FNB_Gauteng Sub-Region House Price Indices

•

1 like•73 views

FNB_Gauteng Sub-Region House Price Indices

Recommended

Recommended

More Related Content

Similar to FNB_Gauteng Sub-Region House Price Indices

Similar to FNB_Gauteng Sub-Region House Price Indices (20)

More from Berty Van Staaden

More from Berty Van Staaden (20)

Recently uploaded

Recently uploaded (20)

FNB_Gauteng Sub-Region House Price Indices

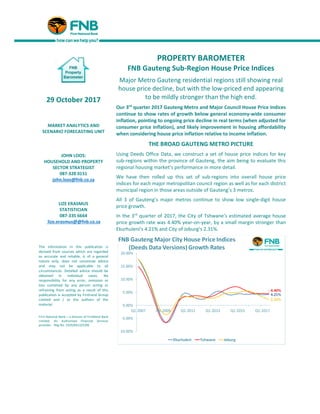

- 1. 29 October 2017 MARKET ANALYTICS AND SCENARIO FORECASTING UNIT JOHN LOOS: HOUSEHOLD AND PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za LIZE ERASMUS STATISTICIAN 087-335 6664 lize.erasmus@@fnb.co.za The information in this publication is derived from sources which are regarded as accurate and reliable, is of a general nature only, does not constitute advice and may not be applicable to all circumstances. Detailed advice should be obtained in individual cases. No responsibility for any error, omission or loss sustained by any person acting or refraining from acting as a result of this publication is accepted by Firstrand Group Limited and / or the authors of the material. First National Bank – a division of FirstRand Bank Limited. An Authorised Financial Services provider. Reg No. 1929/001225/06 PROPERTY BAROMETER FNB Gauteng Sub-Region House Price Indices Major Metro Gauteng residential regions still showing real house price decline, but with the low-priced end appearing to be mildly stronger than the high end. Our 3rd quarter 2017 Gauteng Metro and Major Council House Price Indices continue to show rates of growth below general economy-wide consumer inflation, pointing to ongoing price decline in real terms (when adjusted for consumer price inflation), and likely improvement in housing affordability when considering house price inflation relative to income inflation. THE BROAD GAUTENG METRO PICTURE Using Deeds Office Data, we construct a set of house price indices for key sub-regions within the province of Gauteng, the aim being to evaluate this regional housing market’s performance in more detail. We have then rolled up this set of sub-regions into overall house price indices for each major metropolitan council region as well as for each district municipal region in those areas outside of Gauteng’s 3 metros. All 3 of Gauteng’s major metros continue to show low single-digit house price growth. In the 3rd quarter of 2017, the City of Tshwane’s estimated average house price growth rate was 4.40% year-on-year, by a small margin stronger than Ekurhuleni’s 4.21% and City of Joburg’s 2.31%.

- 2. REAL HOUSE PRICE PERFORMANCES With Gauteng Consumer Price Index (CPI) Inflation at 4.8% year-on-year for the 3rd quarter of 2017, these low nominal house price growth rates translate into house price declines in real terms (when adjusted for CPI), Tshwane to the tune of -0.3% year-on-year, Ekurhuleni -0.5% and Joburg -2.3%. The 3 Gauteng Metros have been undergoing a gradual real house price correction for much of the time since the beginning of 2008. Since the 1st quarter of 2008, Tshwane’s cumulative real house price decline has been -22.3%, Joburg -24.25% and Ekurhuleni -25.5%. WE ZOOM IN ON THE CITY OF JOBURG’S MAIN REGIONS….MEDIOCRE GROWTH EVERYWHERE, WITH THE FORMER TOWNSHIP REGION AROUND SOWETO SHOWING THE HIGHEST GROWTH There are no strong “outperforming” regions in Gauteng of late. Over the past 5 years, the lowest income region, i.e. the former “township” region of Diepkloof-Soweto-Meadowlands-Pimville has shown the strongest cumulative growth of 42.82%, with the Midrand-Diepsloot region a distant second with 26.33% cumulative growth. At the weak end, the highest priced region of “Sandton and Surrounds” has grown the slowest growth off the highest base, i.e. 17.92%.

- 3. More recently, the Diepkloof-Soweto-Meadowlands-Pimville region remains the highest estimated house price growth region at 4.28% year-on-year in the 3rd quarter of 2017. However, this price growth rate itself is weak, negative in real terms, and only slightly above the other low end region of Lenasia-Orange Farm-Ennerdale- Lawley, at 4.04%. Nevertheless, this would suggest that the City of Joburg lower price markets are a little stronger, and the high end weaker, with the most expensive “Sandton and Surrounds” end measuring a very slight -0.1% year-on-year price decline. TSHWANE – ALSO HINTING AT SLIGHTLY STRONGER LOWER END MARKETS In Tshwane, the relative market strength of late also appears to have been more at the low end. Over the past 5 years, cumulative house price growth within Tshwane is estimated to have been the strongest in the Winterveldt-Mabopane-Soshanguve-Ga-Rankuwa-Hammanskraal region, to the tune of 66.98%. In such former “township” regions, care must be taken with interpretation, because where Government subsidized “RDP” homes are transferred to their new owners, the registered amount in the deeds data can be below market value, meaning that a repeat sale can come off an artificially low base.

- 4. However, another low end area, Pretoria West, shows the 2nd highest cumulative growth to the tune of 42.11%, followed by Pretoria North East with 32.44%, also thus pointing to low end markets having done a little better than higher priced regions in recent years. In the 3rd quarter of 2017, those 3 same regions again came out as the 3 highest price growth regions too. EKURHULENI SUB-REGION PERFORMANCE Ekurhuleni also appears to have experienced greater market strength at the lower end. Some of the strongest cumulative house price growth over the past 5 years was seen in the lowest average priced areas, namely Tokoza- Vosloorus-Katlehong with 44.33%, Nigel with 37.91%, Brakpan with 30.81% and Springs by 28.49%. Those 4 regions are the 4 lowest average house price regions in Ekurhuleni. Olifantsfontein region, a relatively high priced region by Ekurhuleni standards, in excess of R800,000 (R805,000) showed very strong growth of 40.85%, but we believe that this is in part due to difficulty in eliminating much of the “land-to-building” effect on the repeat sales index, as this is a relatively new area with much building activity in recent years. Other higher end areas with average prices above R800,000 (higher by Ekurhuleni standards) such as Alberton (16.97%) and Edenvale (16.7%) had relatively low cumulative house price growth.

- 5. In the 3rd quarter of 2017, it remained the lower average price end that seemed to do better, with Nigel (18.6%), Tokoza-Vosloorus-Katlehong (11.8%) and Brakpan (6.94%) being the strongest 3 regions price growth-wise. THE MANUFACTURING-DEPENDENT EMFULENI REGION APPEARS TO REMAIN THE MOST DEPRESSED HOUSING MARKET The Emfuleni District, which includes major towns of Van der Bijl Park and Vereeniging, is heavily Manufacturing dependent, and the Manufacturing Sector in South Africa has been in the doldrums in recent years. The Van der Bijl Park area is especially Manufacturing-heavy. This, we believe, has had an influence on cumulative Emfuleni house price growth of only 21.65% over the past 5 years, but more specifically on the Van der Bijl Park region’s weak 16.03% cumulative house price growth.

- 6. As at the 3rd quarter of 2017, the region’s year-on-year percentage change was very weak at a slightly positive +0.07% rate, with Van der Bijl’s negative -0.41% rate being the weakest sub-region of Emfuleni CONCLUSION Although the Gauteng residential markets don’t show any great strength at present, there appears to be a broad pattern of low priced sub-regions performing a little better than the high-priced end. This appears to tie in with what the FNB Estate Agent Survey tells us regarding 1st time buyer levels in Gauteng’s Metros, i.e. that in the 2017 year-to-date, estimated 1st time buying in Greater Joburg was 26.62% of total home buying, and 24.3% in Tshwane, both percentages being relatively strong and above the national average of 20.26%. Solid 1st time buying in the province may be a key source of support for the low end of the housing market. At the high priced end in each metro, on the other hand, confidence in the country’s economic future can be a reason for buyer caution amongst higher income groups, while it is also arguably about the high running and transaction costs related to higher value homes that comes with municipal rates and tariffs rising at rates well-above general inflation in recent years, and higher transfer duty brackets at the high end. However, while the low priced end appears to be stronger than higher up the price ladder, broadly speaking, it is by no means very strong either. Down in the Emfuleni Regions near the Vaal River, the Manufacturing-dependent Van der Bijl Park appears to stand out as the weakest housing region in Gauteng.

- 7. HOUSE PRICE GROWTH SUMMARY TABLES Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth CITY OF JOHANNESBURG TOTAL 3.79% 3.26% 2.77% 2.31% 248.88% 22.10% Johannesburg 4.29% 3.65% 2.57% 1.53% 279.65% 20.13% Johannesburg South 4.65% 3.97% 3.32% 2.67% 271.02% 20.19% Diepkloof-Soweto-Meadowlands-Pimville 3.71% 3.10% 3.28% 4.28% 831.22% 42.82% Midrand_Diepsloot 4.78% 4.26% 3.46% 2.68% 243.43% 26.33% Randburg 3.68% 3.44% 3.46% 3.56% 197.02% 20.63% Roodepoort 2.21% 2.21% 2.82% 3.55% 201.10% 19.93% Sandton and Surrounds 2.35% 1.48% 0.62% -0.10% 167.55% 17.92% Lanasia-Orange Farm-Ennerdale-Lawley 5.51% 5.00% 4.27% 4.04% 378.42% 19.71% Quarterly year-on-year percentage change CITY OF JOHANNESBURG SUB-REGIONAL HOUSE PRICE INDICES – AVERAGE GROWTH RATES

- 8. Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth CITY OF TSHWANE ROLL UP 4.52% 4.54% 4.52% 4.40% 231.54% 29.69% Akasia 1.84% 2.39% 3.90% 5.51% 263.93% 23.94% Bronkhorstspruit-Cullinan- Rayton-Ekangala-Refilwe 4.60% 4.56% 3.17% -0.46% 274.04% 14.74% Centurion 4.88% 4.44% 3.87% 3.26% 194.83% 29.19% Pretoria-Roodeplaat 4.11% 4.50% 4.68% 4.46% 209.41% 26.76% Winterveldt-Mabopane- Soshanguve-GaRankuwa- Hammanskraal-Kudube- Themba 12.61% 10.77% 11.18% 13.14% 607.26% 66.98% Pretoria Central 3.78% 5.80% 7.00% 7.19% 362.17% 23.33% Pretoria East 5.27% 4.53% 3.79% 3.24% 177.35% 27.36% Pretoria North 3.52% 4.20% 4.62% 4.73% 212.96% 23.77% Pretoria North East 4.68% 6.60% 8.53% 8.91% 297.32% 32.44% Pretoria South East -0.93% 0.20% 0.20% 0.01% 205.06% 21.42% Pretoria West 5.44% 8.17% 10.67% 12.59% 420.43% 42.11% PRETORIA ROLL UP 4.56% 5.33% 5.99% 6.28% 241.11% 30.00% Quarterly year-on-year percentage change CITY OF TSHWANE SUB-REGIONAL HOUSE PRICE INDICES – AVERAGE GROWTH RATES

- 9. Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth EKURHULENI 4.17% 4.03% 4.06% 4.21% 289.06% 24.26% Alberton 2.47% 2.91% 2.80% 2.31% 232.77% 16.97% Benoni 2.65% 1.80% 1.62% 1.77% 207.77% 15.08% Boksburg 3.35% 2.56% 1.91% 1.27% 219.20% 16.88% Brakpan 6.46% 7.42% 7.78% 6.94% 329.32% 30.81% Edenvale 1.01% 0.43% 0.11% -0.17% 213.03% 16.70% Germiston 3.69% 4.30% 4.42% 3.95% 260.43% 21.39% Kempton Park 4.84% 5.12% 5.03% 5.03% 268.61% 22.93% Nigel 8.78% 10.09% 13.88% 18.61% 448.82% 37.91% Olifantsfontein 5.94% 2.87% 0.23% -1.38% 1033.04% 40.85% Springs 3.65% 3.13% 3.24% 4.00% 323.52% 28.49% Tokoza-Voloorus-Katlehong 3.42% 4.93% 7.50% 11.80% 782.68% 44.33% Quarterly year-on-year percentage change CITY OF EKURHULENI SUB-REGIONAL HOUSE PRICE INDICES – AVERAGE GROWTH RATES

- 10. Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth EMFULENI 3.83% 2.84% 1.01% 0.07% 353.85% 21.65% Evaton-Sebokeng 12.79% 10.09% 5.02% 3.89% 615.25% 63.77% Vaal-Vanderbijlpark 1.62% 0.70% -0.44% -0.41% 333.60% 16.03% Vereeniging 3.93% 4.54% 4.06% 2.90% 313.72% 21.76% Quarterly year-on-year percentage change Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth MOGALE CITY 2.37% 3.12% 4.23% 5.09% 262.26% 26.12% Krugersdorp-Magaliesburg-Mogale 3.33% 3.32% 3.00% 2.21% 226.41% 22.98% Randfontein 0.25% 3.61% 8.48% 13.88% 291.55% 28.05% Quarterly year-on-year percentage change Q4-2016 Q1-2017 Q2-2017 Q3-2017 Cumulative 15- year growth Cumulative 5- year growth LESEDI 0.94% -1.75% -3.74% -4.17% 244.15% 9.62% MERAFONG 5.57% 2.84% 2.22% 1.79% 306.09% 9.56% MIDVAAL 2.85% 5.60% 8.21% 9.70% 339.00% 36.14% WESTONARIA 10.67% 13.66% 14.41% 15.26% 545.56% 38.78% Quarterly year-on-year percentage change