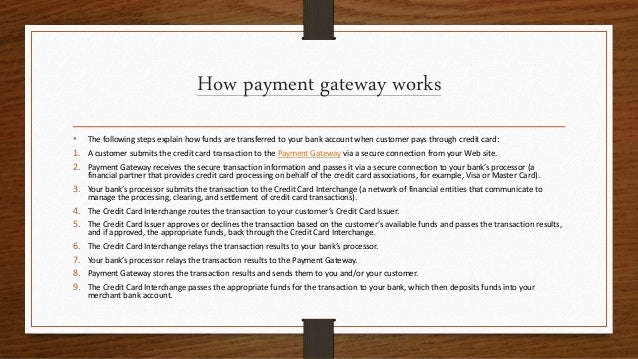

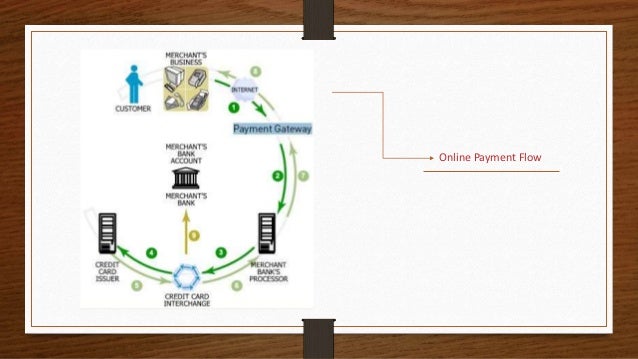

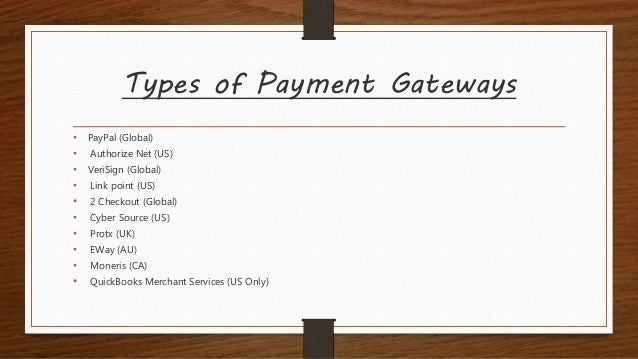

Payment gateways are interfaces that allow merchants to accept electronic payments from customers. They connect online stores and point-of-sale terminals to payment processors, who transfer funds from customers' bank accounts or credit cards to merchants' bank accounts. Payment gateways come in different types depending on their technical requirements and may charge merchants various fees for their services. They enable secure transactions between customers and merchants in both online and physical stores.

![White label payment gateway

some payment gateways offer white label services, which

allow payment service providers, e-commerce platforms, ISOs, resellers,

or acquiring banks to fully brand the payment gateway’s technology as

their own.[4] This means PSPs or other third parties can own the end-

to-end user experience without bringing payments operations—and

additional risk management and compliance responsibility](https://image.slidesharecdn.com/paymentgateway-220114091731/95/Payment-gateway-9-638.jpg)