Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to FNB_Property Insights

Similar to FNB_Property Insights (20)

More from Berty Van Staaden

More from Berty Van Staaden (20)

Recently uploaded

Recently uploaded (20)

FNB_Property Insights

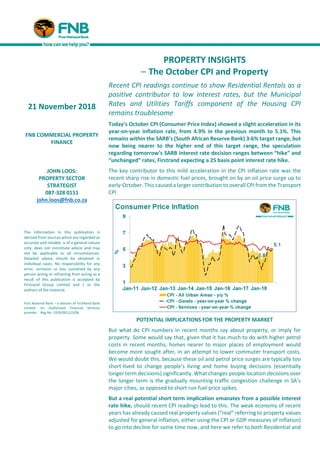

- 1. PROPERTY INSIGHTS – The October CPI and Property Recent CPI readings continue to show Residential Rentals as a positive contributor to low interest rates, but the Municipal Rates and Utilities Tariffs component of the Housing CPI remains troublesome Today’s October CPI (Consumer Price Index) showed a slight acceleration in its year-on-year inflation rate, from 4.9% in the previous month to 5.1%. This remains within the SARB’s (South African Reserve Bank) 3-6% target range, but now being nearer to the higher end of this target range, the speculation regarding tomorrow’s SARB interest rate decision ranges between “hike” and “unchanged” rates, Firstrand expecting a 25 basis point interest rate hike. The key contributor to this mild acceleration in the CPI inflation rate was the recent sharp rise in domestic fuel prices, brought on by an oil price surge up to early-October. This caused a larger contribution to overall CPI from the Transport CPI POTENTIAL IMPLICATIONS FOR THE PROPERTY MARKET But what do CPI numbers in recent months say about property, or imply for property. Some would say that, given that it has much to do with higher petrol costs in recent months, homes nearer to major places of employment would become more sought after, in an attempt to lower commuter transport costs. We would doubt this, because these oil and petrol price surges are typically too short-lived to change people’s living and home buying decisions (essentially longer term decisions) significantly. What changes people location decisions over the longer term is the gradually mounting traffic congestion challenge in SA’s major cities, as opposed to short run fuel price spikes. But a real potential short term implication emanates from a possible interest rate hike, should recent CPI readings lead to this. The weak economy of recent years has already caused real property values (“real” referring to property values adjusted for general inflation, either using the CPI or GDP measures of inflation) to go into decline for some time now, and here we refer to both Residential and 21 November 2018 FNB COMMERCIAL PROPERTY FINANCE JOHN LOOS: PROPERTY SECTOR STRATEGIST 087-328 0151 john.loos@fnb.co.za The information in this publication is derived from sources which are regarded as accurate and reliable, is of a general nature only, does not constitute advice and may not be applicable to all circumstances. Detailed advice should be obtained in individual cases. No responsibility for any error, omission or loss sustained by any person acting or refraining from acting as a result of this publication is accepted by Firstrand Group Limited and / or the authors of the material. First National Bank – a division of FirstRand Bank Limited. An Authorised Financial Services provider. Reg No. 1929/001225/06

- 2. Commercial Property. Should the October CPI reading lead to a rate hike, we would expect property demand to remain weak in this economic environment, and for real property values to remain in decline. WHAT THE CPI SAYS ABOUT THE PROPERTY MARKET – RENTAL MARKET WEAKNESS, BAD FOR LANDLORDS BUT GOOD FOR INTEREST RATES The Property Market itself is a key positive contributor in terms of keeping CPI inflation within the 3-6% target range. And here we refer specifically to the Residential Rental part of the Property Market. The Actual Rental and Owner Equivalent Housing Rental CPI Sub-Indices carry a large weighting of 16.84% of the total CPI together. This is almost as big as the Food and Non-Alcoholic Beverages CPI’s weighting of 17.24%, and a weak Residential Rental Market in recent times has contributed to the low CPI/low interest rate cause. The CPI for Actual Rentals showed inflation of 4.03% (last surveyed in September CPI), having slowed in recent surveys, and the Owner Equivalent Rental CPI an even slower 3.66%. UTILITIES TARIFFS AND MUNICIPAL RATES REMAIN TROUBLESOME However, the overall Housing CPI inflation rate remains mildly “troublesome” for the Overall CPI inflation rate, recording an October rate of 5.2% due to ongoing strong inflation in Municipal Rates and Utilities Tariffs, which are components of the Housing CPI, being costs directly related to owning or renting a house. Municipal Rates and Non-Electricity Utilities Tariffs (“Water and Other Services” CPI) are most troublesome, recording year-on-year inflation of 11.1%. The CPI for Electricity and Other Fuels showed 7.73% year-on-year inflation, also well above overall CPI inflation. By comparison, the CPI for Home Maintenance is better behaved at 3.1% year-on-year. It is possible that this latter CPI component reflects the Home Maintenance Industry being partly “crowded out” by ongoing sharp cost increases for homeowners emanating from Municipal Rates and Tariffs. The long term trend of Municipal Rates and Tariffs inflation far outstripping general inflation raises the affordability challenges for tenants and owners, incentivizing a shift to alternative sources of power to Eskom, while also incentivizing better use of property/space. SMALLER IS BETTER IN THE HOUSING RENTAL MARKET So finally, perhaps not surprising is that the CPI figures also point to “smaller being better” in terms of home rentals, the Flat Rental and Townhouse Rental CPIs continuing to outperform the “Houses” CPI, the latter being on average the largest category and the most costly to run. The Flats Rental CPI inflated by 4.7% year-on-year in October, The Townhouses CPI by a similar 4.8%, and the House CPI by a noticeably lesser 3.5%. Since January 2008, just over a decade, the Flats CPI has inflated cumulatively by 90%, Townhouses by 75.9% and Houses by 62.6%.

- 3. May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Key CPI Inflation Measures CPI - All Urban Areas 107.2 107.6 108.5 108.4 108.9 109.4 Y-o-Y % Change 4.4 4.6 5.1 4.9 4.9 5.1 CPI - All Goods 106.0 106.5 107.5 107.4 107.6 108.6 Y-o-Y % Change 3.5 4.2 5.3 5.0 4.8 5.1 CPI - All Services 108.4 108.7 109.4 109.4 110.2 110.2 Y-o-Y % Change 5.3 4.9 5.0 5.0 5.2 5.1 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Key CPI Housing and Related Measures CPI - Housing and Utilities 105.7 106.0 108.4 108.5 109.4 109.4 Y-o-Y % Change 4.8 4.1 5.2 5.3 5.29 5.19 CPI - Actual housing rentals 106.4 106.9 106.9 106.9 108.4 108.4 Y-o-Y % Change 5.1 4.2 4.2 4.2 4.03 4.03 - Houses 105.9 106.1 106.1 106.1 107.5 107.5 Y-o-Y % Change 4.7 3.6 3.6 3.6 3.5 3.5 - Townhouses 107.7 107.6 107.6 107.6 109.4 109.4 Y-o-Y % Change 6.3 4.6 4.6 4.6 4.8 4.8 - Flats 107.1 108.3 108.3 108.3 109.8 109.8 Y-o-Y % Change 5.8 5.1 5.1 5.1 4.7 4.7 CPI - Owner occupied housing rentals 105.8 106.2 106.2 106.2 107.5 107.5 Y-o-Y % Change 4.6 3.7 3.7 3.7 3.66 3.66 - Houses 105.7 106.0 106.0 106.0 107.3 107.3 Y-o-Y % Change 4.5 3.5 3.5 3.5 3.5 3.5 - Townhouses 106.6 106.9 106.9 106.9 108.4 108.4 Y-o-Y % Change 5.3 4.4 4.4 4.4 4.3 4.3 - Flats 106.4 107.5 107.5 107.5 108.9 108.9 Y-o-Y % Change 5.3 4.7 4.7 4.7 4.3 4.3 CPI - Home Maintenance and Repairs 104.5 105.1 105.2 105.5 105.3 105.6 Y-o-Y % Change 2.5 2.9 2.9 3.0 3.0 3.1 CPI - Housing - Water and other services 107.9 107.9 118.9 119.1 119.1 119.1 Y-o-Y % Change 7.3 7.1 11.0 11.2 11.1 11.1 CPI - Housing - Electricity and other fuels 103.1 103.1 110.0 110.1 110.1 110.1 Y-o-Y % Change 3.1 3.1 7.7 7.8 7.8 7.7 Consumer Inflation - Key Components Consumer Inflation - Housing - Related Components

- 4. May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Key CPI Product and Service Categories CPI - Housing and Utiilities 105.7 106.0 108.4 108.5 109.4 109.4 Y-o-Y % Change 4.8 4.1 5.2 5.3 5.3 5.2 CPI - Food and Non-Alcoholic Beverages 106.8 106.8 107.1 107.0 107.3 107.5 Y-o-Y % Change 3.4 3.4 3.4 3.5 3.9 3.4 CPI - Alcoholic Beverages and Tobacco 108.7 108.7 109.0 108.8 108.9 109.4 Y-o-Y % Change 6.2 6.0 6.0 4.6 4.2 4.2 CPI - Clothing and Footwear 102.6 102.8 102.9 103.1 103.2 103.3 Y-o-Y % Change 1.7 1.8 1.8 1.9 1.9 2.0 CPI - Household Contents and Equipment 102.9 103.9 104.0 103.8 104.5 104.4 Y-o-Y % Change 2.4 2.7 2.8 2.9 3.0 3.0 CPI - Health 110.7 110.7 110.7 111.3 111.7 111.4 Y-o-Y % Change 4.8 4.7 4.4 5.2 5.4 5.0 CPI - Transport 108.2 110.2 111.3 111.4 112.4 115.3 Y-o-Y % Change 5.0 7.3 10.0 9.5 8.7 10.5 CPI - Communication 100.3 100.1 100.0 100.0 99.8 99.8 Y-o-Y % Change 1.1 1.1 1.1 1.2 1.1 1.2 CPI - Recreation and Culture 101.9 101.3 101.3 101.2 101.2 101.3 Y-o-Y % Change 1.3 0.6 0.4 0.3 0.5 0.7 CPI - Education 114.2 114.2 114.2 114.2 114.2 114.2 Y-o-Y % Change 6.7 6.7 6.7 6.7 6.7 6.7 CPI - Restaurants and Hotels 105.3 105.0 105.4 105.6 105.9 106.1 Y-o-Y % Change 5.0 4.5 4.2 4.0 4.6 4.2 CPI - Miscellaneous 113.0 113.1 113.1 113.0 113.1 113.0 Y-o-Y % Change 6.2 6.2 5.7 5.6 5.5 5.4 Consumer Inflation - Key Product and Service Categories