06bn, while customer deposits

stood at OMR937mn. (Bloomberg)

Ithmaar Bank announces key appointments – Ithmaar Bank

has appointed Abdul Hakeem Al Mutawa as the new General

Manager Head of Retail & Private Banking, Abdul Rahman Al

Shaikh as the new General Manager Head of Banking

Operations, IT & Administration and Taimour Raouf as the new

Senior

Manager Head

of

Marketing

&

Corporate

Communications. (Bahrain Bourse)

CBB’s Sukuk Al-Salam securities oversubscribed by 144%

– The Central Bank of Bahrain’s (CBB) monthly issue of Sukuk

Al-Salam Islamic securities worth BHD36mn has been

oversubscribed by 144%. This issue carries a maturity of 91

days, which will mature on January 22, 2014. The expected

return on the issue is 0.85%, which remains unchanged over the

previous issue. (GulfBase.com)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

150.0

0.5%

0.6%

140.0

139.7

130.0

0.3%

128.0

0.0%

(0.0%)

(0.3%)

100.0

(0.1%)

(0.0%)

(0.1%)

(0.2%)

Mar-11

QE Index

Oct-11

May-12 Dec-12

S&P Pan Arab

Jul-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Oman

Aug-10

Bahrain

Jan-10

Kuwait

80.0

Qatar

(0.6%)

Saudi Arabia

90.0

(0.3%)

Dubai

116.5

110.0

Abu Dhabi

120.0

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,340.15

1.8

1.8

(20.0)

DJ Industrial

15,467.66

0.5

0.4

18.0

22.70

2.2

3.5

(25.2)

S&P 500

1,754.67

0.6

0.6

23.0

109.97

0.3

0.0

(1.0)

NASDAQ 100

3,929.57

0.2

0.4

30.1

3.70

(2.1)

(0.4)

8.0

320.97

0.4

0.8

14.8

115.25

0.0

(0.2)

28.8

DAX

8,947.46

0.9

0.9

17.5

150.88

(1.0)

(1.0)

(12.8)

FTSE 100

6,695.66

0.6

1.1

13.5

4,295.43

0.4

0.2

18.0

14,713.25

0.1

1.0

41.5

STOXX 600

Euro

1.38

0.7

0.7

4.5

Yen

98.14

(0.1)

0.4

13.1

Nikkei

GBP

1.62

0.6

0.4

(0.1)

MSCI EM

1,044.66

0.2

0.2

(1.0)

CHF

1.12

0.8

0.8

2.3

SHANGHAI SE Composite

2,210.65

(0.8)

0.8

(2.6)

AUD

0.97

0.6

0.3

(6.6)

HANG SENG

23,315.99

(0.5)

(0.1)

2.9

USD Index

79.23

(0.6)

(0.5)

(0.7)

BSE SENSEX

20,864.97

(0.1)

(0.1)

7.4

RUB

31.68

(0.8)

(0.4)

3.8

Bovespa

56,460.38

0.7

2.0

(7.4)

BRL

0.46

0.0

(0.1)

(5.6)

1,518.54

0.3

0.1

(0.6)

Source: Bloomberg

CAC 40

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6