Recommended

More Related Content

What's hot

What's hot (20)

Similar to Residential status

Similar to Residential status (20)

More from premarhea

More from premarhea (20)

Recently uploaded

Recently uploaded (20)

Residential status

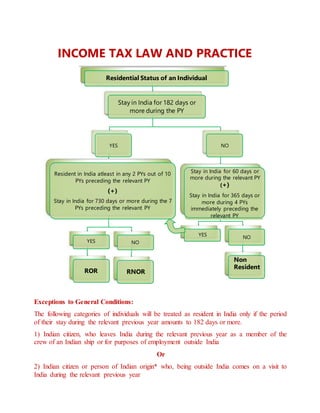

- 1. YES NO NO YES Stay in India for 182 days or more during the PY Residential Status of an Individual INCOME TAX LAW AND PRACTICE YES NO Resident in India atleast in any 2 PYs out of 10 PYs preceding the relevant PY (+) Stay in India for 730 days or more during the 7 PYs preceding the relevant PY Stay in India for 60 days or more during the relevant PY (+) Stay in India for 365 days or more during 4 PYs immediately preceding the relevant PY ROR RNOR Non Resident Exceptions to General Conditions: The following categories of individuals will be treated as resident in India only if the period of their stay during the relevant previous year amounts to 182 days or more. 1) Indian citizen, who leaves India during the relevant previous year as a member of the crew of an Indian ship or for purposes of employment outside India Or 2) Indian citizen or person of Indian origin* who, being outside India comes on a visit to India during the relevant previous year

- 2. Residential status of an individual – Problems 1. Rickey Pointing,an Australian cricketer has been coming to India for 100 days every year since 2006-07: (a) Determine his residential status for the assessment year 2021- 2022. (b) Will your answer be different if he has been coming to India for 110 days instead of 100 days every year. Determine the residential Status of individual a) Previous Year =1.4.2020 to 31.03.2021 i) u/s 6(1) (a) – 182 days or more RPY = =1.4.2020 to 31.03.2021 = 100 days ii) u/s 6(1) (b) – 60 days (RPY) and 365 days for 4 PY immediately preceding the RPY = satisfied RPY = =1.4.2020 to 31.03.2021 = 100 days 1.4.2019 -31.03.2020 = 100 1.4.2018-31.03.2019 = 100 1.4.2017-31.03.2018 = 100 1.4.2016 -31.03.2017 = 100 Total = 400 days Ordinary Resident 6(6) (a) resident in India for 2 years out of 10 PY (b) stay in India for more than 730 days out of 7 PY

- 3. 1.4.2019 -31.03.2020 = 100 1.4.2018-31.03.2019 = 100 1.4.2017-31.03.2018 = 100 1.4.2016 -31.03.2017 = 100 1.4.2015 -31.03.2016 = 100 1.4.2014 -31.03.2015 = 100 1.4.2013 -31.03.2014 = 100 Total = 700 days Hence he is resident u/s 6(1)(b) and he is not ordinaryresident u/s 6(6) as he was resident in India for more than 2years out of 10 previous year preceding relevant previous year and he was stay in India for less than 730 days out of 7 previous years preceding relevant previous year. b) Previous Year =1.4.2020 to 31.03.2021 iii)u/s 6(1) (a) – 182 days or more RPY = =1.4.2020 to 31.03.2021 = 110 days iv)u/s 6(1) (b) – 60 days (RPY) and 365 days for 4 PY immediately preceding the RPY = satisfied RPY = =1.4.2020 to 31.03.2021 = 110 days 1.4.2019 -31.03.2020 = 110 1.4.2018-31.03.2019 = 110 1.4.2017-31.03.2018 = 110 1.4.2016 -31.03.2017 = 110 Total = 440 days Ordinary Resident 6(6) (c) resident in India for 2 years out of 10 PY (d) stay in India for more than 730 days out of 7 PY

- 4. 1.4.2019 -31.03.2020 = 110 1.4.2018-31.03.2019 = 110 1.4.2017-31.03.2018 = 110 1.4.2016 -31.03.2017 = 110 1.4.2015 -31.03.2016 = 110 1.4.2014 -31.03.2015 = 110 1.4.2013 -31.03.2014 = 110 Total = 770 days Hence he is resident u/s 6(1)(b) and he is an ordinary resident u/s 6(6) as he was resident in India for more than 2years out of 10 previous year preceding relevant previous year and he was stay in India for more than 730 days out of 7 previous years preceding relevant previous year. ******** 2. Mr. Joseph, a foreigner, came to India from Poland for the first time on 1st April 2014. He stayed here continuouslyfor 3 years and went to Franceon 1st April 2017. He, however, returned to India on 1st July 2017 and went to Poland on 1st December 2018. He again came back to India on 25th January 2021 on a service in India. What is his residential status for the A.Y 2021-22? Solution: Relevant previous year : 1.4.2020 to 31.3.2021 i) u/s 6(1) (a) – 182 days or more RPY = 1.4.2020-31.3.2021 = 7+28+31=66 days ii) u/s 6(1) (b) – 60 days (RPY) and 365 days for 4 PY immediately preceding the RPY = satisfied RPY = 1.4.2020-31.3.2021 = 7+28+31=66 days

- 5. 1.4.2019-31.3.2020 = Nil 1.4.2018-31.3.2019 = 30+31+30+31+31+30+31+30+1=245 days 1.4.2017-31.3.2018 = 1+31+31+30+31+30+31+31+28+31 = 275 days 1.4.2016-31.3.2017 =365 days Total = 885 days Ordinary Resident 6(6) (e)resident in India for 2 years out of 10 PY (f) stay in India for more than 730 days out of 7 PY Thus Mr. Joseph stayed in India for 66 days during relevant previous year and also did stay in India for more than 365 days in 4 PY preceding the RPY and so he has fulfilled the second condition of section 6(1)(b) hence he becomes resident of India for the PY 2020-2021 And He is an Ordinary Resident of India as he was resident of India for more than 2 years out of 10 PY preceding the RPY and stay in India for more than 730 days out of 7 PY preceding the RPY. ******** 3. Mohan is a citizen of India. He left for Iran on 18th April 2020 and could not return to India till the end of the financial year 2020-2021. Determine the residential status of an individual for assessment year 2021-2022. Solution: Relevant previous year : 1.4.2020 to 31.3.2021 i) u/s 6(1) (a) – 182 days or more RPY = 1.4.2020-31.3.2021 = 18 +0 +0+0+0+0+0+0+0+0+0 =18 days

- 6. ii) u/s 6(1) (b) – 60 days (RPY) and 365 days for 4 PY immediately preceding the RPY = satisfied RPY = 1.4.2020-31.3.2021 = 18 +0 +0+0+0+0+0+0+0+0+0 =18 days Hence Mohan is a non resident u/s 2(30) as he was not satisfied the both conditions of resident u/s 6(1). ******** 4. Mr. Velan of Madurai left India on 12th September 2020 as an employee in Jalausha an Indian Ship and and was back in Madurai on 20th September 2021. Determine his residential status for the assessment year 2021-2022. Solution Determination of Residential status of Mr Velan Assessment year: 2021-2022 Previous year: 2020-2021 a) Stay in India during the previous year 2020-21 1.4.2020-12.9.2020 = 30+31+30+31+31+12=165 days As an Indian citizen employed as member of crew of an Indian ship, Mr Velan has to stay in India at least 182 days in the previous year to fulfill basic conditions 1 and 2 u/s6(1) to qualify as resident. Since he stayed in India only for 165 days in the previous year, he fails to satisfy both the basic conditions. Therefore Mr velan is Non-resident for the assessment year 2021-2022. Note: Additional conditions are irrelevant when a person does not satisfy the basic conditions for being resident. **********

- 7. Residential Status of HUF 5. Head office of XY, a Hindu undivided family, is situated in Hongkong. The family is managed by Y who is resident in India one year out of 10 years preceding the previous year 2020-21. Determine the residential status of the HUF for the assessment year 2021-2022 if the affairs of the family business are a) wholly controlled from Hongkong and b) partly controlled from India. Solution Determination of Residential status of HUF for the assessment year 2021-2022 AY: 2021-22 PY: 2020-21 a) If the affairs of the family business are wholly controlled from Hongkong The residential status of the HUF is “Non-resident” for the assessment year 2021-22 as the control and management of the affairs has been wholly situated outside India. b) If the affairs of the family business are partly controlled from India The residential status of the HUF is “Resident but not ordinarily resident” for the assessment year 2021-22 as the control and management of its affairs is partially done from India and Karta is not ordinary resident because he was resident for one out of ten years preceding the previous year. ****** Residential Status of AOP 6. An AOP carries on business from Chennai. Its president the chief executive, resides in Chennai and controls its operations. Most of its members are foreign citizens and non-residents. a) Determine the residential status of the AOP b) Does it make any difference if its principal officer resides in Bangladesh and controls its affairs? Solution: Determination of Residential status of AOP for the assessment year 2021-2022 a) The AOP is “Resident and ordinarily resident” because its principal officer i.e president resides in India and controls its operations. b) The AOP is Non Resident because its principal officer i.e president controls its operations from outside India i.e Bangladesh. ******

- 8. Residential Status of a Firm 7. K.M.K & Co is a partnership firm registered in India and controlled from India. Out of the 4 partners 3 were in Germany for more than 200 days during the previous year 2020-2021. Determine the residential status of the firm for the previous year 2020-21 and also discuss the residential status of the firm if: i) All the 4 partners are non-resident during 2020-21 ii) All the 4 partners are resident during 2020-21 and firm is controlled from outside India iii) All the 4 partners are resident but not ordinarily resident during 2020-21 Solution Determination of Residential status of KMK & Co for the assessment year 2021-2022 Previous Year =1.4.2020 to 31.03.2021 Assessment Year =1.4.2021 to 31.03.2022 Residential status of the firm is Resident for the previous year 2020-21 as the firm is controlled from India. i) Even if all the partners are non-resident the residential status of the firm still will be Resident as the firm is controlled from India. Residential status of individual partners will be irrelevant in the case of a firm. ii) Residential status of firm will be non-resident as the firm is controlled from outside India. iii) The firm will be resident during 2020-2021, as the business is controlled from India. *********