Downloaded 23 times

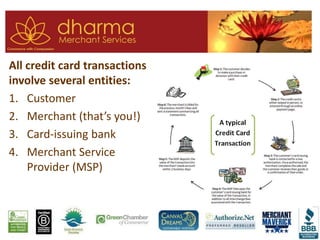

The document serves as a guide for nonprofits on navigating payment processing, detailing essential concepts like merchant accounts, payment gateways, and credit card pricing. It discusses the roles of key players in transactions, including merchant service providers and card-issuing banks, and outlines both online and in-person payment acceptance methods. Additionally, it emphasizes the importance of understanding pricing structures to avoid common traps and maximize savings.