Recommended

Recommended

More Related Content

Similar to Google 2016 annual report-target corporate to get all the necessary .pdf

Similar to Google 2016 annual report-target corporate to get all the necessary .pdf (20)

More from RITU1ARORA

More from RITU1ARORA (20)

Recently uploaded

Recently uploaded (20)

Google 2016 annual report-target corporate to get all the necessary .pdf

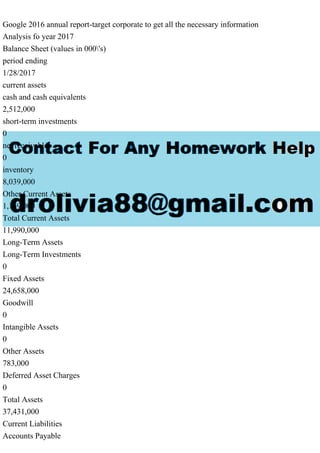

- 1. Google 2016 annual report-target corporate to get all the necessary information Analysis fo year 2017 Balance Sheet (values in 000's) period ending 1/28/2017 current assets cash and cash equivalents 2,512,000 short-term investments 0 net receivables 0 inventory 8,039,000 Other Current Assets 1,169,000 Total Current Assets 11,990,000 Long-Term Assets Long-Term Investments 0 Fixed Assets 24,658,000 Goodwill 0 Intangible Assets 0 Other Assets 783,000 Deferred Asset Charges 0 Total Assets 37,431,000 Current Liabilities Accounts Payable

- 2. 10,989,000 Short-Term Debt / Current Portion of Long-Term Debt 1,718,000 Other Current Liabilities 1,000 Total Current Liabilities 12,708,000 Long-Term Debt 11,031,000 11,945,000 Other Liabilities 1,878,000 Deferred Liability Charges 861,000 Misc. Stocks 0 Minority Interest 0 Total Liabilities 26,478,000 Stock Holders Equity Common Stocks 46,000 Capital Surplus 5,661,000 Retained Earnings 5,884,000 Treasury Stock 0 Other Equity ($638,000) Total Equity 10,953,000 Total Liabilities & Equity 37,431,000 Cash flow (values in000's)

- 3. period ending 1/28/2017 Net Income 2,737,000 Cash Flows-Operating Activities Depreciation 2,298,000 Net Income Adjustments 508,000 Changes in Operating Activities Accounts Receivable 0 Changes in Inventories 293,000 Other Operating Activities 36,000 Liabilities ($543,000) Net Cash Flow-Operating 5,436,000 Cash Flows-Investing Activities Capital Expenditures ($1,547,000) Investments 28,000 Other Investing Activities 46,000 Net Cash Flows-Investing $1,473,000) Cash Flows-Financing Activities Sale and Purchase of Stock ($3,485,000) Net Borrowings ($664,000) Other Financing Activities 0

- 4. Net Cash Flows-Financing ($5,497,000) Effect of Exchange Rate 0 Net Cash Flow ($1,534,000) IV. Adjusting Entries: A. Explain the type of depreciation method Target Corporation uses and why they use this method. B. Identify an example of an adjusting entry (other than depreciation), such as prepaid expenses, supplies, or unearned revenue, and whether or not Target Corporation has this account listed on the balance sheet. You could consider why this might not be listed. VI. Communication: For this part of the assessment, you will prepare memorandums to upper management addressing certain scenarios or situations. A. As the controller of Target Corporation, compose a memo to the CEO addressing the advantages and disadvantages of transitioning from GAAP to IFRS. B. As the controller of Target Corporation, compose a memo to the CEO addressing the following scenario: Your biggest customer has just gone bankrupt, and you must inform the CEO how this will affect your accounts receivable. Assume that the accounts receivable balance is at least $100,000. When writing your paper considers the following: A company may use several different depreciation methods or just one. This information will be disclosed in the notes. If the company has not explained why they use the method, you will want to consider the pros and cons of the method and use the information you know about the method to provide why you think they chose the method. For the adjusting entry think about gift cards (accrued liabilities) and prepaid (accrued expenses), etc. Many items are adjusted based on revenue and expense recognition principles. Transitioning from GAAP to IFRS does have advantages and disadvantages. When discussing Accounts Receivable make sure you do consider whether Target Corporation uses the direct write-off method, or an allowance? How would handling this scenario be different based on the method used? What accounts would be affected based on the method used to account for bad debt? Please do make sure you fully address each critical element with appropriate detail and that you defend your content in your paper with scholarly sources. Support your arguments with at least three peer-reviewed sources cited in APA format. period ending

- 5. 1/28/2017 current assets cash and cash equivalents 2,512,000 short-term investments 0 net receivables 0 inventory 8,039,000 Other Current Assets 1,169,000 Total Current Assets 11,990,000 Long-Term Assets Long-Term Investments 0 Fixed Assets 24,658,000 Goodwill 0 Intangible Assets 0 Other Assets 783,000 Deferred Asset Charges 0 Total Assets 37,431,000 Current Liabilities Accounts Payable 10,989,000 Short-Term Debt / Current Portion of Long-Term Debt 1,718,000 Other Current Liabilities 1,000

- 6. Total Current Liabilities 12,708,000 Long-Term Debt 11,031,000 11,945,000 Other Liabilities 1,878,000 Deferred Liability Charges 861,000 Misc. Stocks 0 Minority Interest 0 Total Liabilities 26,478,000 Stock Holders Equity Common Stocks 46,000 Capital Surplus 5,661,000 Retained Earnings 5,884,000 Treasury Stock 0 Other Equity ($638,000) Total Equity 10,953,000 Total Liabilities & Equity 37,431,000 Solution IV: Adjusting Entries: A. Method of Depreciation: The company is using the cost model of depreciation in which the assets are shown at cost less any accumulated depreciation (i.e. net balance is shown in the

- 7. balance sheet) as per the Accounting Principles. No revaluation balance is shown in the balance sheet, thus it can be said that the assets are shown by using the cost model method of depreciation. The company is using this method in revaluation model approach the assets are shown at the fair market value which may be recorded at its realisation value. The method of depreciation used reflects the way in which the asset is going to be used in its full economic life varying as per the uses and the requirements of the company in the use of the asset. B. Example of Adjusting Entries: Net Income Adjustment of $508000 is an example of adjustment entry. The positive balance in the cash flow statement shows that this amount is added back in the cash flow statement which reflects that it is Unaccured Income which is received in the current year. Although this figure is not shown in the balance sheet in any specific head, it may be merged in other liabilities or Accounts Payable as this is a liability for the company. VI Communication: A. Memos to the CEO considering the advantages and disadvantages of transitioning from GAAP to IFRS: Memo To: Chief Executive Officer From: XYZ, Controller Date: 10th January, 2018 Re: Advantages and Disadvantages of transitioning from GAAP to IFRS Dear Sir/Madam. I, as a controller of the company hereby inform you about the advantages and disadvantage of transtioning from GAAP to IFRS since soon the company has to change its accounting policies and methods as per IFRS. The main advantages of this are: 1. IFRS focus on accurate, complete, timely and comprehensive financial information that is relevant to the national standards. The information provided is easy for the investors and the stakeholders to understand and aware themselves about the financial performance and condition of the company. 2. It also reduces the cost for the investors which they would have to pay to the analyst for understanding the financial information. 3. Recognition of the loss immediately is also one of the foremost benefit of IFRS. 4. Since the information is provided as per the International guidelines, thus it improves the comparability of the information. 5. It promotes the consistency, transparency and and standardization of the financial information. Disadvantages of IFRS:

- 8. 1. The most noteworthy disadvantage of IFRS is the cost associated with the application of IFRS, training of internal staff, etc. 2. Issues such as extra ordinary loss in the new IFRS is also remains the same. 3. Since it is universal thus its adoption may pose difficulties in many countries due to the change in circumstances. 4. Another demerit is the use of the fair value for the asset/liability measurement while transitioning from GAAP to IFRS. So these are some foremost advantages and disadvantages of transitioning from GAAP to IFRS. Thanking You B. Memo regarding one of the customer gone bankrupt To: Chief Executive Officer From: XYZ, Controller Date: 10th January, 2018 Re: One of the biggest customer gone bankrupt Dear Sir/Madam, This is to inform you that one of our biggest customer ABC has gone bankrupt due to heavy fire in his godown in the last month. The information is not at all soothing to the ears as this incident will surely and largely affect our accounts receivalbles. The amount due to the customer is $100000. He has been our top customer the last year and accounts for almost 40% sales of the year. The main motive of this communication is to bring into your notice the bankruptcy of the customer and what steps to be followed to quickly reclaim the amount to the extent possible. Sale during the current year could be less than the last year due to such incidence. It is not a good news as far as our financial statements are concerned. But hope soon we will find someone better customer in the future. Thanking You