- Ranbaxy Laboratories Ltd. is an Indian pharmaceutical company that was found guilty in 2013 of falsifying drug test data and misrepresenting generic drug information submitted to the US FDA.

- In 2004-2005, two Ranbaxy employees blew the whistle on the company's fabrication of drug test reports, which prompted a FDA investigation. This resulted in warning letters and import alerts issued against Ranbaxy plants in 2008-2009.

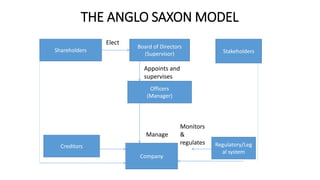

- The case highlights the importance of regulatory compliance, risk management practices, audit functions, and whistleblower protections in ensuring good corporate governance, as emphasized by various Indian committees on the topic.