Сучасний страховий риноквключає:

Перестрахування Співстрахування

Цивільний кодекс України від 16 січня 2003 р.,

Закон України «Про страхування» від 4 жовтня 2001 р. та інші нормативно– правові акти.

3.

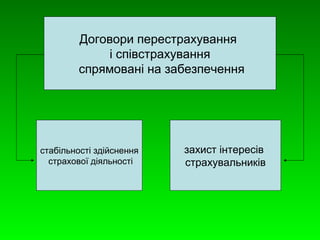

Договори перестрахування

іспівстрахування

спрямовані на забезпечення

стабільності здійснення

страхової діяльності

захист інтересів

страхувальників

4.

Хоча такі договориі є

складнішими

конструкціями, ніж

звичайні договори

страхування, але в

даному випадку така

складність компенсується

більшою надійністю.

5.

Співстрахування – це:

спосіб розподілу ризику між двома та

більше страховиками шляхом

покладання на кожного із них

заздалегідь обумовленої частки

можливих збитків страхувальника.

6.

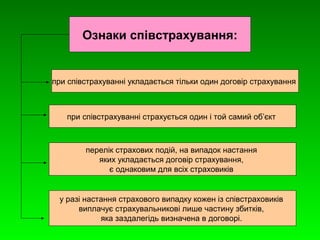

Ознаки співстрахування:

приспівстрахуванні укладається тільки один договір страхування

при співстрахуванні страхується один і той самий об’єкт

перелік страхових подій, на випадок настання

яких укладається договір страхування,

є однаковим для всіх страховиків

у разі настання страхового випадку кожен із співстраховиків

виплачує страхувальникові лише частину збитків,

яка заздалегідь визначена в договорі.

7.

Страховик, котрий бере

участь у страхуванні в

меншій частці,

підпорядковується

умовам, узгодженим

страховиком, що має

більшу частку.

8.

Можлива ситуація, колиодин і той самий предмет

страхування буде застрахований у кількох

страховиків за різними договорами.

9.

Перевага перестрахування полягаєв тому, що

страховик, який перестраховує прийняті на

себе ризики, створює додаткові гарантії своєї

фінансової стійкості. Відповідно, страхувальник

отримує додаткову впевненість у повному і

вчасному відшкодуванні збитків.

10.

За

договором перестрахування

страховик, який уклав договір

страхування, страхує в іншого

страховика (перестраховика)

ризик виконання частини

своїх обов'язків перед

страхувальником.

Страховик, який уклав договір

перестрахування,

залишається відповідальним

перед страхувальником у

повному обсязі відповідно до

договору страхування.

11.

Відповідно до ст.12 Закону «Про

страхування» перестрахування - це

• страхування одним

страховиком

(цедентом,

перестрахувальником)

на визначених

договором умовах

ризику виконання

частини своїх

обов'язків перед

страхувальником у

іншого страховика

(перестраховика)

резидента або

нерезидента, який має

статус страховика або

перестраховика, згідно

із законодавством

країни, в якій він

зареєстрований.

12.

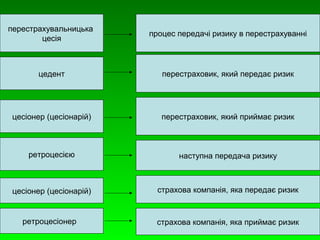

перестрахувальницька

цесія процеспередачі ризику в перестрахуванні

цедент перестраховик, який передає ризик

перестраховик, цесіонер (цесіонарій) який приймає ризик

наступна передача ризику

страхова компанія, яка передає ризик

страхова компанія, яка приймає ризик

ретроцесією

цесіонер (цесіонарій)

ретроцесіонер

13.

Види перестрахування

вхіднеквотне непропорційне факультативне

договір

перестрахування,

який

укладається

з метою прийняти

на себе

відповідальність,

повну або

часткову,

іншої страхової

компанії.

форма

пропорційного

перестрахування,

за якої

перестраховик

передає

перестрахувальнику

певну частину

від усіх

своїх ризиків

перестрахування,

за якого

перестраховик

несе відповідальність

за збитки,

які перевищують

певну суму

метод

перестрахування,

за якого

перестраховику

і

перестрахувальнику

надається

можливість

оцінки ризиків,

які можуть бути

передані в

перестрахування

повністю

або частково

14.

Інколи

співстрахування

розглядаєтьсяяк

окремий випадок

перестрахування,

коли одночасно

кілька страховиків

за взаємним

узгодженням

приймають чи

передають на

страхування

великі ризики.

15.

Хоча з юридичногопогляду

співстрахування та страхування різні,

за своєю економічною сутністю вони

дуже схожі :

здійснюється розподіл страхових внесків та

страхових виплат

наявна співучасть у преміях та

страхових ризиках

координуються страхові фонди різних страховиків

(перестраховиків), які одночасно беруть участь в

одному і тому ж страхуванні

16.

З юридичного боку:

Співстрахування Перестрахування

Кількість договорів

страхування

У договорі

зазначаються:

один договір

два договори:

основний договір

та договір

перестрахування

всі страховики

та їх частки

у страховій виплаті

страховик не

зобов’язаний

повідомляти

страхувальника

про укладання

договору

перестрахування

17.

Перестрахування пішло наспад

• За I півріччя 2012 року обсяги перестрахування впали в

5,7 рази. Трапилося це в основному через подорожчання

послуг перестрахування і відсутність довіри між

страховиками.

• Страховий ринок в I півріччі зміг вирости по чистим

премій відразу на 17,95% - до 8,98 млрд гривень, проте в

цілому ринок продемонстрував падіння.

• Обсяг ризиків, переданих перестраховикам-резидентам,

зменшився в 5,68 рази - до 604,2 млн гривень. Премії

нерезидентам, незважаючи на необхідність проходження

складної процедури реєстрації договорів

перестрахування, у I півріччі виросли на 25,2% - до 731,9

млн гривень.