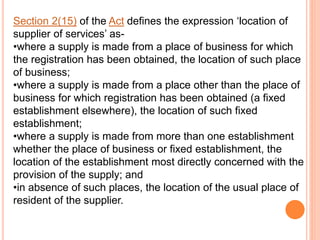

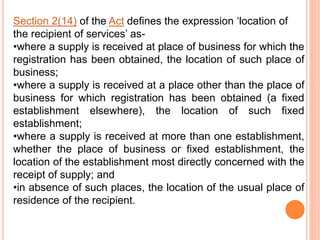

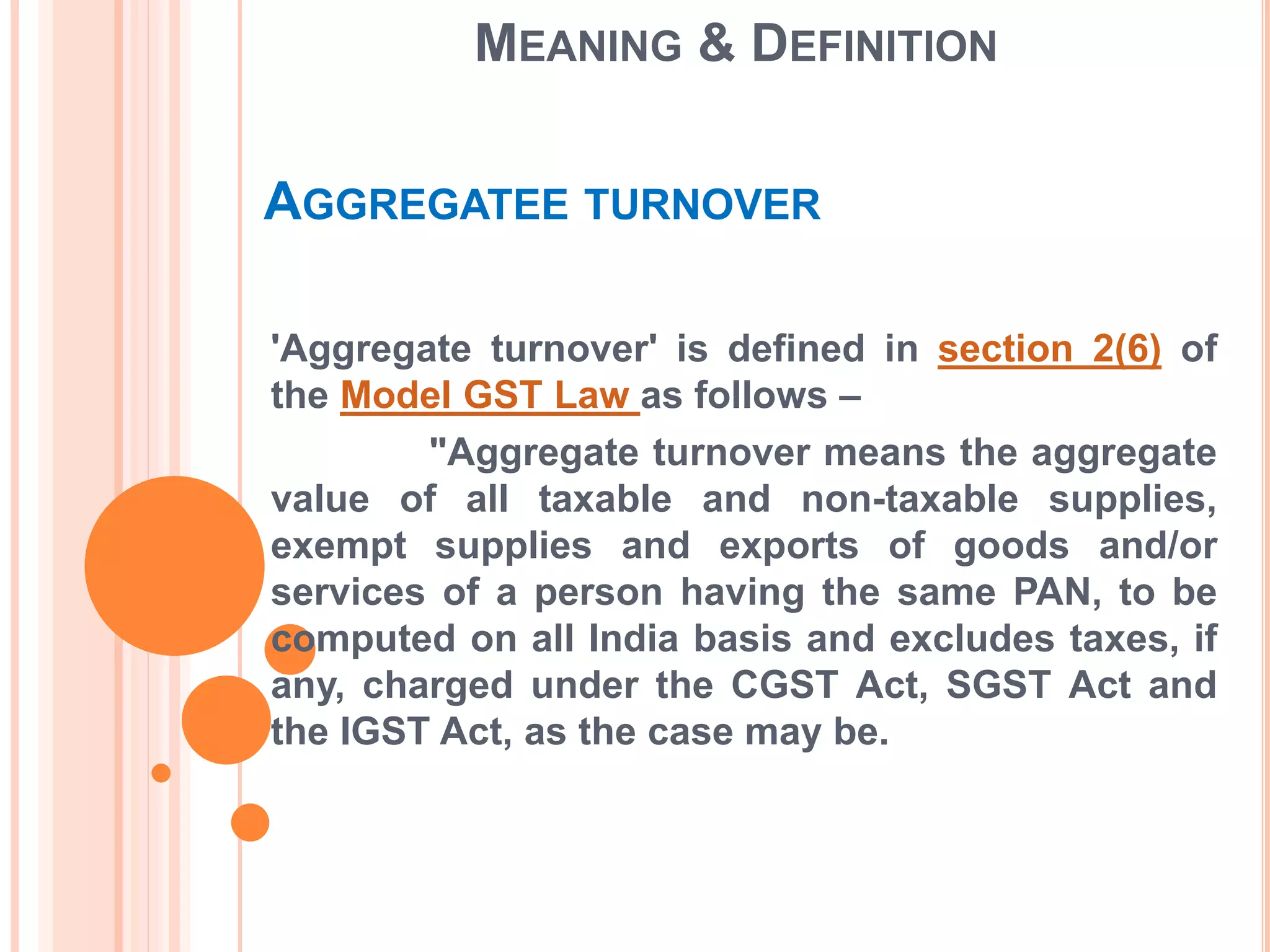

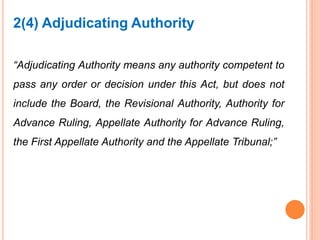

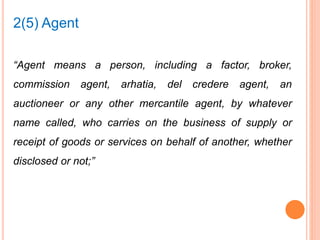

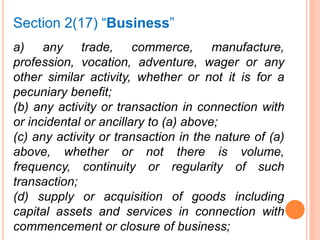

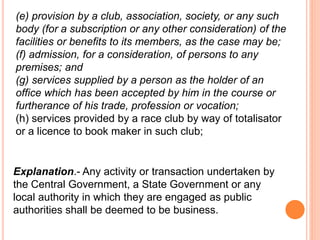

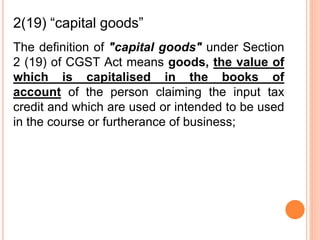

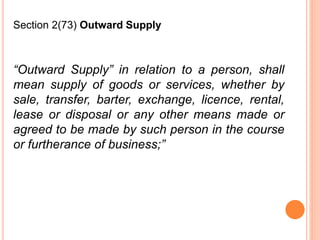

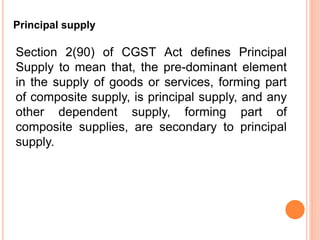

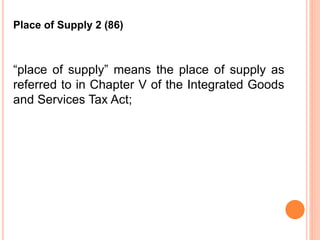

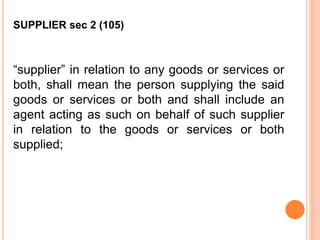

The document defines key terms from the Model GST Law and CGST Act related to aggregate turnover, adjudicating authority, agent, business, capital goods, casual taxable person, composite supply, exempt supply, goods, input service distributor, input tax, job work, manufacture, mixed supply, non-resident taxable person, outward supply, person, place of business, place of supply, principal supply, reverse charge, supplier, works contract. It provides concise definitions for these important GST concepts in 2-3 sentences each.

![“Goods” means every kind of movable property

other than money and securities but includes

actionable claim, growing crops, grass and

things attached to or forming part of the land

which are agreed to be severed before supply or

under a contract of supply;

Goods [Section 2(52) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-15-320.jpg)

![“Input Service Distributor” means an office of the

supplier of goods or services or both which

receives tax invoices issued under section 31

towards the receipt of input services and issues

a prescribed document for the purposes of

distributing the credit of central tax, State tax,

integrated tax or Union territory tax paid on the

said services to a supplier of taxable goods or

services or both having the same Permanent

Account Number as that of the said office;

Input Service Distributor [Section 2(61) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-16-320.jpg)

![“Job Work” means any treatment or process

undertaken by a person on goods belonging to

another registered person and the expression

“job worker” shall be construed accordingly;

Job Work [Section 2(68) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-17-320.jpg)

![“Manufacture” means processing of raw material

or inputs in any manner that results in

emergence of a new product having a distinct

name, character and use and the term

“manufacturer” shall be construed accordingly;

Manufacture [Section 2(72) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-18-320.jpg)

![“Input Tax” in relation to a registered person,

means the central tax, State tax, integrated tax

or Union territory tax charged on any supply of

goods or services or both made to him and

includes—

Input Tax [Section 2(62) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-19-320.jpg)

![(a) an individual;

(b) a Hindu Undivided Family;

(c) a company;

(d) a firm;

(e) a Limited Liability Partnership;

(f) an association of persons or a body of individuals, whether

incorporated or not, in India or outside India;

(g) any corporation established by or under any Central Act, State Act or

Provincial Act or a Government company as defined in clause (45) of

section 2 of the Companies Act, 2013;

(h) any body corporate incorporated by or under the laws of a country

outside India;

(i) a co-operative society registered under any law relating to co-operative

societies;

(j) a local authority;

(k) Central Government or a State Government;

(l) society as defined under the Societies Registration Act, 1860;

(m) trust; and

(n) every artificial juridical person, not falling within any of the above;

Person [Section 2(84) of CGST Act 2017]: “Person” includes—](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-21-320.jpg)

![(a) a place from where the business is ordinarily

carried on, and includes a warehouse, a godown or

any other place where a taxable person stores his

goods, supplies or receives goods or services or

both; or

(b) a place where a taxable person maintains his

books of account; or

(c) a place where a taxable person is engaged in

business through an agent, by whatever name

called;

Place of Business [Section 2(85) of CGST Act 2017]: “Place of

Business” includes––](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-22-320.jpg)

![“Reverse Charge” means the liability to pay tax by

the recipient of supply of goods or services or both

instead of the supplier of such goods or services or

both under sub-section (3) or sub-section (4) of

section 9, or under sub-section (3) or subsection (4)

of section 5 of the Integrated Goods and Services

Tax Act;

Reverse Charge [Section 2(98) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-23-320.jpg)

![“Works Contract” means a contract for building,

construction, fabrication, completion, erection,

installation, fitting out, improvement, modification,

repair, maintenance, renovation, alteration or

commissioning of any immovable property wherein

transfer of property in goods (whether as goods or in

some other form) is involved in the execution of such

contract;

Works Contract [Section 2(119) of CGST Act 2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-24-320.jpg)

![“Non-resident Taxable Person” means any person

who occasionally undertakes transactions involving

supply of goods or services or both, whether as

principal or agent or in any other capacity, but who

has no fixed place of business or residence in India

Non-resident Taxable Person [Section 2(77) of CGST Act

2017]:](https://image.slidesharecdn.com/unit-2-170816134358/85/Important-Definitions-under-GST-25-320.jpg)