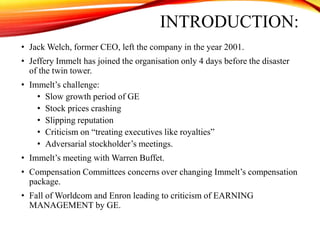

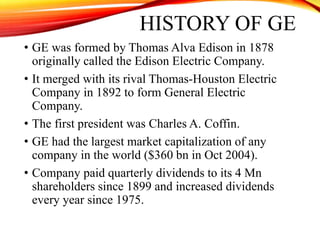

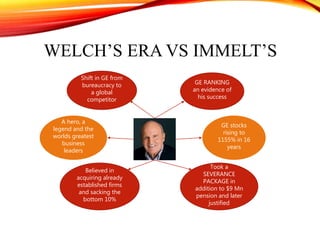

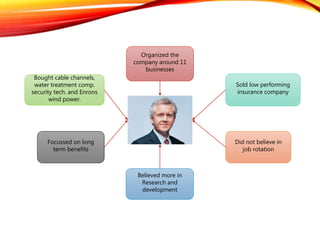

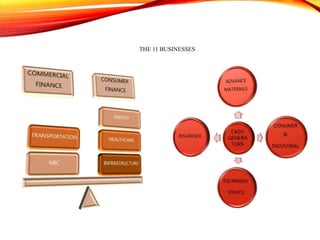

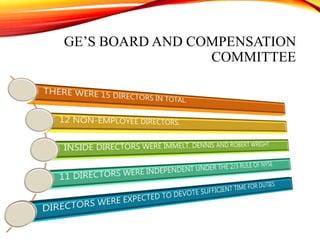

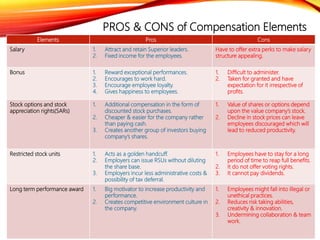

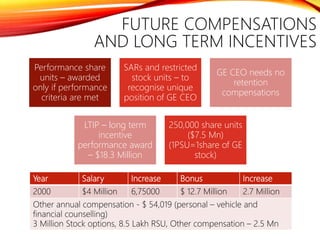

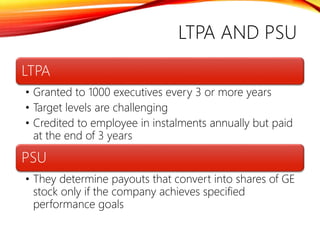

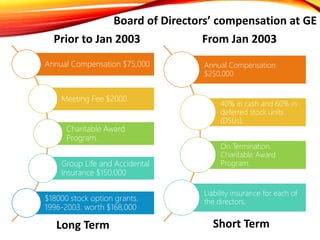

The document summarizes Jeff Immelt's challenges as the new CEO of GE after Jack Welch stepped down in 2001. Immelt took over during a period of economic slowdown, with GE experiencing slow growth, falling stock prices, and criticism of its treatment of executives. The document also provides background on GE's history and leadership changes. It discusses Welch's versus Immelt's approaches, GE's businesses, executive compensation practices, and elements of Immelt's compensation package aimed at long-term performance when he took over as CEO.