1.

India Morning Note

a g

Tues

sday, June 1 2012

12,

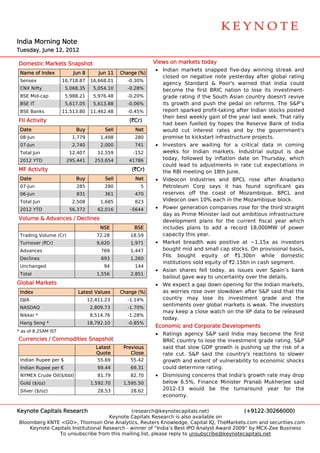

Dom

mestic Mark

kets Snapsh

hot Views on markets t

today

• India markets snapped f

an five-day win

nning streak and

Nam of Index

me Jun 8 Jun 11 Change (%)

)

close on nega

ed ative note y yesterday affter global rating

Sensex 16,718.87 16,668.01 -0.30%

agenncy Standard & Poor' warned that India could

's

CNX Nifty

X 5,068.35 5,054.10 -0.28% becoome the fir BRIC nation to lose its investment-

rst e

BSE Mid-cap 5,988.21 5,976.48 -0.20% grad rating if the South A

de Asian country doesn't r revive

BSE IT 5,617.05 5,613.88 -0.06% its growth and push the p

g pedal on refforms. The S&P’s

BSE Banks 11,513.80 11,462.48 -0.45% repo sparked profit-taking after Indian stocks p

ort posted

their best week gain of th year last week. That rally

r kly he t

FII A

Activity (`Cr)

had been fuelle by hopes the Reser

ed s rve Bank of India

f

Date

e Buy Sell Net would cut inte erest rates and by th governm

he ment's

08-Jun 1,779 1,498 280 prommise to kicks

start infrast

tructure pro

ojects.

07-Jun 2,740 2,000 741 • Investors are wwaiting for a critical data in co

oming

Tota Jun

al 12,407 12,559 -152 weeks for Indian markets Industria output is due

s. al s

2012 YTD 295,441 253,654 41786 toda followed by inflatio date on Thursday, which

ay, d on

could lead to a

adjustments in rate cut expectatio

s t ons in

MF A

Activity (`Cr) the RBI meeting on 18th Ju

R g une.

Date

e Buy Sell Net • Vide

eocon Indusstries and BPCL rose after Ana

adarko

07-Jun 285 280 5 oleum Corp says it has found significant gas

Petro

06-Jun 831 361 470 rese

erves off th coast o Mozamb

he of bique. BPCL and

L

Tota Jun

al 2,508 1,685 823 Vide

eocon own 1

10% each in the Mozam

n mbique block

k.

2012 YTD 56,372 62,016 -5644 • Powe generatio companies rose for the third straight

er on

day as Prime Minister laid out ambitio

ous infrastru

ucture

Volu

ume & Adva

ances / Dec

clines deveelopment plans for the current fiscal year which

f

NSE BSE inclu

udes plans to add a r record 18,0000MW of p power

Trad

ding Volume (Cr) 72.28 18.59 capaacity this ye

ear.

Turn

nover (`Cr) 9,620 1,971 • Markket breadth was posit

h tive at ~1.15x as inve

estors

Advances 769 1,447 boug mid and small cap stocks. On provisional basis,

ght d

FIIs bought e equity of `1.30bn while dom mestic

Declines 693 1,260

institutions sold equity of `

d `2.15bn in cash segmen

nt.

Unchanged 94 144

• Asian shares fe today, a issues ov

ell as ver Spain’s bank

Tota

al 1,556 2,851

bailo gave wa to uncert

out ay tainty over the details.

t

Glob Markets

bal • We expect a gap down ope

e ening for the Indian ma

e arkets,

Inde

ex Late Values

est Change (%)

) as worries rose over slowd

w down after S&P said tha the

S at

DJIA

A 12,411.23 -1.14% coun

ntry may lose its in nvestment grade and thed

sent

timents over global maarkets is weak. The inve

estors

NAS

SDAQ 2,809.73 -1.70%

may keep a close watch on the IIP data to be released

y n

Nikk *

kei 8,514.76 -1.28%

toda

ay.

Hang Seng * 18,792.10 -0.85%

Econom and Cor

mic rporate Dev

velopments

s

* as o 8.25AM IST

of

• Ratin

ngs agency S&P said India may become the first

y e

Curr

rencies / Co

ommodities Snapshot

s BRIC country to lose the in

C o nvestment grade rating S&P

g g.

Latest Previous said that slow G

GDP growth is pushing up the risk of a

h g

Quote Close rate cut. S&P ssaid the coountry's reaactions to s

slower

Indian Rupee per $ 55.69 55.42 grow and extent of vulne

wth erability to economic sshocks

Indian Rupee per € 69.44 69.31 could determine rating.

e

NYM

MEX Crude Oil($/bbl) 81.79 82.70 • Dism

missing conc

cerns that India's growth rate may drop

y

Gold ($/oz)

d 1,592.70 1,595.50 below 6.5%, Finance Minister Pranab Mukherjee said

b e

Silve ($/oz)

er 28.53 28.62 20122-13 would be the turnaround year for the

d d

econ

nomy.

Keyn

note Capitals Research

h (reseaarch@keyno otecapitals.net) (+91222-3026600 00)

Keyynote Capita Research is also available on

als h

Bloo

omberg KNTE <GO>, Tho

E omson One A Analytics, Re

euters Knowwledge, Capit IQ, TheMa

tal arkets.com and securitie

a es.com

Keynote Capitals Institu

utional Resea

arch - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

To unsubsc cribe from th mailing lis please reply to unsub

his st, bscribe@keyynotecapitals

s.net

2.

TOP GAINERS Buzzin Stocks

ng

(BSE A-Group)

E • Vide

eocon and Philips are gearing up to usher in a

p

Previous Currennt Change new regime wi

w ith new mo odels that can receive and

c

Com

mpany Name

e

Close(`

`) Price(`

`) (%) adcast TV signals witho a set-top box, though a

broa out

Volt

tas 104.15

5 108.15 3.84 debate over th preparedness of cab operator to

he ble rs

Vide

eocon Inds 169.55

5 175.00 3.21 migrate to digit

tisation from July 1 continues to ra

m age.

Synd

dicate Bank 96.90

0 99.65 2.84 • The two companies are launching light-emit

e g tting

Lanc Infra

co 13.28

8 13.65 2.79 diod (LED) TV that will eliminate the need f

de Vs for a

ADA POWER

ANI 47.00

0 48.10 2.34 set-top box, a d

device otheerwise neces

ssary to rec

ceive

(BSE Mid-Cap)

E digit signals in the new regime. This will be the

tal w T e

seco

ond time that Videocon will take a shot at this; it

n

Previous Currennt Change had launched ‘Satellite TV almost five years ago,

Vs’

Com

mpany Name

e

Close(`

`) Price(`

`) (%)

but these didn’t work in the marketpla

ace.

GVK Power

K 12.65 14.40 13.83

KSK Energy

K 51.15 53.70 4.99 • Vedanta Aluminum Ltd (V VAL) is plann

ning to buy the

y

Anant Raj Inds 47.35 49.55 4.65 pow

wer business undertak king of Mad dras Aluminnium

Volt

tas 104.15 108.15 3.84 Commpany Ltd (Malco) fo an estimated `15

or 50Cr.

Vedanta Group will subse

p equently me erge Malco with

Raymond 369.25 382.65 3.63

Sesa Goa as pa of a larg amalgam

a art ger mation scheeme,

TOP LOSERS acco

ording to V VAL Group’s Sterlite In

s ndustries (In

ndia)

Ltd. Vedanta “ “shall pay t Malco a lump-sum cash

to

(BSE A-Group)

E conssideration o around `

of `150Cr”, sa a note f

aid from

Previous Currennt Change Ster

rlite Industri

ies.

Com

mpany Name

e

Close(`

`) Price(`

`) (%)

• Suzl

lon said tha the holders of the June tranch of

at J he

Lupi

in 546.10

0 524.45

5 -3.96

FCC

CBs (foreign currency convertible bonds) h

n e have

Sun TV Network 257.65

5 248.55

5 -3.53

approved its p proposal for an extens

r sion of maturity

Unio Bank

on 212.40

0 205.10

0 -3.44

date until July 2

e 27.

Havells India 562.70

0 544.55

5 -3.23

US markets

Pidil

lite Inds 174.25

5 169.00

0 -3.01

U.S. stocks drop

s pped sharp ply Monday as inves

y, stors

(BSE Mid-Cap)

E fretted coming events, includ

d ding election in Greece

ns e.

Previous Currennt Change The Do Jones Ind

ow dustrial Ave

erage slid 14

42.97 point or

ts,

Com

mpany Name

e

Close(`

`) Price(`

`) (%)

1.1%, at 12,411.2 The S&P 500 Index declined 16.73

23. P

Pres

stige Estates 122.20 115.15 -5.77

points, or 1.3%, at 1,308.93 The Nas

3. sdaq Compo osite

COX KINGS

X 137.80 131.55 -4.54

Index slipped 48.6 points, or 1.7%, at 2,809.73.

s 69 r

D B REALTY 89.70 85.90 -4.24

Mon

nnet Ispat 340.45 327.20 -3.89

Delt Corp

ta 65.85 63.30 -3.87

Keyn

note Capitals Research

h (resea

arch@keyno

otecapitals.net) (+912

22-3026600

00)

3.

India and Globa Economic Calendar

a al c

Countries / Tue

esday Wed

dnesday Th

hursday Friday

Reg

gions 12-Jun 13

3-Jun 14-Jun

1 15-Jun

Ind

dia Index of In

ndustrial WPI base Inflation

ed Forex Reserves Data

R

Production (IIP) for

n for the m

month of Ma

ay

April 2012

2 2012

Bank Lo

oan Growth

US Monthly budget Retail Sales Capacity utilization

y Industri Productio

ial on

statementt (MoM), Capacity

Utilization, Total Ne

et

TIC Flowws

Business Inventories

s NY Emp pire State

Manufacturing Inde ex

Glo

obal UK industr

rial Germany CPI Data

y Euro Zo

one

production

n Employyment Chang ge

(YoY & QoQ) & Trad de

Balance n.s.a

e

UK Trade balance UK Goods Trade

Balance & Trade

e

Balance non- EU

e;

Japan BoJ Interest

B

Rate De

ecision

KEYN

NOTE CAPITTALS LTD.

The Rub 9th Floo Senapati Bapat Marg, Dadar (W), Mumba – 400 028

by, or, ai 8

Tel. : +9

9122-30266

6000 • www

w.keynotec

capitals.com

m

Disclaiimer: This re

eport is purely for informa ation purpose and is bassed on public information News cont

c n. tent is attribu

utable to

various media, unle specified otherwise. A market related statistic data perta

ess All cal ains to the im

mmediately preceding trad ding day,

unless stated other

s rwise. Neithe the informa

er ation nor any opinion expressed in this report constitutes an off

y s fer, or an invitation to

make an offer, to bbuy or sell the securities m

mentioned he erein. We or any of our directors, offic

cers or emplo

oyees shall not in any

way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgmen before

e e s m e o nt

acting on the conteents of this re

eport. The rep

port has not been edited due to time c

d constraints.