Downloaded 137 times

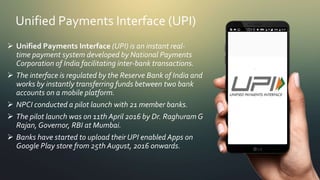

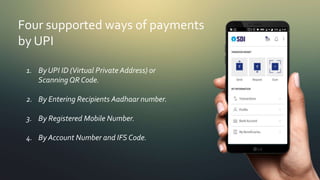

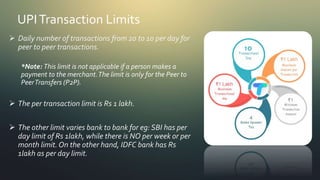

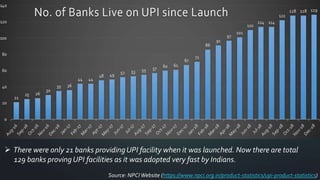

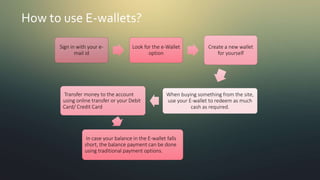

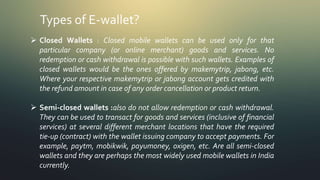

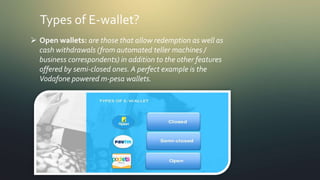

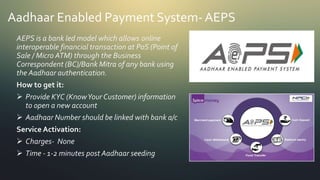

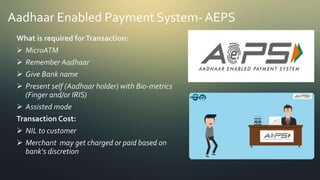

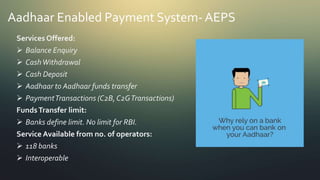

This document provides information about Unified Payments Interface (UPI), e-wallets, Aadhaar Enabled Payment System (AEPS), and Bharat QR. UPI allows instant fund transfer between bank accounts on mobile. E-wallets store money online to make purchases. AEPS allows cash withdrawals and deposits using Aadhaar authentication at micro ATMs. Bharat QR is a common QR code standard for person to merchant mobile payments in India.

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)