2. 24

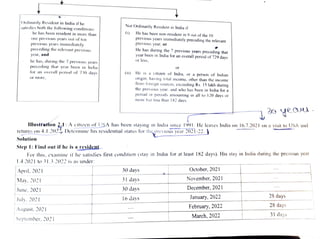

Step 2

.

As he is in India for more than I82

resident.

Thus his total stayinIndia duringthe previoous yearis of 194 days.

Find out ifhe is ordinarilyresident or not

In this case we need not examine the second conditionnasthe fistconditionis alreadysatisfied.

Solution

|Time and hour of leaving and arrival is relevant. However, in thiscaseit is not given. Here number ofFhours are otherwise not

| important as he was in India for mnore than 182 days. It would havebeenimportantifit was a marginal case of 182 days.

201920

SimplifiedApproachtoIncomneTax

days during the relevant previous year, he satisties the first condition

EAamne Ist condition (Residentfor at Jegst) out of l) nrevious vears prior to relevant previOus year)

1en previous years prior to thbe relevant previous vear are 2011-12to 2020-21.

During these years he has alwavs been in India He therefore. satisfics the first condition tor being a resident (1o

stay in India during the relevant previous year).

As he has been in India during the entire period. this condition is also satisficd.

(o NOW examine the second condition (730 davs stav in India during 7previous years prior to the relevantprevious vea)

vellyCars prior to previous year means the period L4 2014 to 31.3.2021. During this period he should be in Irnd:

least 730 days.

As both the conditions have been satisfed he is a resident and ordinarily resident in India.

Problenm 1: M Clinton, an American citizen comes to India for the first time in previous year 2016-l7 1or 120 days, Duries

previous years 2017-18, 20I8-19, 20|9-20. 2020-21 and 2021-22 she stayed in India for 150 days, T00 days, 120 days, 190 da

and 94 days respectively. Determine her residential status for the assessment year 2022-25

AnsResident butnot ordinarily resident in India, (See problem 2.4lofPractical Approach)

Previous Y'ears

.(a Determiee residential status of Shri RajGopal for the assessment year 2022-23.

Alustration 2.2: Indian citizen and businessman Shri Rai Gopal, who resides in Jaipur. went to Germany for employment

purposes on 15.8.202 1and c

(by will your answer be dift'erent if he had gone on a leisure trip?

(a) The previous year for the assessment year 2022-23 is 2021-22. During this period he was in lndia for 137 days (30 + 31

30 + 31 + 15). As he is not in India for I82 davs, he does not satisfy the first condition of category A. The second

condition of category 'A' is also not satisfied because he is a citizen of India and leaves India during the previous year for

employment outside India and is therefore, covered under exceptionNo. lwhere 60days will be substituted by l82 das

Therefore, he is anon-resident. Conditions of categoryBneed not to be examined.

NIstration 2.3: R, a German national, comes to India for the first time

2018-19; 2019-20 and 2020-21 he was in India for 156 davs 7) da

previous year 2021-22, he is in India far 84 days.

(b) Inthis case, although he does no satisfy he first conditiYnof category A, he satisfies the second condition as he was in

India for more than 60 days in the relevant previous year and was also here for more than 365 days during four preced1ng

previous years. He is therefore, resident in lndia. The exception will not be applicable to him because he did not leave

India for the purpose of employment. He satisties both the conditions of category B because he has alwavs been in India

before 1S.8.2021.

Tke status ofthe assessee for the previous year 2021-22 willin this case be resident and ordinarily resident in India.

Detemine the residential status of R for the assessment ycar 2022-23.

Stay in India during previous year 2021-22 -- 84 days

Stay in the four preceding previous years.

156 + 72 + 183 + 161=572 days

andis,

therefore. a

Solution: The residential status in this question is to be detemined for the previous year 2021-2which is relevant to

assess1nent year 2022-23.

He satisfies the 2nd basic condition, hence he isresident in India.

Previous lear 2020-21: Stay in India l61days.

Chap. 2

Stayin 4 preceding previous years.

To deternine whether he is ordinarilyresidentin India he should satisfy boththe additional conditions:

1

Tondition No. l resident inatleast 2poviesycars out of the 10 previousyears

immediately preceding previous year 202-22.

l. Durng the preViOUS years 2017-18,

and l61 ays respectively. Further during the

Days

183

72

Chap, 2

2017-18

2016-17

Total

Hence, he is resident for the previous year 2020-21 as he satisfies the second condition.

Previous year 2019-20: Stay in India 183 days.

Thus, he satisfies the first additional condition.

2020-2 1

2019-20

2018-19

Scope of Total lncome & Residential Status

He is resident in Indiafor previous vear 2019-20 as he satisfies the first condition. There is no need to see the 2nd condition.

Since, he has become resident in 2 previous years immediately preceding the previous year 2021-22, there is no need to see his

residential status for prior previous years.

2017-18

2016-17

2015-16

2014-15

Additional condition No. 2. He should be in India for atleast 730 days in 7 preceding previous years immediately preceding the

DEevious yeer 2621-22. His stay in India in past 7 years is as under:

Previous Years

Total

156

Nil

(by Willyour answer be different if he has been coming to India for 110 days instead of 100 days every year?

Sotution

411

Days

J61

183

72

|56

Ni

25

Ni

Ni

He does not satisfy the second additional condition.

Hexe, he is resident but not ordinarily resident in India.

Alystration 2.4: Rickey Ponting, an Australian cricketer has been coming to India for 100 days every year since 2008-09:

sá) Determine his residential status for the assessment year 2022-23.

572

(a) Rickey Ponting satisfies the second condition of category A because he is in India for more than 60 days during the

relevant previous year and for 400 days during four years preceding the relevant previous year. Therefore, he is a resident.

Further, in this case, although he satisfies the first condition of category of being resident for at least 2 out of 10

preceding previous years but he does not satisfy the second condition of category B as during 7 years preceding the

previous year, he is in India for only 700 days. He shall, therefore, be a resident but not ordinarily resident in India

(b) Yes. He will, in this case, be resident and ordinarily resident in India. He satisfies both conditions of category B' as he was

in India for 770 days in the last seven years and he was resident for at least 2 previous year out of 10 previous years

immediately preceding the relevant previous year.

Illustration 2.5: X came to India from America for the first time on 10. 10.2021.He returms to his home country after staying in

India upto 5.7.2022. Willhe be a resident in India for the assessment year 2022-23?

Solution: In this case although X has been in India for a continuous period of 271 days but it falls in two previous years i.e.

previous year 2021-22 and previous year 2022-23. the previous year 2021-22, his stay in India was only 173 days (22 +30 +

31 +31 + 28 + 31) (ie. 10.10.2021 to 31.3.2022). Therefore, he will be a non-resident in India in previous year 2021-22 as hedoes

not satisfy the first condition of 182 days stay in India during the previous year. Further. the second condition is also not satisfied as,

although, he was in India for more than 60 days in the relevant previous year, he was not here for 365 days or more in 4 preceding

previous years as he came to India for the first time on 10.10.2021. He would also be non-resident in previous year 2022-23, for the

same reasons, if he does n

not come to India thereafter, as the period of stay in India will be 97 days only (i.e. 1.4.2022 to 6.7.2022).

Illustration 2.6:X came to India from America for the first time on 3.10.2020. He retumed to his home country after staying in

India upto 28.9.2021. Will he be a resident in India for the assessment years 2021-22 and 2022-23?

Solution

Assessment year 2021-22: During the previous year 2020-21, he is in India from 3.10.2020 to 319.2021 ie for 181 davs.

Priorto the previous year he has neverbeen in India. He does not satisfy any ofthe conditions ofcategory Aandis therefore, anon

resident.

Assessment year 2022-23: During the previous year 2021-22, he is in India from 1.4.2021 to 28.9.2021 ie. for 181 days. He

does not satisfy the first condition. During 4 previous years immediately preceding the previous year 2021-22 he is in India fo onty

181days. He does not satisfy the second condition also. He is, therefore, anon-tesident.

Icame backto India on l0.J L2022. He has never been out of India in the past.

The second condition is also not satisfied as in the preceding 4 years he was here only for 174 days.

5. (i)

Actual

HRA

received

(10,000

x

12)

1,20,0)

Ihe

minimum

of

the

Solution

taxable

HRA.

benefits.

He

is

also

entitled

to

HRA

of

Z10,000

p.m.

He

actually

pays

?10,000

p.m.

as

rent

for

a

house

in

Delhi.

lWustration

4.6

(Where

there

is

no

change

in

any

factor

during

the

previous

year)

next

change.

together

for

that

period.

Whenever

there

is

a

change

in

any

of

the

above

factors,

it

should

be

separately

calculated

till

the

(4)

HRA

received. (3)

Rent

paid (2)

Place

of

residence

(1)

Salary The

exemption

in

respect

of

HRA

is

based

upon

the

following

factors:

(ii)

50%

of

salary

(ii)

Rent

paid

in

excess

of

10%

of

salary

40%of

salary Rent

paidin

()

Allowance

actually

received

Allowance

actually

received

Mumbai/Kolkata/Delhi/Chennai

Other

Cities

Quantum

of

Exemption:

Minimum

of

following

three

limits:

The

above

provisions

may

be

summarised

as

under:

under

section

115BAC.

4.

Exemption

of

house

rent

allowance

under

section

10(13A)

shall

not

be

allowed

to

the

employee,

if

he

opts

to

be

taxed

3

exemption

of

H.R.A.

is

available.

Where

the

employee

has

not

actually

incurred

cxpenditure

on

payment

of

rent

or

stays

in

his

own

accommodation,

no

taxed

during

the

previous

year.

[Gestemer

Duplicators

Pvt.

Ltd

v

CIT

(1979)

|17

ITR

1

(SC).

commisstOn,

if

rceived

as

a

fixed

percentage

of

turnover

achieved

by

employce,

would

form

part

of

the

salary

emplovment.

All

other

allowances

and

perquisites

will

not

be

included.

However,

as

per

the

Suprcme

(Court

decision,

allowances

and

perquisites.

Thus

dearness

allowance

will

be

included

to

the

extent

it

is

part

of

salary

as

per

terms

of

.

Salary

tor

ths

purpose

includes

dearness

allowance

if

the

terms

of

employment

so

provide

but

cxclude

all

ofher

includedin

prous

Vear,

Relev

ant

penod

means

the

period

during

which

the

said

uccommodation

was

occupicd

by

thc

assessee

during

the

salarv

where

the

house

is

situated

at

any

other

place,

for

the

relevant

period.

(c)

ot

the

salary

where

the

residential

house

is

situated

at

Mumbai,

Kolkata,

Dellhi

or

Chennai

and

40%%

of

the

()

Excss

of

rnt

pad

tor

the

accommodation

oceupicd

by

him

over

|0%

of

the

salary

for

the

'relevant

period"?

a)

Actual

House

Rent

aNNunts:

xempt

under

svtion

T003A).

HRA

is

exempt

under

section

10(13A)

to

the

oxtent

of

the

ninimum

of

the

following

three

wmdation

whieh

the

employee

might

have

to

take.

HRA

0s

tuxable

under

the

hend

'Salaries'

to

thc

extent

it

is

not

House

Rent

Allowanee

is

given

by

the

employer

to

the

enployee

to

mect

the

expenses

in

connection

with

rent

shall

not

be

allowed,

if

the

employee

opts

to

be

taxed

under

section

11SBAC)

4.12

House

Rent

Allow

ance

|Section

10(13A)

and

Rule

2A|

(Exemnption

under

sectlon

Chap. 4

Inome

following

three

amounts

shall

be

exempt

under

section

10(13A):

Computcthe

A

is

entitled

to

a

basic

salary

of

25,000

p.m.

and

dearness

allowance

of

5,000

p.m.,

40%

of

which

forms

part

of

retirement

not

always

be

calculated

on

annual

basis.

As

long

as

there

is

no

change

in

any

of

the

above

factors

it

can

be

calculated

Since

there

is

a

possibility

of

change

in

any

of

the

above

factors

during

the

previous

ycar,

cxemption

for

HRA

should

excess

of

10%

of

salary

employee

in

the

previous

year.

The

salary

of

any

other

period

is

not

to

be

included

even

though

it

may

be

recejvcd

and

2.

Salary

is

to

be

taken

on

due'

basis

in

respect

of

the

period

during

which

the

rentcd

accommodation

is

occupicd

by

the

gross

salary

of

the

employee.

The

mnimum

ot

the

above

three

umounts

shall

be

cxempt

from

tax

and

thc

balunco

shall

bc

taxable

and

thus

Allowance

received

by

the

cmployee

in

respect

of

the

relevant

poriod.

of

the

10(03A)

under

the

Heud

"Salures"

6. 52

(ii) Rent paid in excess of 10% of salary(1,20,000 32,400)

(iü) 50% of salary

Therefore, 87,600 shall be exempt and the balance 732,400 shall be included in gross salary.

Working Note: Salary for the above purpose is calculated as under:

|() Salary 25,000 x 12

(ii) Dearness Allowance 40% of 60,000

Illustration 4.7 (Where there is change in the rent paid)

Basic Salary

(ii) Deamess Allowance (forming part of basic salary)

(iii) Conveyance Allowance for personal purpose

(i) Commission (@ 2% of the tumover achieved which was 22,50,000 during the previous year and the

same was evenly spread.

(v) House Rent Allowance

Solution

X is employed at Delhias the Finance Manager of R Company Ltd. The particulars of his salary for the previous year 2021.2

are as under:

Actual HRAreceived

SimplifiedApproach to Income Tax

|Less: Exemption under seetion 10(13A)

()Actual HRA received

(ii)Rent paid - 10% of salary of relevant period

(a) 90,000 - (10% of 3,93,750)

(b) 60,000 - (10o of 1,31,250)

The actual rent paid by him is /0,000 p.m, for an accommodation at Noida till 31.12.2021. From 1.1.2022. the rent wae

increased to 20,000 p.m. Compute the taxable HRA.

(iii) 40% of salary

I35,000

S0,625

(ompuichis gross salary for the assessment vear 2022-23. ifX

at des not optto be taxed under section |!SBAC

I,57,500

ots fo ho iaxcd undier section l1SBAC

Periodof

9 months

14.2021 to

31.12.2021

Taxable amount 84,375 + Nil 84,375

Exemptionamount <50,62S +45,000 =295,625

Meaning of salarytrom I.4.2021to 31.12.202I 2,70,000+90,000 +33,750 =3,93,750

Meaning of salary from 1.1.2022 to 3|3.2022 90,000+ 30,000 + |1,250=1,31,S0

1,35,000

S0,625

84,375

45,000

46,875

Chap. 4

$2,S00

Duringthe previoUs year 2021-22, he has received arrears of salary pertaining to carlier vears anounting to N0,000.

87,600

1,62,000

3,00,000

24,000

3,24,000

30,000 p.m.

10,000 p.m.

5,000 p.m.

45,000

15,000 p.m.

Period of

3 months

Mr. Nis employed with ABCLtd. on a basic salary of 60,000p.m. He is also entitled to adeamess allowance of 0°% of basN

salary. 70°% of the dearness allowance is included in salary for retirement benefits.The companvgives him HRA of30,000 p.m.

With efect from 1.1.2022, he reveives an increment of 10,000 in his baS0C salary.

1.12022)

to 31 3.2022

45,000

X was staying with his parents till 31.10.2021. From 1.I1.2021. he takes an avommodation on rent in Delhiand pays 2W

nm as rent tor the acconmodation,

45,000

Chap, 4

Solution

Basic Salary:

60,000 x 9

70,000 x 3

Dearness allowance: 20% of basic salary

Arrears of salary

Actual amount of house rent allowance received

Less: Exemption under section 10(13A)

Gross Salary

Working Notes

(2)

(3)

(4)

(i)

(iii)

L1.2021 to 31.12.2021

(a)

1.L2022 to 31.3.2022

(b

Income under the Head "Salaries"

(1) In the above question, there are two factors which have changed but calculation of HRA will be done in 3 parts, i.e.,

(i) L4.2021to 31.10.2021 when he did not pay any rent

(a)

For the period November and December 2021 exemption will be as under:

Actual HRA received (30,000 x2)

5,40,000

when he pays rent but no change in other factors

when the salary has increased

36,320 will be exempt.

2,10,000

Since no rent has been paid from 1.4.2021 to 31.10.2021, no exemption shall be available.

| Salary p.m.

H.R.A.p.m.

3.60,000

87.380

Therefore, 251,060 will be exempt.

Rent paid - 10% of salary [50,000 - 10% of (1,20,000 + 16,800)| i.e. (50,000 - 13,680]

(c) 50% of salary

The total exemption shall be Nil +36,320 +51,060 = 87,380.

Does not opt to be

taxed u/s 11SBAc

For the period 1.1.2022 to 31.3.2022, exemption will be minimum of the following 3amounts:

Actual HRA received (30,000 x 3)

(b) Rent paid - 10% of salary 75,000 -10%(2,10,000 +29,400) ie. 75,000 -23,940

(c)50%salary

7,50,000

Apriland May, 2021 Nil, as he stayed with his parents

1,50,000

Problem 1:Compute theexemption availableunder section 10(13A) in the following cases:

Name of Employee

Place of residence Delhi

(a) does not opt to be taxed under section I15BAC

4,000

(b) opts to be taxed under section 11SBAC

80,000

2.72.620

12,52,620

1,500

Nil

Compute his gross salary for the assessment year 2022-23. if R

B

Noida

6,000

June to October, 2021 3,000 per month for an accommodation in Ghaziabad

1,200

1,000

November. 2021 to March. 2022 - 24,000 per month for an accommodation in Delhi.

Opts to be taxed u/s

Mumbai

80,000

3,60,000

Exemption not alowed

13,40,000

8,000

Rent paid p.m.

Ans. Nil; B-4,800;C-48,000; D-6,000; E-Nil. (See Problem No. 4.13 of"Practical Approach to IncomeTax")

5,000

6,000

$3

11SBAC

7,50.000

1,50,000

Ans. (a)132,650: (b) Z1,59.,500. [See Problem No.4.14 of"Practical Approach to Income Tax"]

60.000

36.320

Problem 2: R is employed with XY Limited on a basic salary of 5,000 per month. He is also entitled to deamess allowance (a

100% of basic salary. 50% of which is included in salary for as per terms of employment. The company gives him HRA of 23,000

per month which was increased to 3.500 w.e.f. 1.1.2022. He also got an increment of 500in his basic salary w.e.f. 1.2.2022. Rent

paid by him during the previous year 2021-22 is as under:

68,400

90,000|

S1,060

1,19,700

E

Patna Bangalore

3,000 S.000

1,000 1.500

800

Illustration 4.8 (VWhere there is a change in 2 factors e.g. salary and rent paid)

400

8. Chap.4

4.42 Interest credited to recognised provident fund

Income under the Head "Salaries"

Anyinterest credited to employees' recognised provident fund in excess of 9.5% per annum is taxable in the nands o u

employeeand hence included inthe gross salary of the employee.

A3 Amountcomprised in thetransferred balance

The aggregate o all sum that are comprised in the transferred balance of unrecognised provident

fund. when itisconverted into recognised provident fund, is also taxablein he handsofthe employee

and hence included in gross salary.

Fordetailed discussion of Provident Fund, etc. see under treatment of provident fund later inthis Chapter.

So far, we have diScussed what are the various incomes, allowances and perquisites which are exempt and wic

Deductions from Salaries (Section 16]

i) Standard deduction (Section 16(ia)]

be included in gross salary. From the gross salary so computed, the followingthreedeductions are allowed under section l6

orovided the employee does not opt to be taxed under section 11SBAC:

(i) Entertainment allowance (Section 16i)]

(ui) Tax on employment (Section 16(u))

4,44 Standard deduction (Section 16(ia)|

The standard deduction from gross salary shallbe t50,000 or the amount ofthe salary, whichever is less.

4.45 Entertainment Allowance (Section 16(ii))

As alrcady discusscd in para 4.14, entertainment allowance is first included in computation of the gross salary. A

deduction is then allowed under scction 161) if cond1tionsprescribed have been satisfied.

4.46 Taxon Employment (Professional Tax) |Section 16(ii)|I

Asper the onstituttonof Ind1a, the State (rovernmentsLocalAuthorities are empowered to make law and collect taxes

on professions,trades, call1ngs and employment

As per section 16), adeduction ofany sumpaud by the assesec, on account ofatax on emnployment, shall be allowed.

The deductionwill beallowed in the ycar in which the tax Is actually paid by the employee.

Note The deductions under section 16(1a), section 16{1) of scction l6(1) shall not be allowed to the cmployce if he

optsto bclaxcd under section I|SBAC

|L Where professional tax is paid by the employer on behalf of the employee, it will first be included in his gross salary

as aperquisite, being amonetary obligationof thc cmployee discharged by the employer. Thercafter, a deduction on

accountof such professional tax will be allowed to the employee from his gross salary.

Professional tax due butnot paid shall not be allowed as deduction.

the following particulars

Illustration fum1shes

4.43

2021-22 from RCompany LId where he is employcd as an Accountant:

Basic salarv

Dearness allowance (forming part of salary for retirement benefits)

EntertainmentAllowance

Children Education Allow ance (lor one child)

He is entitled to use of acar (below l.6 Itrs.) for official and personal work.

He has paid |,200towards professional tax to State Government.

Computec his income from salary for the assessment year 2022-23 if X:

(a) does notopt tobe taxedunder section 115BAC

Solution

97

(b) opts to be taxed under section 11SBAC

his for the

Does not opt to be

taxed u/s 115BAC

2,12,400

24.000

previous year

17,700 p.m.

12,000 p.m.

2250 p.m.

250 p.m.

Opts to be taxed

u/s 115BAC

2,12,400

24,000.

of remuneration

10. Note.--1f

De

taxed

under

section

5BAC.

d

income

account

|Income

from

house

property

5,400

72,000 =

)66,600.

|

Income

from

self

occupied

portion

()72,000

Less:

Dcduction

40%

of

interest

of

1,80,000

72,000

Annual

value

Nil

(B)

Self-occupied

portion

|Income

from

portion

let

5,400

Interest

on

money

borrowcd

(60%

of

R1,80,000)

1,08,000

1,56,600

Standard

deduction

(@

30%

48,600

|

Less:

Deductions Net

annual

value

1,62,000

Less:

60%

of

Municipal

tax

paid

18,000

Gross

annual

value

1,80,000

Actual

rent

|Compute

net

annual

value

..

Expected

rent

is

1,44,000

R15,000 x

12

Hence,

GAV

shall

be

higher

However,

if

cannot

excecd

60%

of

standard

rent

L.e.

R144,000.

1,58,400

of

the

above

two

i.e.

21,80,000.

1,80,000

Hence,

it

shall

be

(60%

of22,64,000)

It

shall

be

60%

of

municipal

value

or

fair

rent

whichever

is

hipher.

Compute

expected

rent

(A)

House

property

let:

Solution:

Since

60%

of

he

propcrty

is

let

and

the

balance

self-0ccupicd

we

shall

compute

the

income

separately.

Interest

on

money

borrowed

for

purchase

of

housc

property

which

was

acquired

in

2010

1,80,00030,000

Municipal

taxes

paid

Standard

rent

20,000

p.m.

22,000

p.m

Far

ret

2,00,000

Municipal occupicdby

him

Illustration

Particulars

(omputc

s

mcOme

Iron

house

property

from

the

following

infonaion

nubmilled

to

you

ad

interest

shall

also

bc

apportioncd

on

he

basis

of

buil

up/tloor

arcu

space.

nrovisio1s

and

thc

Toor

which

is

Nell-oceupied

shall

be

comuled

separately

as

per

self-occupied

provisions,

Municipal

tax

shall

not

be

treated

as

a

single

unit,

Iostead,

incoe

from

lint

tooH

whieh

is

let

shall

he

computed

separately

as

per

iet

our

Smlarly,

wherC.

n

a

buldinp

the

ground

(loor

iN

Nelle0ceupied

nd

first

floor

is

let

out

or

viceversM,

SCH

a

propty

on

built

up

arca

bavis,

Munieipal

valuc

Tar

rent

iT

not

given

sepaately,

nlhall

be

upportioped

between

the

et

out

porion

snd

self

occupied

pon

ER

where

one

mt

IN

let

out

and

the

othc

uilin

nellcubied

heu

he

whole

ooperty

capot

be

taken

as

ia

single

e

detemincd

as

pe

ata

S.10

nder

tlhe

"elf

0ccupied

property"

category

6.11

147

Chap. 5

he/it

shall

an

individual

or

HUF

opts

to

be

taxedon

under

section

115BAC,

neither

be

allowed

loss

of

272,000

from

house

property,

it

shall

not

be

allowed

to

be

set

off

trom

any

other

head,

if

the

individual

or

HUF

onts

to

of

elf-occupied

1

portion

nor

the

loss

of

5,400

on

the

account

is

a

as

if

of

portion

of

the

property

let,

there

loss

under

valueof

the

house

5.14:

R

ows

a

houNC

property

in

Delhi,

o0%

ot

he

pronerty

it

let

out

for

15,000

p.m,

and

40%

portion

I5

Se

uder

o

separatelv

un

he

let

out

poperty

ud

le

income

ofthe

poion

Ibe

part

propety

wlich

is

self

occupied

shall

be

In

this

case

the

Anual

value,

deduetion

and

the

icoe

o

he

past

of

the

popety

which

is

let

shall

he

comnputed

Computation

of

income

of

houNe

property

which

is

purtly

let

and

partly

self

oceupled